UBS: Apple deserves benefit of doubt with iPhone 5c pricing

Kevin Bostic

Kevin Bostic

Assorted investment analysts who downgraded Apple stock in the wake of last week's new iPhone 5c reveal may have been a bit hasty, according to a new report out from UBS that says Cupertino may have earned the benefit of the doubt.

A number of analysts largely expected Apple to hit a lower unsubsidized price point for the polycarbonate-backed iPhone 5c, which was unveiled last week, but were disappointed when the final cost was officially announced. Many panned the decision, though Apple's choice to go premium may ultimately play out in its favor, a UBS report said on Monday.

"Apple probably deserves more credit than the view it is asleep at the wheel," reads the report from UBS, which retains a neutral 12-month rating on AAPL. "Successful companies historically have consistently chosen better over cheaper, for which Apple is the poster company."

UBS was actually among those firms that cut their AAPL ratings to neutral following the unveiling of the iPhone 5c.

UBS attributes its own downgrade to three factors. First, the firm was "concerned that Apple might be disrupted." It was also "worried that investors are worried Apple might be disrupted." Finally, there were concerns that, even if correct, Apple's strategy may not play out for some time.

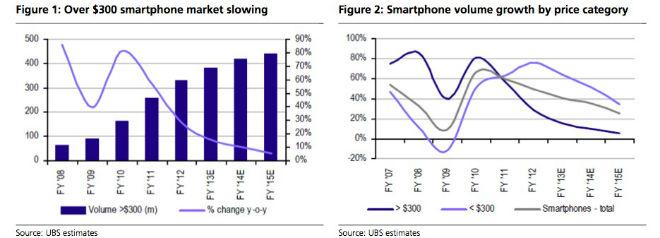

The new report posits that Apple's management may well be aiming for the growing global middle class with the iPhone 5c instead of the much lower-end markets some were expecting. A $400 price point, analysts believed, would help Apple address a significant portion of the fastest growing smartphone consumer segment. Instead, Apple announced the 5c at a $549 price point, more than a third more costly than some investors had hoped.

UBS sets a 12-month price target for AAPL at $520, noting that it is still "right on its 200-day moving average with the 50-day having just moved above the 200-day MA (a bullish golden cross.)" The firm predicts a price-to-earnings ratio of 11.5, or $45.46 per share for fiscal 2014.

Malcolm Owen

Malcolm Owen

William Gallagher

William Gallagher

Sponsored Content

Sponsored Content

Christine McKee

Christine McKee