Shares of Apple stock slid Thursday morning after investment firm Barclays Capital lowered its rating on shares of the iPhone maker, saying it doesn't expect the stock to break out of its current trading range within the next year, and suggesting its performance could become comparable to that of rival Microsoft.

Analyst Ben A. Reitzes issued a note to investors, provided to AppleInsider, in which he advised them to "step aside," citing a maturing smartphone market that he believes presents limited future growth potential for Apple's iPhone. And without a new "revolutionary" product, he doesn't believe shares of Apple will see a boost anytime soon.

"Frankly, we just couldn't quite bring ourselves to use smart watches or TVs as reasons to raise numbers — nor were we fully convinced that these products could move the needle like new categories did in the old days," Reitzes wrote on Thursday.

The analyst said that as an iPhone user, he's "very excited" about some of the company's new products in the pipeline, with potential innovations in mobile payments, geolocation, and wearable devices. But as an investor, he doesn't see Apple introducing anything as groundbreaking from a financial perspective as the iPhone or iPad.

"We believe Apple's story is all about iPhones and 'new categories' seem to be designed to make the iPhone more useful — Â but don't necessarily reaccelerate growth in the iPhone category to sustainable double-digit levels," he wrote. "If we were to see evidence that payments and/or new content deals enhance the Web services aspect of Apple vs. Google and others long-term, we may need to reassess this opinion."

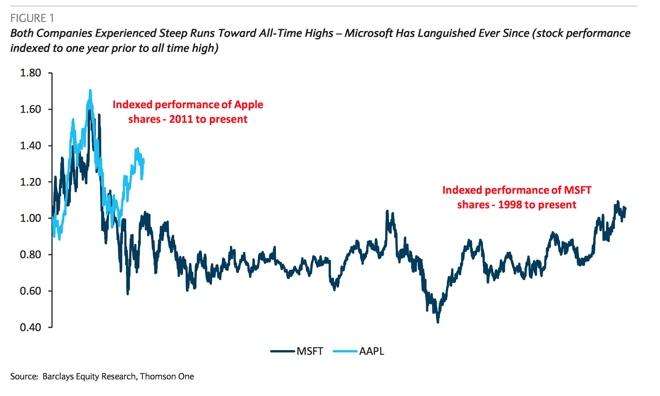

Reitzes then went on to cite the valuation of Apple's rival Microsoft from 2000 to 2010, and suggested that Apple might see a similar pattern. The analyst said that he sees "no precedent" that large tech companies can broadly outperform once again after "a tough year or two."

In his eyes, the "law of large numbers" may have caught up with Apple, and the company's gross margins may have peaked.

"As a result, there doesn't seem to be anything wrong with saying shares could be range-bound as we move from product cycle to product cycle until we can see Apple creating entirely new markets in the cloud," he said.

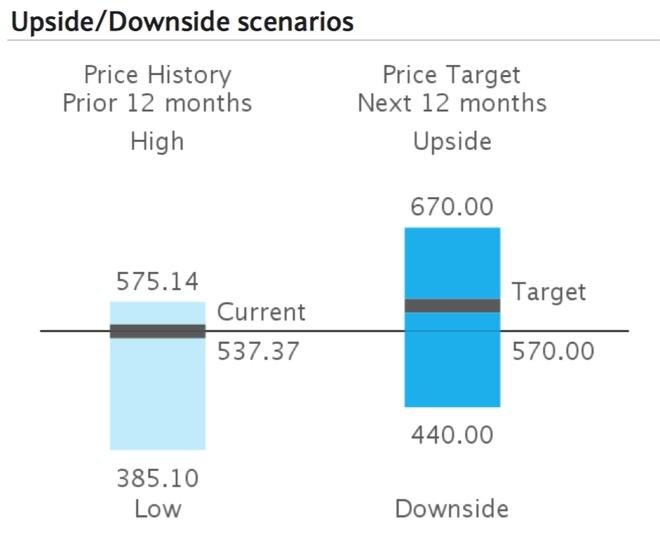

Accordingly, Barclays has downgraded Apple from an "overweight" rating to "equal weight," with a continued "neutral" outlook for the company. The firm's price target for shares of AAPL is $570, or about $35 higher than where it is trading as of Thursday morning.