In a research note on Thursday, Piper Jaffray analyst Gene Munster said buy-side investors' concerns that Apple's gross margin will see a two-year decline to below 30 percent is unlikely, specifically noting the company's important iPhone margins are stable.

Munster believes investors are unduly worried about an Apple margin dip as the company prepares to enter the mid-tier smartphone market with a rumored low-cost iPhone. Such a device, the argument goes, will cannibalize the flagship iPhone's market share and pull down overall gross margin, as the handset is a major profit driver for Apple.

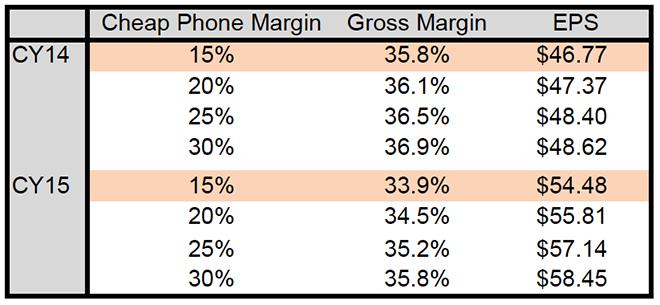

"We believe concern that margins will drop below 30% in the next 2 years is overblown," Munster wrote in the report shared with AppleInsider. "While we believe iPhone margin is stable, we can build a case for a 32% gross margin in 2015 (Street at 37%), but it would require a nuclear meltdown in Apple's model including 50% cannibalization of the regular iPhone from the cheaper iPhone, a 15% margin on the cheaper phone, and a 10% margin on the TV."

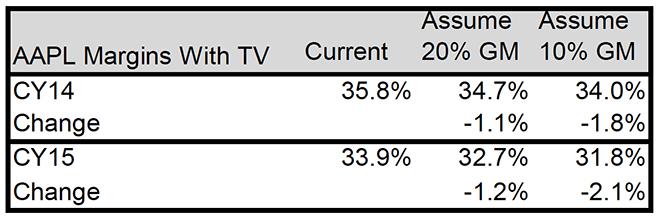

Munster is referring to a much rumored television set Apple supposedly has in the works, a traditionally low-margin consumer product.

The analyst currently sees iPhone margin at about 55 percent despite Apple's drop in gross margin from 42.8% in June 2012 to 37.5% in March 2013. According to Munster, the downturn the most recent quarter was likely a product of strong iPad mini sales and an estimated $414 million hit from the combination of new Chinese warranty policies and what Apple called an "unfavorable adjustment."

Going further to prove that iPhone margins are stable, the analyst calculated what Apple's margins would look like if no iPad minis were sold from December 2012 to March 2013. The result was a rise in overall gross margin, from 39.7 percent to 40.2 percent over that period.

As for the effect of a low-cost iPhone, Munster is modeling sales at 50 million units for 2014, and 100 million units in 2015, down 25 million each year because the handset has yet to materialize. With an implied 50 percent cannibalization rate to the full cost iPhone, up from the analyst's prior estimates of 30 percent, and an adjustment in margin from 15 percent to 30 percent, the net result is an overall margin reduction of 40 basis points in 2014 and 140 bps in 2015.

Here Munster notes that if the cheaper iPhone turns out to be more successful than the expected 7 percent marketshare for 2014, the impact to Apple's overall margin could be greater. In that case, however, a hit to margins would also result in positive profit growth.

Despite modeling a conservative 15% gross margin for the low-cost iPhone, Munster offers a "more realistic" estimate in the chart above. | Source: Piper Jaffray

Munster also sees some investors thinking that Apple will one day degrade to Samsung's operating margins, which stood at 14 percent for the 2012 calendar year. Because the Korean company produces a wide range of products, the electronics division alone making everything from TVs to washing machines, the comparison is flawed.

Adding to the argument is a favorable component pricing environment going forward, something that Apple CFO Peter Oppenheimer alluded to during the company's most recent quarterly earnings conference call.

Regarding an Apple television, Munster doesn't expect such a device to enter the picture until 2014 and has thus not included it in his model. He expects an announcement to take place at the end of the year, with shipments going out in 2014, with a selling price of $1,500. Margins could be as high as 20 percent, but normally TVs carry gross margins of 10 percent or below.

Given the new model, Munster is maintaining an Overweight rating for AAPL, but is adjusting his price target to $655 from $688 due to 5 percent lower earnings per share estimates for the 2014 calendar year.