Kevin Bostic

Kevin Bostic

Apple's lower gross margins — and, subsequently, its lower stock price — could be largely attributable to cyclical drivers such as capital expenditures and component pricing, paving the way for a significant improvement with the launch of a so-called "iPhone 5S," a new analysis argues.

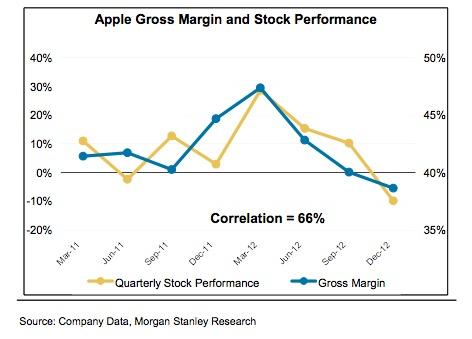

Morgan Stanley's Katy Huberty pointed out on Monday that Apple's quarterly stock performance and gross margin both peaked in March of 2012. Thereafter, capital equipment investments in preparation for the launch of the iPhone 5 and higher NAND flash prices knocked margins down 900 base points.

Huberty expects that Apple will follow its previous patterns and release an "iPhone 5S" that will not likely require much in the way of significant hardware changes. She also expects Apple to grab better deals on NAND components going forward, a trend possibly foreshadowed by the release of a 128-gigabyte iPad.

Huberty's take stands in opposition to some pessimistic investors, who have expressed concern that Apple's volatility in gross margin could be as a result of structural issues with the company. But she believes that lower capital equipment purchases and potentially more favorable NAND flash prices could result in improved margins toward the end of 2013.

As evidence, Huberty pointed to Apple's 10-Q filing, in which the company revealed that its purchase commitments for the current quarter are just $904 million. That compares to $4.5 billion just two quarters ago, when the company invested in new in-cell touch displays for the iPhone 5 launch.

For its part, Apple's own guidance projects that the company's fiscal year 2013 gross margin will fall short of its peak of 43.9 percent in fiscal year 2012. Morgan Stanley's models call for Apple to see gross margins of 38.7 percent in fiscal 2013.

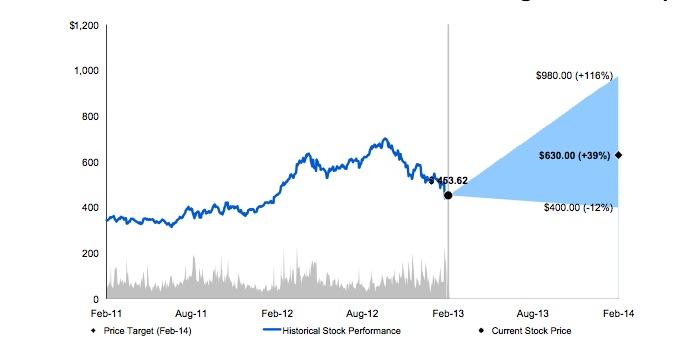

Morgan Stanley lowered its price target for AAPL stock to $630 last month, but has retained its overweight rating for the company. Huberty did caution that she believes near-term catalysts for the company are limited, as Apple faces tougher comparisons in the first quarter of calendar 2013.

The investment firm's price target falls in the middle of a range of possibilities seen: The "bull case" sets a 12-month target of $980, based on the possibility of Apple releasing a new iPad and lower-cost iPhone this summer while reaching an agreement with China Mobile. The bear outlook for the stock targets $400, with Apple losing share to Windows 8 and Samsung in mature markets and lower-priced options in emerging markets.

-m.jpg)

Christine McKee

Christine McKee

Charles Martin

Charles Martin

Mike Wuerthele

Mike Wuerthele

Marko Zivkovic

Marko Zivkovic

Malcolm Owen

Malcolm Owen

William Gallagher

William Gallagher

-m.jpg)

32 Comments

You don't say!

I have lost track of how many times I have seen the ole 'reduced margins' spin to knock AAPL down after a product refresh.

The study of AAPL shows us almost everything that is wrong with the stock market and the psychology of "investors" in the U.S.. Companies know they'll likely be "punished" for making R&D or capital investments because all "investors" are interested in is the bottom line (although, sometimes, that's even giving them too much credit), just like AAPL is punished, ignoring the blatant manipulation, for decreased margins. So, for years, American companies didn't, and foreign companies are now eating their lunch. Just one of the many negative consequences of running a company with a focus on "maximizing shareholder value", rather than making sound business decisions.

I've written this before, but if margins are such a big deal, then why doesn't Apple jack up it's prices? I don't give a crap if some people can't afford Apple devices, too bad for them. Frankly speaking, life isn't fair, and if somebody can't afford a new Apple device, then go buy something else, problem solved, just please don't whine about it. And also, why does Apple keep expanding into new markets? Why not cut down in some markets? Keep a presence in key markets and then there will be enough supply, and Apple can maintain their big margins. It's the same story over and over again. Apple releases something new and there are often delays because they are not able to meet the initial demand. And there's no good reason or excuse behind these delays. It's not like a natural disaster or an act of nature occurred. These are man made delays and somebody is surely to blame.

It seems to me that certain people wish to turn Apple into junk, and for no good reason. A cheaper iPhone? Why? What's that going to do for margins? Even if Apple were to sell 117 million phones in a quarter, then that probably won't be good enough, because some crackhead on Wall Street predicts 118.4 million.

Instead of making cheaper phones for people who live in mud huts, I'd like to see Apple go in the opposite direction. Release something like a limited edition iPad! Make it look irresistible and have it come with some awesome features, with a price tag to match. Raise the margins instead of lowering them by making ghetto iPhones for ghetto people.

[quote name="AppleInsider" url="/t/155790/apples-margins-predicted-to-change-improve-with-the-seasons#post_2270883"]As evidence, Huberty pointed to Apple's 10-Q filing, in which the company revealed that its purchase commitments for the current quarter are just $904 million. That compares to $4.5 billion just two quarters ago, when the company invested in new in-cell touch displays for the iPhone 5 launch..[/quote] Apparently, understanding something about business finances is not necessary to become an analyst. Purchase commitments do not affect the gross margin when they are made. Rather, the gross margin is affected when the parts are actually used (or scrapped). Let's say that Apple sells $20 B of product every quarter and their gross margin is 40% so COGS is 60%. For simplicity, let's say that this is $10 B of component purchases per quarter and $2 B of overhead and assembly cost). So in a year, Apple would buy $40 B of components. From a gross margin standpoint, it doesn't matter if they buy $800 M per week or if commit to buy $10 B at the beginning of each quarter or even if they commit to buy the entire $40 B on January 1. It would make no difference at all in terms of gross margin. (It does, however, matter, particularly on the balance sheet. If they prepay, it reduces their cash by that amount. A purchase commitment might also become a liability if they commit to paying it regardless of whether they need the product or not, but, of course, we don't know if they made that kind of commitment, anyway). Sorry, Katy, but you're just plain wrong. Of course, anyone who has followed your prognostication for years already knows that.

Minor fluctuations aside, component costs tend to drop over time. Apple product prices, however, don't drop much at all over time. The result: better Apple gross margins over time.