Wall Street expects new iPad to continue dominating tablet market

Josh Ong

Josh Ong

Apple's new iPad features a 2,048-by-1,536 pixel resolution Retina Display, a faster processor, LTE 4G, a 5-megapixel camera and voice dictation. The tablet goes on sale March 16 in 10 countries.

Though the third-generation iPad was largely in line with analysts' expectations leading up to Wednesday's media event, they view the new tablet as a positive for Apple and expect it to help the company widen its lead over its competitors.

Piper Jaffray

Piper Jaffray analyst Gene Munster wrote in a note to investors that the new iPad is a "significant upgrade" to the iPad 2. He expects the device and a new version of iOS will help Apple maintain its lead in the tablet market.

Munster also noted that the lower-priced iPad 2 is "a strong defensive move" in the face of competition from Amazon's Kindle Fire and other budget tablets. The analyst does not expect the older entry-level iPad to cannibalize sales of the new model, noting instead that it will expand "Apple's addressable market in the rapidly growing tablet space."

The investment bank expects Apple will lead the tablet market to outgrow the PC market in the long term. Given the firm's long-term outlook, Munster cautioned that its current near-term estimate of 26 percent year-over-year unit growth may be too conservative. Piper Jaffray's estimate of 450 million tablet sales, including 225 million iPad sales, in 2016 implies an annual growth rate of 40 percent over the next four years.

The firm maintains an Overweight rating for Apple stock with a price target of $670.

UBS

Maynard Um reiterated UBS' Buy rating for Apple and its $550 price target. According to the analyst, the accelerated international launch of the new iPad could "provide upside" to estimates for the March quarter. Apple will launch its third-generation tablet first in 10 countries on March 16 and 25 more countries a week later. The company waited two weeks before going international with last year's iPad 2 launch.

UBS currently expects Apple to ship 12 million iPad units during the March quarter

RBC Capital Markets

Analyst Mike Abramsky said Wednesday he expects the new iPad to "maintain Apple's tablet dominance." According to him, Apple's "powerful ecosystem," which includes iTunes, iTunes Store, iCloud, iOS, App Store, and carrier/store distribution should help drive sales of the device.

RBC continues to expect Apple will ship 62 million iPads during calendar 2012, holding on to a 74 percent share of the tablet market. Abramsky viewed the third-generation iPad as "raising the performance bar" for tablets, since it has the highest-resolution screen on a tablet, a faster processor than the NVIDIA Tegra 3 and 4G LTE.

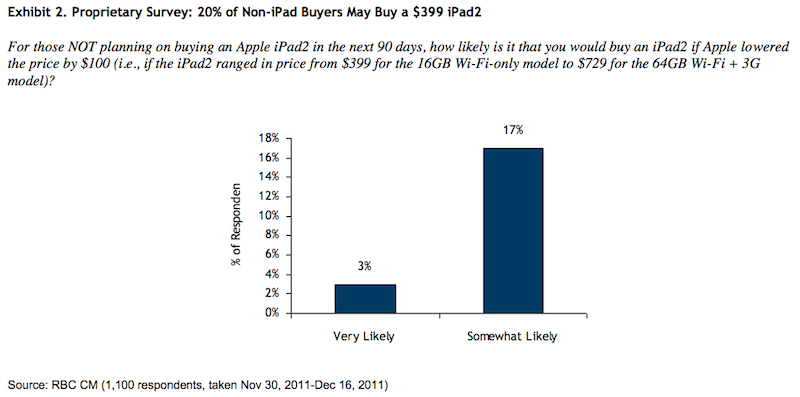

The analyst added that the cheaper iPad 2 should have a better appeal to price-sensitive buyers. An RBC survey from late last year found that 20 percent of non-iPad buyers were "likely" to purchase a $399 iPad 2.

Deutsche Bank

Chris Whitmore described Apple as "lapping the competition again" with the new iPad. The launch of the device arrived earlier than the analyst originally expected, so he also noted a potential upside in March quarter iPad sales.

Whitmore expressed the belief that Android and Windows tablet competitors will "have trouble matching" the price-performance specs of Apple's current iPad lineup. He expects Apple to "continue to dominate the category." The firm now believes its 60 million iPad estimate for 2012 is "beatable."

Deutsche Bank also believes developers will "flock" to the iPad's raw performance characteristics. A side-by-side comparison of the third-generation iPad and the iPad 2 showed that the new hardware was "particularly impressive" when running graphics intensive applications such as games or video content.

"We expect this upgrade to attract even more developers to the iOS platform (315M+ units shipped) whose new Apps (200K+ and counting) will attract even more users to the platform," he said.

Whitmore viewed the iPad ecosystem as winning out against its rivals. He pointed out that Windows 8 is receiving "mixed reviews" and is not expected until the second half of 2012. According to him, Android is in "disarray," making the iPad's value proposition for developers "abundantly clear."

J.P. Morgan

J.P. Morgan's Mark Moskowitz said the combination of upgrades in the new iPad should "cement Apple's market dominance in a preemptive response" to the flood of Windows 8 tablets later this year. He called the third-generation tablet a "quality" upgrade.

The analyst also marveled at Apple's ability to add LTE without compromising battery life. J.P. Morgan's research shows that battery issues have been an "impediment to broader manufacturing and adoption of 4G LTE-capable devices." As such, he noted Apple has having accomplished an "impressive feat" by dramatically improving iPad specs while maintaining 9-10 hours of battery life.

Moskowitz also said he expects comments from Apple CEO Tim Cook that there is "a lot to look forward to" from Apple in 2012 to stoke speculation about the rumored full-fledged TV offering. In the firm's view, Apple's leadership through innovation "stands to continue" and should drive the company's stock even higher.

Morgan Stanley

Katy Huberty told investors she expects the new iPad to "drive strong demand." The investment bank's model conservatively predicts a 1.2x unit increase in iPad shipments over the next four quarters as compared to the prior four. A 2.3x increase in iPad shipments occurred after the iPad 2 was introduced last year.

If the iPad were to continue growing at the 2.3x rate, Apple could ship as many as 90 million iPads this year. The firm currently expects shipments of 51 million units during 2012.

Morgan Stanley characterized Apple's price cut on the iPad 2 as an important move to "expand its addressable market and grow profit dollars." An earlier survey by the firm showed that Apple could stimulate 15-20 million incremental U.S. unit demand and 38 million global demand by lowering the iPad 2 price by $100. According to Huberty, each incremental one million iPads could add $0.20 of earnings per share.

The analyst does not expect the iPad 2 discount to affect Apple's gross margins. She estimates Apple has negotiated 20 percent annual component cost decreases from suppliers. Assuming a 30 percent shipment mix of cheaper iPads, the gross margin of the iPad would deteriorate by just half a point, Huberty noted.

Malcolm Owen

Malcolm Owen

Christine McKee

Christine McKee

Amber Neely

Amber Neely

William Gallagher

William Gallagher