In spite of recyling many parts from other iPhones, Apple's profit margin on the iPhone SE is relatively low next to the high-end iPhone 6s, a new analyst estimate suggests.

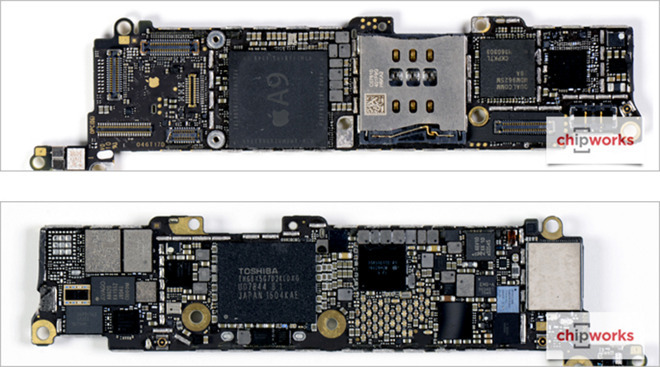

Based on a recent Chipworks teardown, Apple's bill of materials is probably about $260, RBC Capital Markets analyst Amit Daryanani argued in a memo obtained by AppleInsider. Given an entry retail cost of $399, that would indicate a profit margin of roughly 35 percent, lower than the mid-40s estimated for the iPhone 6s or the now-defunct 5s.

The SE's bill of materials is about 22 percent cheaper than the 6s, Daryanani noted. The analyst suggested that Apple likely renegotiated prices with its suppliers, taking advantage of excess parts inventory generated for the 6s.

In the Chipworks teardown, markings showed the sample phone's A9 chip was manufactured by TSMC around August or September of last year — presumably for the 6s, not the SE. Many other parts are also identical to those in the 6 and 6s, such as modem and audio hardware.

The SE also uses the same display as the 5s, and similarly old Broadcom touchscreen chips.

"While most of the components in iPhone SE were previously used in either iPhone 6/6s or 5s, we think the prices for the same components have likely come down by >10% reflecting better scale and importantly price concessions from component providers, especially considering some of the components were likely from excess capacity for 6s," Daryanani wrote.

RBC is maintaining an "outperform" rating for Apple stock, along with a $130 price target. It's thought that the SE could generate $6.8 billion in revenue for Apple during calendar 2016.