Apple upgraded by UBS, seen launching new integrated service

Neil Hughes

Neil Hughes

Analyst Maynard Um had issued a new price target of $265 for AAPL stock, up from $170. The improvement is based on the strength of the iPhone platform, as well as a push toward integrated services across the company's entire line of products.

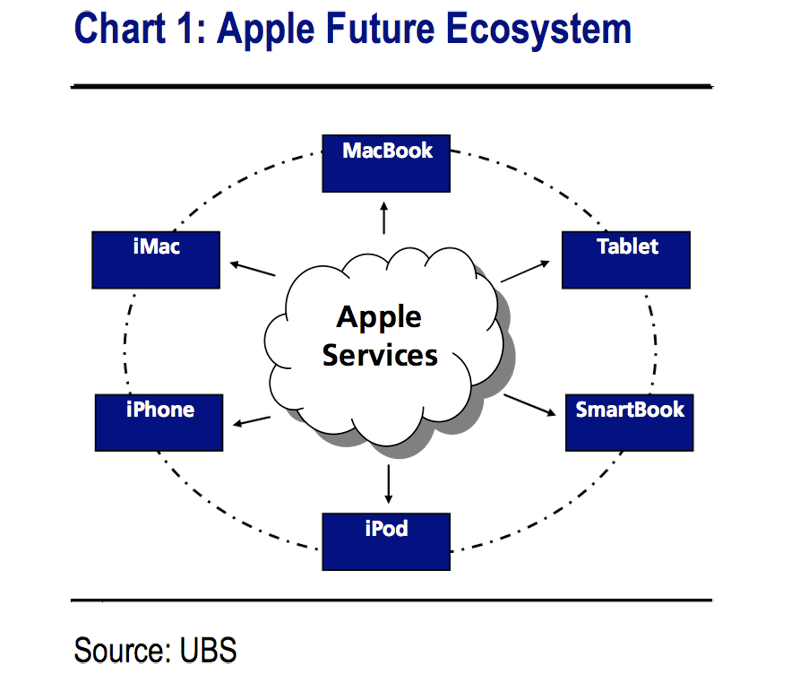

"We believe AAPL may be working on building out a foundation for a service to provide seamless access & mobility of digital content across all of its products," Um wote. "We envision a service that seamlessly allows access to media-focused content of iTunes & user-generated content of MobileMe (pictures/videos/email/caleendar) as well as social networking integration from any existing Apple product."

By tying users in to Apple services, he believes that the company will draw consumers to purchase other products. Essentially, it's the iPod "halo effect" taken to the next level.

Um said that Apple's capital expenditures related to infrastructure and corporate facilities has been growing steadily every year. That number hit $702 million in 2008, Um estimated will be $840 million in Apple's 2009 fiscal year — both well up from the $128 million spent in 2005.

"We believe a material portion of (these capital expenditures) may be related to the size out of a data center/network operating center (NOC) which we hypothesize will be the foundation for a service that provides seamless access and mobility of digital content across all its products, at any time, and from any place," he said.

The UBS upgrade also stems from high expectations for the iPhone. Um sees recurring hardware revenue from an expanding install base and "stickiness" of the App Store with consumers. Um now believes that Apple will ship 36 million phones in its 2010 fiscal year, up from a previous prediction of 25.9 million.

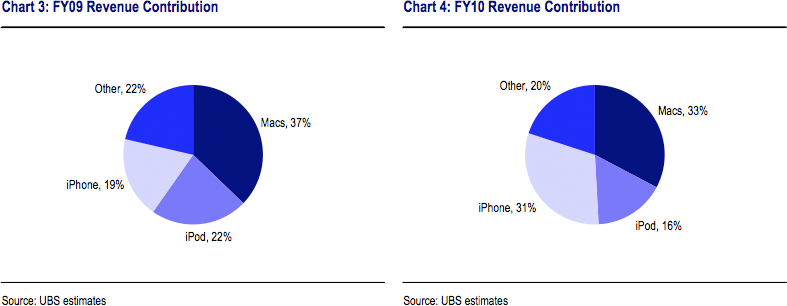

Margins for iPods are expected to be above 20 percent, Mac margins in the high 30 percent range, and iPhone margins above 40 percent.

Um also said he sees more products on the way from Apple, namely a data-only product at Verizon and a tablet. The report suggested that the new Verizon hardware could be a "smart book." Um also sees the iPhone being made available on additional carriers in the next year, and an upcoming refresh to the Mac desktop line.

After Apple reported a record third quarter this summer, UBS was not as enthusiastic about the company's stock as other analysts. The firm, at that point, maintained its neutral rating.

In August, Um upgraded the recommendation to a short-term buy, based on MacBook Pro and iPod refreshes and iPhone 3GS expansion. At the time, the long-term forecast remained neutral based on global economic weakness.

William Gallagher

William Gallagher

Malcolm Owen

Malcolm Owen

Sponsored Content

Sponsored Content

Christine McKee

Christine McKee