Andy M. Zaky, Bullish Cross, Special to AppleInsider

Andy M. Zaky, Bullish Cross, Special to AppleInsider

We're talking about the mother of all earnings blowouts. Well maybe not that big, but certainly the largest blowout in company history without question.

The difference between wealth and poverty on Wall Street is determined by ignoring the fluff, respecting the details and using reason to tease out the bottom-line reality generally overlooked by the masses. While everyone focuses on whether the passing of Steve Jobs marks the end of Apple, or whether the Amazon Kindle Fire will kill the iPad, the company is quietly selling millions upon millions of iPhones that far exceed even the most rosy expectations.

The most valuable company in America is about to grow its earnings by a whopping 84 percent this quarter, and Wall Street is asleep at the wheel. Apple's trailing twelve months of earnings is going to skyrocket from $27.68 to at least $33.00 which will finally drive Apple's P/E ratio down into the 11′s. While fund managers continue to debate whether they should buy Amazon (AMZN) at a 95 P/E ratio or Google at 22 P/E ratio, Apple will have reported more in revenue in one quarter than each of these companies reported all last year.

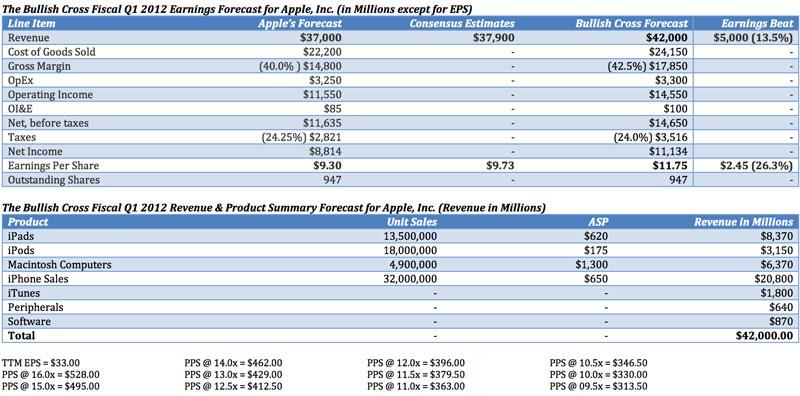

Bullish Cross Research expects Apple to report $11.75 in EPS on $42 billion in revenue in fiscal Q1, which compares to the Wall Street consensus estimates of $9.79 in EPS on $38 billion in revenue. The Bullish Cross outlook, if proven accurate, will amount to Apple reporting the largest revenue and earnings blowout in the history of the company. The table below outlines the Bullish Cross Fiscal Q1 2012 Earning Forecast for Apple Inc. and includes a very specific breakdown in our revenue expectations:

We expect this blowout to be largely driven by Wall Street underestimating the power of the iPhone side of the force. That will be the story this quarter. We expect Apple to conservatively report that it shipped 32-40 million iPhones far ahead of the 25 million iPhones that Wall Street expects out of the company. That will be the largest gap between Wall Street expectations and actual results since the iPhone was first introduced in 2007.

Yet, not only do we believe that Apple will comfortably ship 32 million iPhones without a hitch, we think our expectations will actually prove too conservative. In fact, we believe that Apple will actually end up reporting sales of more than 35 million iPhones which will cause the heart attack of at least several hundred short sellers. It will be a total deer-in-head-lights type earnings blowout where people just stand there and say "WTF" repeatedly while slowing doing the defeated head-shake — CNBC contributor Steve Cortez will be among their number with his admitted Apple short position.

While we think Apple will basically more or less report in-line on iPads, iPods and Macs, iPhone sales will redefine everything Wall Street thought they knew about the company. The minute this report hits the street, the cyclical Apple bear will be shot point blank in the head. You're going to see the sentiment shift from ultra-bearish to ultra-bullish in mere seconds. We've seen it happen before and we're about to see it happen again in fiscal Q1. So the bears have about 3-4 more weeks to live. Enjoy it while it lasts.

Now it is important to understand that investors should view the Bullish Cross "official" outlook this quarter as being merely the lower boundary of what one should reasonably expect Apple to report. While we think there's a significant chance that Apple will end up reporting $11.75 in EPS on $42 billion in revenue, we still believe that there's a much higher likelihood that Apple will report a quarter that is more in-line with the outlook presented by my colleague at Asymco, Horace Dediu. Horace Dediu is one of the best analysts out there, is one of the leading experts on the global smart-phone market, and is a testament to his Alma Mater, the Harvard Business School.

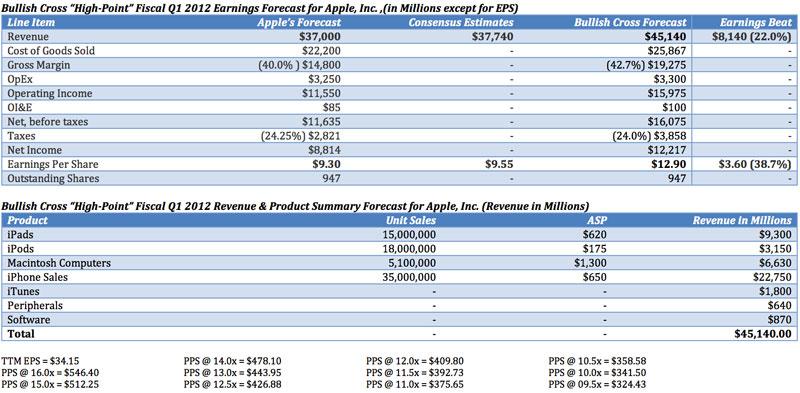

Dediu has put together an expectation that is very much in-line with the Bullish Cross "high-point" forecast for Apple. Our "high-point" forecast is an expectation we put out every quarter that takes into account the possibility that Apple could deliver a perfect quarter. Notice that Apple has delivered a report that was in-line or slightly above the Bullish Cross high-point estimate twice in the past two years. Once in fiscal Q2 2010 and again in fiscal Q3 2011. Both times it resulted in Apple gapping up uncontrollably after being unhalted in after-hours. The table below outlines the Bullish Cross High-Point Outlook:

This expectation outlined by Dediu, if proven accurate, will result in an unimaginable blowout of epic proportions. We're talking about a top-line beat of nearly $7 billion with iPhone sales blowing out estimates by over 10.7 million units or nearly 50 percent. The most Apple has beaten the consensus on iPhones in any previous quarter has been by only a few million units or about 20 percent. That's at the high end. Here we're talking something completely unseen before on Wall Street. Missing iPhone units by 50 percent will force the street to go back to the drawing board and re-evaluate everything they thought they knew about the company.

The Dediu outlook is calling for Apple to report $12.30 in EPS on $44.6 billion in revenue on the back of sales of 35.7 million iPhones, 14.7 million iPads and 5.2 million Macs. Dediu is expecting iPhone sales to grow 120 percent leading to a 91 percent increase in earnings per share.

If this outlook by Dediu comes to pass, it will lead to the biggest gap-up in the history of the company. In fact, I think such a report will lead to at least a 10 percent gap-up in the stock if not more. What I would expect to see is Apple halted at least 10 minutes before the results are released and once Apple resumes trading, we should see the stock $50.00 higher. If Apple is trading around $400 when it reports its results, it will gap-up to $450. If it's trading at around $430 a share when it repots, it will test $500 that week.

This is a once in a decade type earnings reaction that we've seen happen a few times with Google. Haven't really seen that type of an earnings reaction out of Apple yet. And that's mostly because Apple typically runs into the results.

Moreover, Apple tends to almost always sell-off after reporting earnings in fiscal Q1 as the stock tends to rally significantly between September and January. Here, Apple has been trading sideways since July. So there hasn't been much of a run-up in the stock price.

Thus, the type of reaction that we will get this quarter will largely depend on the type of pre-earnings run-up we see in the stock. If the bearish sentiment and trading action continues up until the day Apple reports earnings and we get a Horace Dediu blowout, Apple's going up $50.00.

Again, this type of a blowout expected by Dediu is a once in a decade type earnings blowout and we'll observe a corresponding once in a decade type response in the stock price. Yet it is important remember that Dediu is presenting what is the equivalent of our high-point outlook. If everything goes perfectly, we will see his expectations come to fruition.

But if the Bullish Cross "official" outlook is to be viewed as the lower boundary, then the Horace Dediu outlook forms the upper boundary. You should expect Apple to report between those two outlooks. And when it does, it will be a record blowout regardless. Our lower boundary is already calling for a record revenue and earnings blowout out of Apple.

For those who are interested in the events and reasons leading up to this eventual blowout, we basically explain how it came to this in two articles entitled, Why Apple's Guidance is Still Conservative and How to Properly use Apple's Guidance to Accurately Forecast Earnings.

Andy M. Zaky is a fund manager at Bullish Cross Capital and the editor of the Bullish Cross Financial Newsletter. Bullish Cross Capital owns a significant long position in Apple, Inc.

-m.jpg)

Wesley Hilliard

Wesley Hilliard

Stephen Silver

Stephen Silver

William Gallagher

William Gallagher

Charles Martin

Charles Martin

Marko Zivkovic

Marko Zivkovic

Andrew Orr

Andrew Orr

Amber Neely

Amber Neely

89 Comments

Oh, great. So when this is wrong, the stock will tank and…

Well, you know the drill.

THIS ISN'T HELPING!

I used to think Daniel Eran Dilger was the most hyperbolic writer on this site, but Andy M. Zaky sure takes the cake now. I hope it's true though, that earnings will increase 84%.

Oh, great. So when this is wrong, the stock will tank and?

Well, you know the drill.

THIS ISN'T HELPING!

Worse, Apple will likely achieve this, and yet, perhaps after a brief, tepid bump, it's back to noodling around at where it is now.

At this point, I am convinced the market is waiting to see Apple successfully execute a major new product intro post-Jobs. (Which, they will, superbly).

Oh, great. So when this is wrong, the stock will tank and…

Well, you know the drill.

THIS ISN'T HELPING!

... and if he's right... well, let's just say that there will be shorts filling their shorts.

[but there is always the possibility that even if Apple pulled off a $45 billion quarter the analysts would say that Apple will never be able to keep up that momentum and therefore give Apple a neutral rating. Fiscal q2 is unveiled in April and Apple shows $35 billion in rev... the analysts say, "I told you so!"... and AAPL declines 10% by the end of May.)

Largest earnings blowout in the history of the world. Run while you can. Take cover. Happens right after closing bell. Go, go, go.

[LOL. Wipes tears from eyes.] Seriously though, Andy Zaky has a good record. He posts his numbers before the call and I'm astonished that he's gotten so much closer than analysts with, ahem, less flair for the dramatic. I appreciate that his posts appear here but make sure to take a heaping measure of salt with any predictions. ("It is difficult to make predictions, especially about the future." - Yogi Berra)