How to properly use Apple's guidance to accurately forecast earnings

Andy M. Zaky, Bullish Cross, Special to AppleInsider

Andy M. Zaky, Bullish Cross, Special to AppleInsider

Understanding how to properly use Apple's guidance to forecast earnings will get you to within 5 percent margin of error. Yet, to get there you have to use the right methodology. Trying to extrapolate anything from EPS guidance simply isn't it.

The very first thing any good analyst should look for when forecasting Apple's earnings is the company's revenue guidance. Apple's revenue guidance is not only the most important and consistent line item in the company's overall multi-layered guidance, but it is by far the most important data point period. Those with a very strong background in finance can very accurately forecast Apple's full income statement simply by understanding how to interpret the company's revenue guidance. Yet, unlike Apple's revenue guidance, its EPS guidance is by far the most random, meaningless and inconsistent number which acts as nothing more than a red herring for the inexperienced.

The reason for this is actually quite simple for a financial analyst but complicated for the average Seeking Alpha contributor to understand. It demands more than a surface understanding of accounting and financial analysis as well as a highly specialized knowledge of the way guidance actually works. The problem is, that 99 percent of the entire financial community and 100 percent of the financial press is completely clueless when it comes to this issue. So that results in a lot of bad analysis being circulated.

In order to accurately forecast Apple's income statement, it requires a top-line down approach to Apple's guidance. You have to begin the analysis by looking at Apple's revenue guidance. A good analyst will be able to infer within a 1-3 percent margin of error what Apple's revenue will be in any given quarter using nothing else than Apple's revenue guidance.

From there, you use Apple's gross margin guidance in order to determine what the company will report in overall gross margin. Apple typically sandbags gross margin by 250 basis points +/- 30 basis points on a very consistent basis. Simply adding 250 basis points to Apple's gross margin guidance will lead to extraordinarily accurate results on a very consistent basis.

From there you simply add $50 million to Apple's OpEx guidance as Apple consistently under-estimates its expenses by about $50 million. That will get you down to operating income. Apple typically sandbags OI&E by $15 million. That will get you down to net income before taxes.

Recently Apple has been giving us the tax rate guidance almost perfectly. Simply multiply the tax rate by Apple's operating income and you arrive at a highly accurate net income number. After that, all you have to do is reverse engineer what Apple expects in outstanding diluted shares in the quarter by using simple algebra, and you will arrive at an EPS forecast that will very likely be within a 5 percent margin of error to Apple's actual results. That's the methodology we're going to develop below.

Our objective is thus two fold. First, we going to demonstrate how one can very accurately put together one of the top income statement forecasts that will beat every single Wall Street analyst simply by using nothing more than Apple's guidance. Secondly, we're going to show why the method of doing so requires one to simply ignore Apple's EPS guidance as being random, meaningless and distracting.

On page two, revenue tells the whole story.

1. Revenue Tells the Whole Story

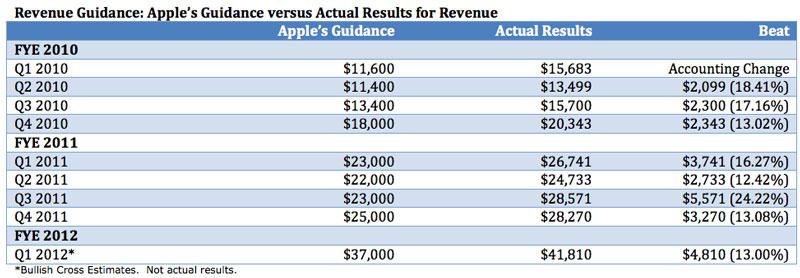

Over the past several years, and especially after undergoing a major accounting change in fiscal Q1 2010, Apple has consistently reported a quarterly revenue number that was precisely 12-18 percent above its revenue guidance. Regardless of how rosy or conservative the Wall Street consensus happens to be, regardless of what Business Insider has to say about the Android destroying iPhone sales, regardless of all of the channel checks, Gartner & IDC research data, Comscore, NPD data, and the supply chain.

Regardless of rumors of Apple cutting manufacturing orders by 90 percent as falsely reported every quarter by the Chinese equivalent of the National Enquirer, Digitimes. Regardless of all of these reports that Apple has cut iPhone production by 75 percent, regardless of reports, and rumors of reports of Apple's untimely death. Regardless of everything you hear from analysts, fund managers CNBC or anyone else for that matter. The fact remains that Apple consistently beats its own revenue guidance by the same exact 12-18 percent every single quarter. The rest is all noise intended to do nothing else but to distract you.

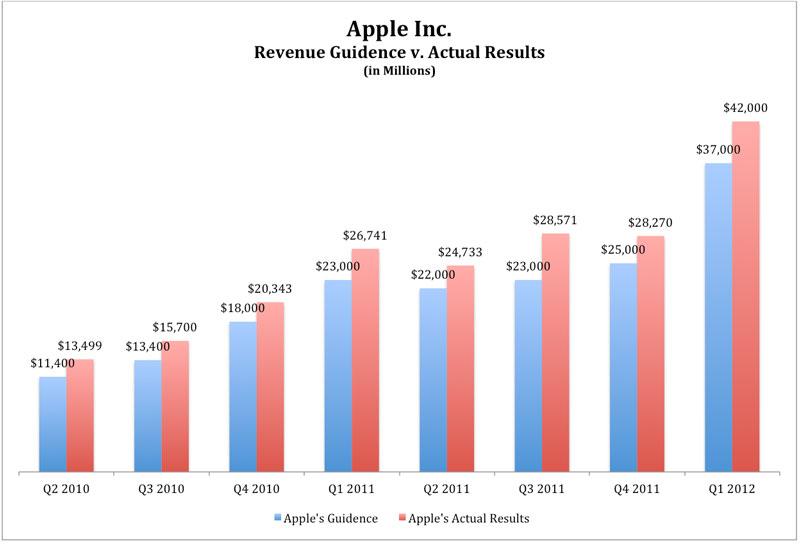

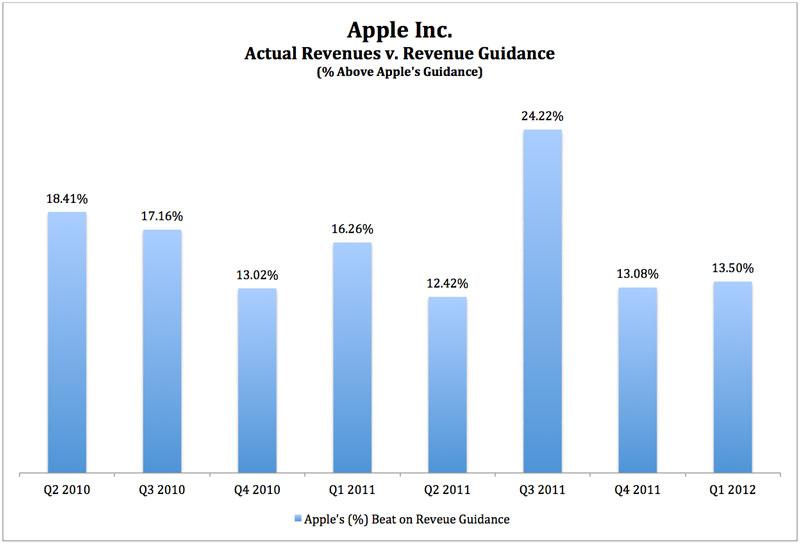

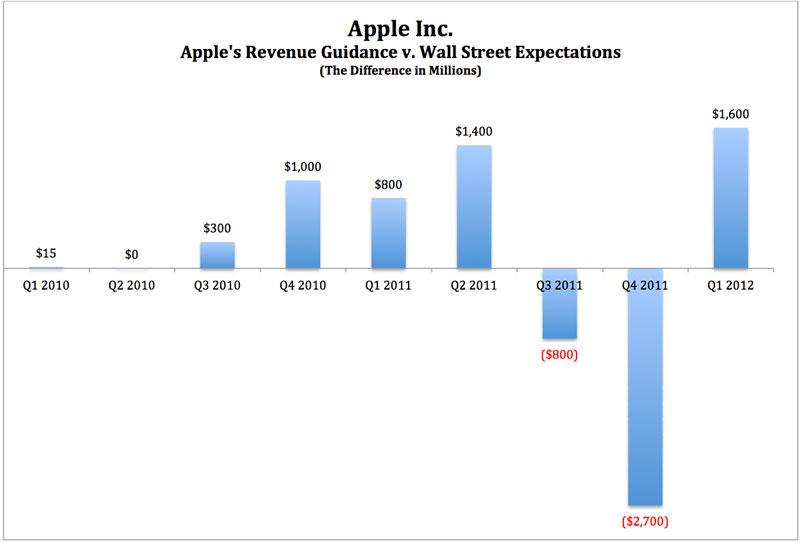

Half the time Apple beats its revenue guidance by 12-13 percent and half the time Apple beats its revenue guidance by 16-18 percent. The only exception came in fiscal Q3 2011 when Apple beat its revenue guidance by 24.22 percent. The charts below show the difference between Apple's actual revenue and Apple's guidance.

The reason Apple regularly beats its revenue guidance so consistently between 12-18 percent every quarter is the fact that of any entity, research group, analyst or fund manager, Apple's management is by far the best positioned to know exactly how the company will perform in any given quarter. In fact, Apple probably possesses on the order of 20-30 times more information than everyone else put together.

Being so well positioned, what Apple does before offering it's sales guidance is it formulates a conservative internal outlook. After doing so, Apple then offers a guidance number that is just about 10 percent below that internal sales expectation.

Good conservative accounting practices dictates that if and when a company decides to offer guidance on its sales expectations, the company must provide an outlook that is reasonably conservative, consistent and comparable across quarters. The expectation set by the company must allow the average analyst to reasonably infer what is likely to unfold. Both reported financial statements and unaudited financial forecasts must be reported consistently across quarters, comparable across quarters and conservative across quarters.

Thus, Apple ultimately ends up offering a guidance number that is 12-18 percent below what it ends up reporting. The reason for this is simple. As with any other company, Apple's internal expectations tend to be slightly conservative. So when the company offers a sales estimate that is roughly 10 percent below its internal expectations, those internal expectations are already slightly conservative leading to the ultimate 12-18 percent beat.

Consequently, any good analyst doing even a modicum of research would understand immediately that when Apple offers revenue guidance, it is essentially telling the Street that it should expect sales to come in around 12-18 percent above that estimate. An analyst that forecasts a sales estimate higher than 16-17 percent above Apple's guidance is being overly optimistic and setting Apple up to fail. An analyst publishing a revenue estimate lower than 10 percent below Apple's guidance is setting the bar too low.

Good conservative forecasting practices dictate that a sales forecast should fall between 12-14 percent. Any lower and you're being unrealistic. Any higher and Apple will generally fall short of your expectations on a regular basis.

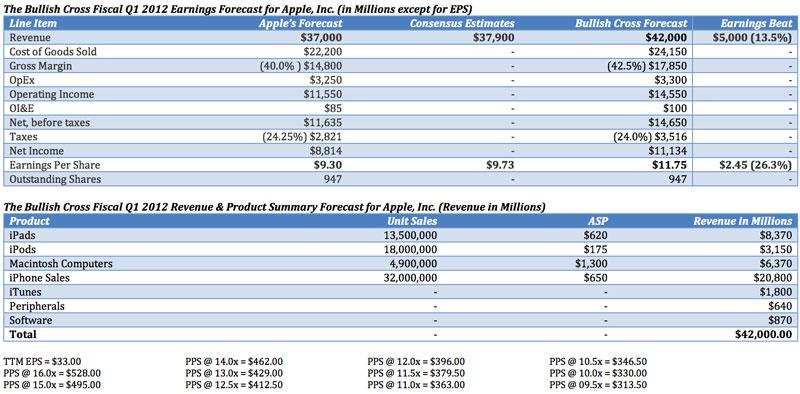

Apple guided revenue to $37 billion for fiscal Q1 2012 which is expected to be released sometime in the third week of January. Based on Apple's history of offering revenue guidance that is 12-18 percent below what it generally reports, that would suggest that Apple will report between $41.5 billion and $43.7 billion in revenue.

Bullish Cross expects Apple to report $42 billion in revenue in fiscal Q1 2012. That is precisely 13.51 percent above Apple's revenue guidance for the quarter and based partly on the extrapolation of certain inferences derived by analyzing Apple's gross margin guidance.

If Apple reports on the higher end of its range, it will result in Apple exceeding our expectations by 4.01 percent. If Apple reports at the lowest end of our expectation, we will have missed Apple's revenue by $500 million or just about 1.19 percent. So that puts us in a position to forecast Apple's revenue almost perfectly in a range of -1.2 percent to 4.0 percent. That's a very reasonable margin of error for a forecast on sales.

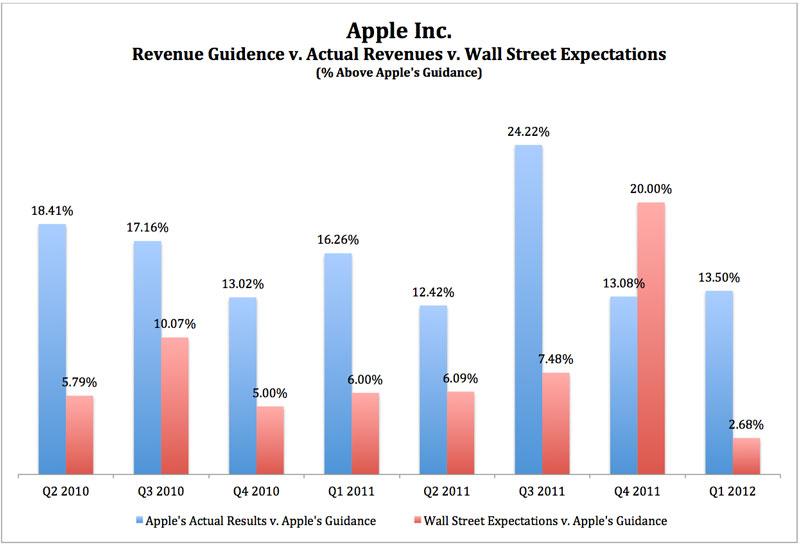

Finally, as a side-note, some people believe that the reason Apple missed on revenue expectations in fiscal Q4 was either due to a slowdown in sales or due to the fact that Apple somehow was more aggressive with its guidance. Yet, I find that interesting given that Apple reported a 13.08 percent beat on its revenue guidance which falls right within the normal range. The only thing out of the ordinary in fiscal Q4 was the fact that the Wall Street consensus was nearly 20 percent above Apple's guidance. That would have amounted to a miss in 7 out of the last 8 quarters. Moreover, what was very odd about that consensus estimate is the fact that it was more than two times higher than usual. It seems like Apple was set-up to miss pretty much no matter what. See the chart below:

I also find it quite fascinating that people try to argue that Apple's guidance has become “more aggressive†for fiscal Q1 just because Apple guided above the street on revenue. Well this isn't the first time that Apple has guided above the street. In fact, Apple has guided above the street on revenue in 6 out of the last 8 quarters. Since Apple underwent its accounting change in fiscal Q1 2010, the company has steadily offered revenue guidance way above the street. And in four out of the last six quarters, Apple has offered revenue guidance that was either very close to $1 billion above the street, or far more than $1 billion above the street. Moral of the story. Stop listening to morons that don't know jack about Apple's guidance i.e. the financial press and the SA average contributor:

We're going to spend a lot of time on this issue of Apple supposedly getting aggressive with its guidance in article we will be publishing later on in the week. For now, we're going to continue discussing how to properly use Apple's guidance to accurately forecast its earnings and why EPS guidance is meaningless.

2. Gross Margin Tells the Story of the Sales Breakdown

One thing that Apple doesn't really tell you in its guidance is how many iPhones, iPads, Macs and iPods the company expects to sell. At least not directly. While Wall Street analysts pretty much waste a lot time on the conference call trying to get Apple to give up information about how the company feels about iPhone sales or iPad sales or Mac sales etc., the company has already indirectly told anyone intelligent enough to understand the subtleties in Apple's gross margin guidance.

This is probably one of the most complex, subtle and intriguing things in financial accounting and analysis. It is the reason Bullish Cross has been far more accurate than Wall Street in forecasting Apple's earnings over the years and it is the reason Bullish Cross is able to consistently forecast Apple's unit sales.

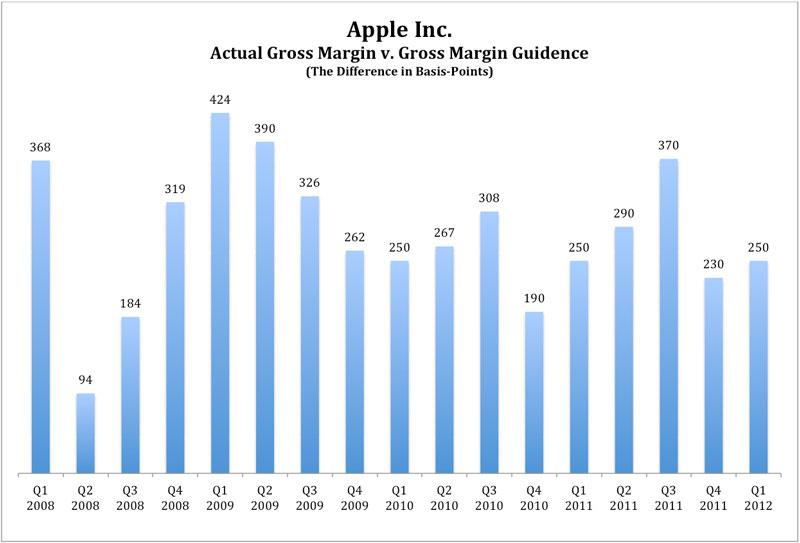

What you have to understand about Apple's gross margin guidance is that Apple almost always guides at least 200 basis-points below what it actually expects to report. In fact, in the last 14 quarters, Apple's guidance came in less than 200 basis-points above Apple's guidance a whopping one time out of fourteen quarters. In fiscal Q4 2010, Apple's gross margin percentage came in at exactly 190 basis points above Apple's guidance. See below:

Yet, normally what you tend to see is Apple guides between 250 and 300 basis points below what it actually reports. In fact, in 8 out of the last 10 quarters i.e. since Apple underwent its major accounting change — the company has reported a gross margin percentage number that was at least 250 basis points above its revenue guidance — one quarter came in at 230 basis points and the other was 190 basis points above. See the table above.

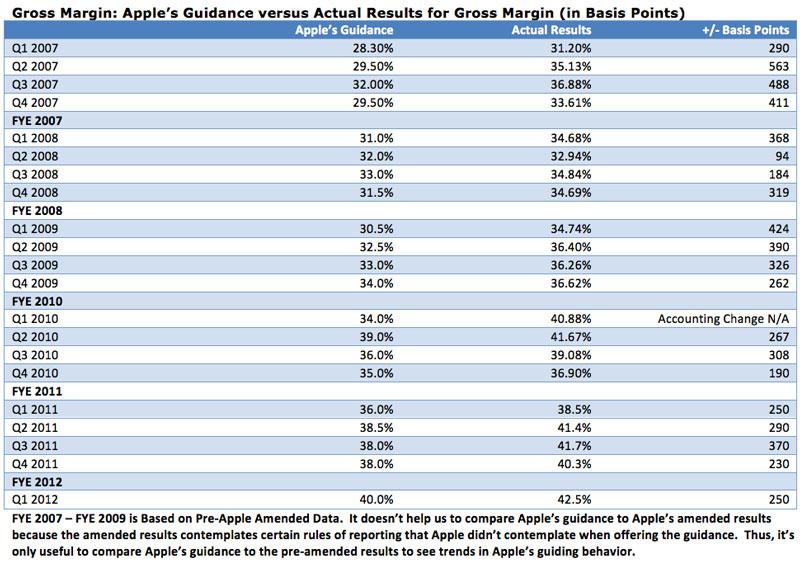

So what you can conservatively infer here is that Apple will probably report a gross margin percentage that is just about 250 basis points above its guidance. In fact, if you look at the seasonality, here's what Apple has done in previous fiscal Q1′s. In fiscal Q1 2011, Apple reported a gross margin percentage that was exactly 250 basis points above its guidance. In fiscal Q1 2010, Apple reported a gross margin percentage that was exactly 250 basis points above its guidance. In fiscal Q1 2009, Apple reported a gross margin percentage that was 424 basis points above its guidance and in fiscal Q1 2008, it reported a gross margin percentage that was 368 basis points above its guidance.

From analyzing these numbers, a very strong case can be made that Apple will report a gross margin percentage that is at least 250 basis-points above its guidance if not slightly more. For fiscal Q1 2012, Apple guided for a 40.0 percent gross margin percentage. Thus, Bullish Cross holds the expectations that Apple will report a gross margin percentage of exactly 42.5 percent on the quarter.

That means taken together with our revenue expectations of $42 billion, it gives us three different line items in our forecast for Apple's fiscal Q1. It gives us (1) Revenue at $42 billion, (2) the Cost of Goods Sold or “COGS†at $24.15 billion; and (3) Gross Margin at $17.85 billion or 42.5 percent of revenues.

Bullish Cross Fiscal Q1 2012 Earnings Forecast for Apple, Inc (in Millions except for EPS)

Revenue: $42,000

Cost of Goods Sold (COGS): $24,150

Gross Margin: $17,850 (42.5 percent)

Now the next thing every good analyst should understand immediately is that the iPhone carries the highest gross margin percentage by far. The more Apple's revenue is driven by iPhone sales, the higher Apple's gross margin percentage will be.

Apple's two main revenue drivers are iPhones and iPads. While iPads do carry a pretty solid gross margin percentage, it is nowhere near as profitable as the iPhone. Apple's third biggest revenue driver is Macintosh sales. Everything else is nonsense.

Thus, using some relatively basic algebra, it is very possible to determine how Apple envisions the product mix between iPhones and iPads to look like simply by analyzing the gross margin percentage on the quarters. Now if Apple does in fact report a 42.5 percent gross margin number, that would the highest gross margin percentage in the company's history by far.

And no one should be shocked by this fact for at least three major reasons. First, Apple is giving the most aggressive gross margin percentage guidance it has ever given in its history. Just for comparison's sake, in fiscal Q4 Apple guided gross margin to 38 percent. In fiscal Q1 of 2011, it guided gross margin to 36 percent.

So just from Apple's gross margin guidance alone, no one should be shocked when Apple reports a record high gross margin percentage. The second big reason that no one should be shocked by Apple's gross margin percentage guidance is the fact that Apple just guided revenue to $37 billion. You know how freaking high that is? That's $10 billion above what it just reported in fiscal Q4 2011 and 50 percent higher on a year over year basis. So it shouldn't be surprising to see Apple report a 42.5 percent – 43.5 percent gross margin number.

Thirdly, with the iPhone 4S just being released, it is obvious this quarter's revenue is largely driven by iPhone sales. As revenue increase and as the distribution of revenue is attributed more proportionately to iPhone sales than iPad or Mac sales, Apple's gross margin increases.

What Apple basically told us with its revenue guidance + gross margin guidance is that the company expects to report a huge revenue number and it expects that revenue number to be driven primarily by iPhone sales. In fact, while I don't want to spend the time explaining the math in this particular article, Apple's guidance suggests sales of 32 – 35 million iPhones, 13.5 – 14.5 million iPads and 4.9 million Macintosh Computers. For those who want to see our completely methodology, you can do so by visiting some past earnings previews published at Bullish Cross. But this article is supposed to be all about forecasting an income statement using nothing but guidance and historical data.

So we're not going to have a detailed discussion about the breakdown in terms of sales. Though I will post the sales breakdown, and how we arrive at our revenue expectation below. For now, what you should take from Apple's gross margin guidance is that (1) Apple tends to report a gross margin number that is about 250 basis-points or above its guidance which suggests Apple report a 42.5 percent gross margin percentage; (2) Apple's gross margin guidance is the highest in the companies history which suggests Apple should report a record revenue number and a record gross margin percentage number; (3) Apple's gross margin guidance suggests Apple is very dead serious about its revenue guidance. If Apple was even slightly hesitant about its sales expectations, it wouldn't have guided gross margin to 40 percent. It means Apple stands squarely behind its revenue guidance.

Wall Street believes Apple has become conservative with its guidance for the dumbest f'ing reasons you could ever imagine. After getting overly aggressive with its guidance in fiscal Q4, now Wall Street has turned the wheel just as hard in the opposite direction and has guided only 2.68 percent above Apple's revenue guidance. This is going to lead to the largest blowout in company history. We will discuss why in an article later this week.

But now let's turn to operating expenses which will give us the next two line items in our income statement forecast.

On page three, how operating expenses are only a small fraction of Apple's revenue.

3. Operating Expenses: Only a Small Fraction of Apple's Revenue

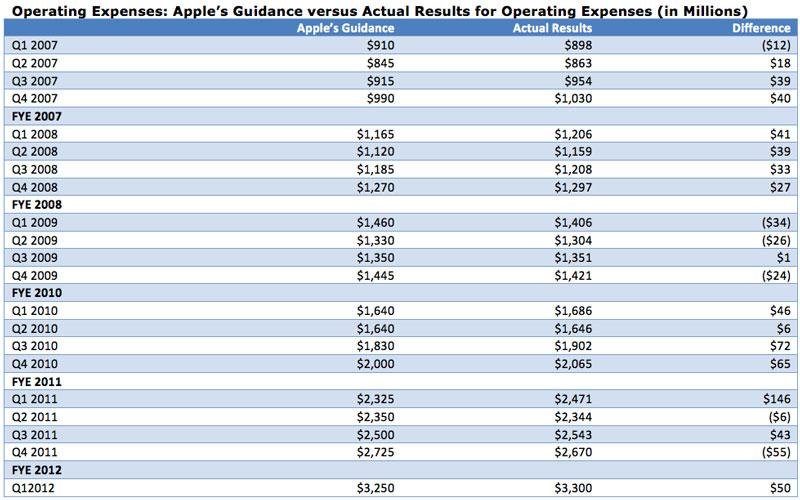

Like with other line-items in Apple's guidance, there is a very consistent trend here. Apple pretty much always tends to deliver an operating expense number that is just about $50-$60 million above or below its forecast. For example, in fiscal Q4 2011, Apple guided operating expenses to $2.725 billion and came in at $2.67 billion which was $55 million below its forecast. It's a pretty negligible number overall.

Because of the holiday shopping season, there has been a historical tendency for Apple to actually overshoot on expenses. What we've seen happen is Apple report an OpEx number that is about $50 million above what guided. Yet, in the last 20-quarters, there is only 1 instance where Apple's operating expenses fell outside of this $50 million +/- range. For whatever reason, Apple reported operating expenses of $146 million above its guidance in fiscal Q1 2011. But if you go back to previous fiscal Q1′s, it was $46 million in Q1 2010, -$34 million in Q1 2009 and +$41 million in 2008.

If one wanted to be very conservative, he or she would forecast operating expenses to come in about $100 million above Apple's forecast. But I think a very strong case can be made that Apple really intends to come in above $50 million above what its guiding. That fiscal Q1 2011 is truly just an outlier. And in fact it is given that it's only happened once in twenty quarters or 5-years.

For fiscal Q1 2011, Apple's guiding for $3.250 billion in operating expenses. Bullish Cross expects Apple to report that operating expenses rose to $3.3 billion versus $2.471 billion in the year ago quarter.

Now let's add this line item to our developing forecast. In fact, we can add two line items. Operating Expenses are those expenses that are necessary for the running of the business. They include things like selling, general and administrative expenses and the cost to do research. Anything related to running the Apple operating falls under this expense category.

In order to get operating income, one needs only to merely subtract operating expenses from gross profit/gross margin. Remember gross margin is the profit Apple makes on each device it sells before taking out expenses to run the operation. So for example, if it costs $200 to make an iPhone and Apple is selling that iPhone for $600, then Apple is making a gross profit or gross margin of $400. Operating expenses are those expenses needed to take the iPhone and put it in the hands of the consumer by hiring people, renting retail stores etc. etc. Ok. So we have two line-items to add to our income statement forecast. (1) Operating Expenses and (2) Operating Income. In this case, operating income is $14.55 billion.

Bullish Cross Fiscal Q1 2012 Earnings Forecast for Apple, Inc (in Millions except for EPS)

Revenue: $42,000

Cost of Goods Sold (COGS): $24,150

Gross Margin: $17,850 (42.5 percent)

Operating Expenses: $3,300

Operating Income: $14,550

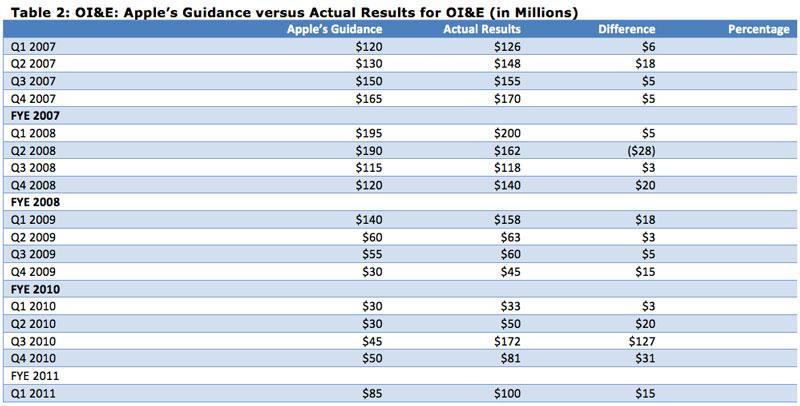

4. OI&E: A sleeper in buffing EPS

In the past, OI&E used to dramatically impact EPS in a pretty significant way. Sometimes you would see a 10 percent increase in EPS just as a result of OI&E. In fact, I remember times where Apple decimating Wall Street expectations only because OI&E came in a lot higher than anyone expected. It's not so big of a deal these days even though Apple could make it a big deal if it wanted to with those trillions of dollars it has sitting there in its coffers.

In the typical quarter, Apple tends to beat its OI&E guidance by between $5 million and $20 million. There is one outlier in fiscal Q3 2011 where Apple reported $127 million which was a big contributor to the huge EPS beat it delivered. But in most cases, it's a $5 – $15 million difference. Recently, however, we've seen a bigger trend. For example, in four out of the last five quarters, Apple has delivered an OI&E number that was $15 million or more above its guidance. It also offering the most aggressive OI&E guidance in nearly two years this quarter.

For this reason, we're expecting Apple to deliver a $15 million beat on its OI&E guidance this quarter. Apple guided OI&E to $85 million for fiscal Q1 and Bullish Cross is expecting OI&E to come in at an even-Steven $100 million.

For those who are curious, OI&E stands for “Other Income & Expenditures.†The reason Apple breaks this income off into its own category is very simple. It would be deceiving for any company to include that number in their revenue.

The reason for that is the fact that OI&E is income received from its secondary operations. Apple is in the business of selling iPhones, iPads, Macs and iPods. It's not in the business of investing. At least not primarily. If Apple were to make a windfall one quarter, it would be unfair to investors to flaunt that number around as part of its revenue if Apple didn't derive that revenue from the things it normally sells. So OI&E under GAAP-accounting is generally broken off into its own category.

Now when you add OI&E to operating income, we get net income. Hurray we're almost there! So we have two line-item to add to our forecast and we're almost done. We have to add OI&E and Net Income before Taxes.

Bullish Cross Fiscal Q1 2012 Earnings Forecast for Apple, Inc (in Millions except for EPS)

Revenue: $42,000

Cost of Goods Sold (COGS): $24,150

Gross Margin: $17,850 (42.5 percent)

Operating Expenses: $3,300

Operating Income: $14,550

Other Income & Expenditures: $100

Net Income, Before Taxes: $14,650

5. The Tax Rate: Apple Pays Like No Taxes

One of the largest companies in the world, and Apple pays half the tax-rate that I pay to Uncle Scam. Pretty amazing isn't it? Now I don't want to spend an incredible amount of time explaining the historical trend when it comes to the tax rate. Suffice it to say that there is consistent trend when it comes to Apple's tax-rate guidance.

Generally speaking, Apple tends to report a tax-rate that is about 250 to 500 basis points below its guidance. Yet, very recently, Apple just started getting very realistic with its guidance. For the longest time, I had an edge on Wall Street on this issue. The tax rate does have a huge impact on EPS too so if you had an edge in being able to accurately forecast the tax rate, you were generally at a massive advantage on everyone else.

This quarter, I think Apple is pretty much guiding in-line with what it will actually report in terms of the tax-rate. Apple guided the tax rate to 24.25 percent and I expect the company to report roughly 24.0 percent in taxes this quarter. Though I should note that in fiscal Q3 Apple reported a 23.5 percent tax rate and in fiscal Q2 it reported a 23.7 percent tax rate. And Apple does indeed have a tendency to sandbag on the tax rate. So we could very easily see a 23.5 percent tax rate for fiscal Q1 since Apple pays taxes at the poverty level.

And there you have it. Bullish Cross expects Apple to report a 24.0 percent tax rate for fiscal Q1 2012. Thus, we can add two more line items to our developing income statement. First we can add the amount Apple will pay in taxes which is nothing more than multiplying 24 percent to $14.65 billion in net income before taxes. That number happens to be $3.516 billion. If you subtract the tax rate from Net Income before Taxes, you get the bottom-line i.e. Net Income. Thus, Bullish Cross expects Apple to report $11.134 billion in net income for fiscal Q1 2012. See below:

Bullish Cross Fiscal Q1 2012 Earnings Forecast for Apple, Inc (in Millions except for EPS)

Revenue: $42,000

Cost of Goods Sold (COGS): $24,150

Gross Margin: $17,850 (42.5 percent)

Operating Expenses: $3,300

Operating Income: $14,550

Other Income & Expenditures: $100

Net Income, Before Taxes: $14,650

Taxes: $3,516 (24.0 percent)

Net Income: $11,134

6. Earnings Per Share Guidance: Why it is completely meaningless, random and useless

The only thing that Apple's EPS guidance is good for at all is being able to infer the number of shares that will be outstanding in fiscal Q1 2012. What you have to understand is that Apple introduces new shares all of the time which leads to a quarterly increase in the number of shares used in the calculation of diluted EPS. Based on Apple's EPS guidance this quarter, we are able to infer with a very high level of accuracy the number of outstanding shares Apple will have in fiscal Q1 2012. That number happens to be 947,000,000 shares.

In order to arrive at our final line-item, all we have to do is divide net income by the number of diluted shares that will be outstanding in fiscal Q1 2012. In this case, that means dividing $11.134 billion in net income by 947 million shares. Doing so will give us $11.75 in earnings per share (EPS).

Currently, Apple guided that it will report $9.30 in EPS, Wall Street expects Apple to report $9.73 in EPS, and Bullish Cross expects Apple to report $11.75 in EPS. That EPS number would match the largest EPS blowout of Wall Street estimates in Apple's history.

The table below outlines the Bullish Cross Outlook for Apple's Fiscal Q1 2012. Notice that this table also displays a product breakdown which we arrived at only after doing an analysis that was on the order of 3-4 times greater that what we've outlined in this article. It's an entirely different type of analysis only based in part on this guidance analysis. Yet, the difference between Bullish Cross and Wall Street is that we're not guessing what Apple reported in sales. We know that the revenue number will be around $42 billion. It's just a matter of doing the requisite analysis necessary to know precisely how that revenue will be derived.

As a side note, I think it is also very important to note that based on our earnings forecast, Apple's trailing 12-months of earnings will rise very dramatically to $33.00 in fiscal Q1 which is 19.18 percent higher than it is today. If you're an Apple investor, I hope you understand the gravity of what that means. What this means precisely is that in order for the stock to maintain its current very depressed valuation, the stock would have to rise 19.18 percent after earnings. Notice that is merely just to maintain the current crap-valuation it has been getting.

As of the close of trading on Thursday, Apple trades at a 14.11 P/E ratio. In order for the stock to maintain that 14.11 P/E ratio, the stock will have to rise $465.63. That's just to maintain a 14.11 P/E ratio. If the stock trades at $390 a share after earnings, the stock's P/E ratio will collapse to 11.82. Apple's P/E ratio can only contract so far before it gets to 0. This pace of minute 2-points every quarter on the P/E ratio is unsustainable. Something is going to give and soon. You don't want to be short like Steve Cortez when it does. He's going to get massively blindsided like Whitney Tilson on the Netflix short. The difference is that Whitney Tilson is actually a smart guy.

Now that we've demonstrated how one can build a net-income statement forecast using each element of Apple's guidance except for EPS, let's now discuss why EPS guidance is entirely random, meaningless and useless

As we demonstrated above, each item in Apple's guidance has a level of intentionality to it. Apple intentionally guides gross margin about 250 basis points below what it actually reports. It guides revenue between 12-18 percent below what it actually reports. Intentionally as we demonstrated above. It intentionally guides operating expenses +/- $50 million above or below its guidance. It guides OI&E just about $15 million below what it actually reports. It guides the tax rate in-line.

But notice that Apple's EPS guidance is a sum amalgamation of the different line-items in the overall guidance. Just as Apple doesn't give guidance for operating income, cost of goods sold, net income before taxes and net income, it really shouldn't give guidance for EPS. EPS is just a result. It's not an intentional number.

If you gave me each element in Apple's guidance including its shares outstanding, I can tell you exactly what it's EPS guidance is. And that's because Apple's guidance has to be internally consistent. Meaning, it can't give an EPS that doesn't compute mathematically with the other line items. In that sense, the EPS guidance is dependent on the other line items.

That is PRECISELY why Apple tends to beat its EPS guidance by an outrageously large range. If you look at Apple's EPS beats on its guidance, it's been anywhere from 20 percent to 60 percent. That's because Apple isn't intentionally giving you that guidance number. Unlike every other line item, there is no consistent pattern to Apple's EPS guidance. One quarter Apple beats EPS guidance by 54.9 percent and in the very next quarter it beats EPS guidance by 28.2 percent.

If Apple guided gross margin to 43 percent this quarter, Apple's EPS guidance would be much higher. If it guided gross margin guidance to 41 percent, Apple's EPS guidance would be much lower. As you saw in the analysis we outlined above, Apple's EPS guidance is highly dependent on how each of these different line-items in the income statement work together.

It's all about proportions. But rest assured, Apple could deliver a 28.2 percent beat on its EPS guidance in one quarter which results in a massive miss and it can do so in a different quarter which would result in a huge blowout. In fact, that's precisely what's going to happen in here.

In fiscal Q4, Apple beat its own EPS guidance by 28.2 percent. For fiscal Q1, Bullish Cross is expecting Apple to beat its EPS guidance by a lower 26.3 percent. Yet, we believe that in fiscal Q1 it will amount to one of the biggest if not the biggest earnings blowout in company history whereas in fiscal Q4 it resulted in a huge earnings miss.

That's because what matters here is not how much Apple beats its own EPS guidance but how much it beats Wall Street expectation. Now the reason I went through all of the trouble to point out that Apple's EPS guidance is meaningless is because too many people in the financial press have been recently spreading some very piss-poor research that is starting to mislead the public at large. Hopefully this report will help clear up this issue.

Andy M. Zaky is a fund manager at Bullish Cross Capital and the editor of the Bullish Cross Financial Newsletter. Bullish Cross Capital owns a significant long position in Apple, Inc.

Malcolm Owen

Malcolm Owen

Chip Loder

Chip Loder

William Gallagher

William Gallagher

Christine McKee

Christine McKee

Michael Stroup

Michael Stroup

William Gallagher and Mike Wuerthele

William Gallagher and Mike Wuerthele