When Apple rolls out a rare new product— rather than canceling it internally— you'd have to be naive to think it was rushed to market without much consideration and therefore probably doomed to failure. But you'd be equally naive to think that the incumbents positioned in the path of Apple's next potential juggernaut wouldn't desperately seek to defend their turf, bending the truth to the breaking point if necessary.

Apple Pay— the fingerprint-authenticated, card-free payment system that blocks retailers from gaining access to more than just your money when you make a purchase— has offended a broad swath of status quo moneychangers and their consultants, from retailers who profile their shoppers to create marketing dossiers (like MCX CurrenC) to various outfits that are trying to sell their own methods for paying without cash.

PayPal dumps on Apple Pay, then offers to support it

The first attack on Apple Pay came within a week of its appearance, hurled by the fraud experts at PayPal— a grotesquely incompetent operation that understands fraud in the same intimate way that Bill Gates knew how to play Monopoly.

When PayPal implied that Apple couldn't be trusted with electronic payments because the company didn't somehow stop celebrities from saving their private nudie pics to iCloud using account passwords that were too easy to guess, even the firm's former senior executive Keith Rabois was quick to point of what a steaming load his former employer was feeding the media.

PayPal was obviously threatened by the appearance of Apple Pay— but at the same time, the company's subsidiary Braintree was advertising that it could help developers process secure Apple Pay transactions, making it clear that PayPal knew that Apple Pay was in no way insecure when it bought a full page of the New York Times to advertise the idea that perhaps there were reasons to be afraid of Apple Pay, while trusting its own notoriously flawed and hassle-ridden PayPal.

Google failed at it first, as it so often does

Android fans also took umbrage at the attention Apple Pay was getting, considering that Google Wallet had blown out an NFC mobile payment scheme years ago in 2011, and Motorola had introduced a phone with a fingerprint scanner earlier that same year— four years before iPhone 6.

One problem was that nobody in Android land had put those two things together, nor had enough work gone into either project to make either one of them really usable or even reasonably functional. Motorola's problematic Atrix fingerprint scanner was abandoned before the year was out, never to return again.

Google Wallet limped along with the enfeebled vigor of Google Plus, even as the company kept eliminating core support for it on its own Nexus devices, while changing the definition of "Wallet" to find some part of the wall where it might stick, if thrown hard enough.

Most recently, Samsung (i.e., half of Android) split from Google to introduce its own new Samsung Pay product, incorporating legacy LoopPay hardware that hacks card swipers into thinking you have an old fashioned magswipe card. Alistair Barr, writing for the Wall Street Journal gushed that Samsung's feature, tied exclusively to its 2015 flagship phone, was "looking to outsmart Apple," and Google Wallet as well.

It's interesting how the market share of Samsung's not-yet-on-sale Galaxy S6 (succeeding the black hole in collapsing sales of previous premium Galaxy products) isn't even considered in the puff piece, while the same authors and their colleagues have incessantly told us that iOS has minority market share in the global market for phones, and is perhaps on the brink of commercial irrelevance if you take numbers from Gartner, IDC and Strategy Analytics as anything other than powerpoint spin-doctoring and client-flattery.

Certainly if the whole pantheon of Android— with all the support Google can muster— can't successfully deploy a mobile payment system across four years of trying, one luxury-priced phone released by Samsung should do the job of containing the spread of Apple's success, right? Kind of like how Adobe Flash Player, VP8 and QWERTY keyboards really blew Apple right out of the water.

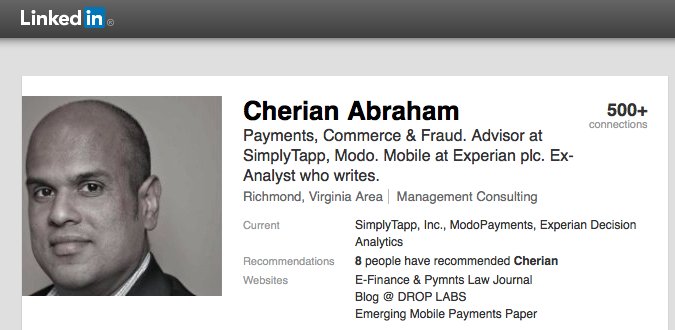

Cherian Abraham, Apple Pay fraud expert and Apple Pay competitor

Now imagine being a consultant tasked with propping up the relevance of the Host Card Emulation technology created to save Google Wallet, while at the same time backing a variety of Android-centric mobile payment platforms erected in the path of Apple Pay, and watching as everything you're deeply invested in turns brown while nearly every bank in America advertises your competitor.

That's the position Cherian Abraham found himself in. According to his LinkedIn profile, he sits on the advisory board of SimplyTapp and MondoPayments, and leads mobile commerce and payments at Experian Global Consulting.

Rather than buying full page ads in the New York Times to passive-aggressively vilify Apple Pay, Abrahams published a series of blog entries inventing the idea of "Apple Pay Fraud" until they were picked up by the rebloggers at the Wall Street Journal, LA Times, and a series of other former newspapers that have recently converted into third rate-blogs still wrapped in the credentials of their former journalistic identities like a stinking fish carcass.

Shame on the Wall Street Journal

The editorial staff of the Wall Street Journal— and by "editorial staff" I mean "rubberstamping committee of all the slanted reporting that can be dredged up"— hasn't yet hit rock bottom in its crusade to present the world's most successful technology company — the most valuable public corporation in existence— as an enfeebled "haunted empire" that makes too much money due to its IDC market share problems and its failure to give away its hardware or software in the manner than clearly isn't working for the Samsung and Google horses that Wall Street Journal writers have historically placed all their bets on, foolishly and naively.

Given my deadline for producing this editorial before Apple releases more stuff tomorrow, I cannot even concoct a sentence that effectively communicates the depth of the ridiculous and embarrassing unprofessionalism of a newspaper that has demonstrated such ignorant hostility and contempt for perhaps the most competent American company of our generation.

For a paper that bends over backward to make excuses for the economic collapse caused by unregulated bankers and which once staunchly defended Microsoft at its monopoly trial, you might imagine that Apple's prowess in capitalism would at least earn it neutral coverage in the Wall Street Journal, considering that Apple's primary competition is Google's communal knockoff platform aimed at facilitating China's copying of the iPhone— even as Google miserably fails to recover any profits from its busywork.

Instead, Daisuke Wakabayashi, the same Wall Street Journal reporter who for years carried water for Samsung and its supposed ability to "innovate"— at least until that company's profits imploded and it revealed beyond a doubt that its real source of innovation is in copying Apple's previous generation of products (not, as it testified under oath in the infringement case hosted by Judge Lucy Koh, "a bowl of water")— is now rushing to tell us that fraud has "come to Apple Pay."Rather than describing Abraham as a consultant and advisory board member of various Android-centric Apple Pay competitors, Wakabayashi only described him "a payment expert."

Except that Wakabayashi's entire report of "fraud" is based upon the creative writings of Abraham, the consultant with so much of his livelihood tied up in Apple Pay's freshly emasculated competitors. Rather than describing Abraham as a consultant and advisory board member of various Android-centric Apple Pay competitors, Wakabayashi only described him "a payment expert."

Only at the end of his piece did Wakabayashi backhandedly mention that Abraham has some connection to SimplyTapp, the HCE provider for Android. Abraham's many other affiliations coloring his "expert" opinion on Apple Pay were not mentioned. None of that made it into the versions of the story published by MarketWatch.

Instead, Wakabayashi tried to suggest that card provisioning performed by banks— who were so eager to partner with Apple Pay that they were allowing a tiny number of previously stolen card numbers to be approved as legitimate— was somehow Apple's problem, and that this "fraud" should be associated with Apple Pay in readers' minds, even though Apple Pay has nothing to do with card provisioning any more than it's Apple Pay's fault if you write "2014" on your checks issued from the same account tied to the card provisioned with Apple Pay on your iPhone 6.

Abraham's original blog entry did actually state "it seems like fraud has come to Apple Pay," but it then backpedaled to clarify that, "No, iPhones weren't stolen and then used for unauthorized purchases, TouchID was not compromised, Credentials weren't ripped out of Apple's tamper proof secure element - nor the much feared but rarely attempted MITM attacks (capture and relay an NFC transmission at a different terminal)." None of that.

"Instead," Abraham wrote, "fraudsters bought stolen consumer identities complete with credit card information, and convinced both software and manual checks that they were indeed a legitimate customer." It wasn't Apple Pay provisioning those cards, it was Apple's partner banks. Abraham certainly understood that, despite his financially-supported, easily discerned bias against Apple Pay. He simply used some weasel wording to set a trap for sloppy journalists searching for a negative story to write about Apple, regardless of the facts.

That raises the question: was Wakabayashi of the Wall Street Journal feigning ignorance, or does he just have incredibly terrible reading comprehension?

Recall this is the same paper that confidently claimed China's Xiaomi had turned itself into a "lucrative business" after its reporters supposedly gained access to "internal documents" indicating the company had earned over a half billion dollars in 2013. The numbers cited by the Wall Street Journal were actually off by an order of magnitude.

Blogs, old media fish-wrap disagree on the nature of Wall Street Journal clickbait

It has to be embarrassing for the Wall Street Journal that even Business Insider managed to get the story right, even if this occured because the site simply republished an article by Rurik Bradbury of Trustev, rather than assigning one of its usual minions the task of brutalizing the public with its typical factually hostile, sensationalized blatherings.

Quartz, on the other hand, published a story by Alice Truong that wept out the headline, "Apple shirks responsibility for fraud happening on Apple Pay," even while also reporting directly from Apple that there wasn't "any breach in any of Apple's systems," and citing a third party expert as saying provisioning fraud "has nothing to do with the breach of the Apple system."

Writing for Macworld, Glenn Fleishman got it right and successfully backed up his clever headline: "Fraud comes to headlines about Apple Pay."

Micah Singleton of The Verge also got the story right, as expressed efficiently in his article's subheading, "The fraud is happening through the banks, not through Apple Pay."

LA Times wraps up fishy coverage of Apple Pay

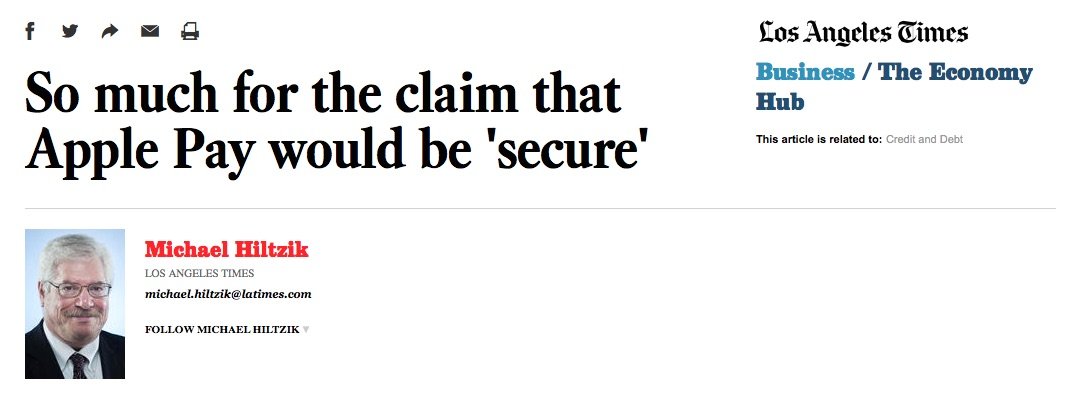

On the other hand, the LA Times version of the story, written by Michael Hiltzik, appeared to be a step backward in basic logic compared even to the Wall Street Journal version.

"So much for the claim that Apple Pay would be 'secure,'" Hiltzik's headline gloated, complaining that Apple had somewhere assured us all that Apple Pay "would be all but immune from fraud." Perhaps even through several generations of relationships in the financial chain, like a magical amulet. Pickpockets? Sorry, I have an iPhone 6 in my pocket! Nobody can even lie to me, because Apple Pay solved fraud for all time!

Hiltzik continued that, "Apple's systems haven't been anything like secure in the past," citing the problems suffered by Wired writer Mat Honan, who tragically lost all of his data because he: didn't ever back up his data; linked all of its online accounts, ranging from Google to Twitter to Amazon to his Apple ID; and apparently stored his unencrypted credentials for Apple ID on Amazon's servers ("Getting into Amazon let my hackers get into my Apple ID account," he wrote).

That was all Apple's fault, in Hiltzik's understanding, due to the company's "not anything like secure" history. Hiltzik also threw in celebrity nudes, PayPal style, for added impact. But as with the topic of security in general, Hiltzik also knew nothing at all about the topic of Apple Pay security in specific, instead merely reblogging, poorly, the story written up by Abraham.

Hiltzik went well beyond merely repeating Abraham, instead improvising his own expert opinion about how Apple was at fault over banks' provisioning. "Apple could have mandated tougher standards on its own, say by refusing to accept cards that hadn't been put through the validation wringer," he wrote, apparently unaware that Abraham has actually written that Apple had "mandated tougher standards" for provisioning weeks before Apple Pay launched.

Abraham had originally expressed the opinion that Apple's rule tightening on card provisioning was tough for banks to meet. But that's not even at issue because Hiltzik clearly doesn't even understand what provisioning is, given his word-spaghetti suggesting that Apple should be "refusing to accept cards that hadn't been put through the validation wringer." He could have written a more sensible paragraph by randomly selecting words suggested by iOS 8 QuickType.

For example, my phone just randomly gave me, "I just got back to sleep now and I don't think that I have a great way for a few weeks of a sudden it was the best of the year." That doesn't exactly make sense, but it makes more sense than Hiltzik's take on Apple Pay. Somewhat ironically, Hiltzik also wrote a piece two years ago titled "How Apple invites facile analysis"

Somewhat ironically, Hiltzik also wrote a piece two years ago titled "How Apple invites facile analysis," with the subheading, "Conjecture and misunderstanding can trump actual knowledge when it comes to evaluating a company; the hubbub surrounding Apple is a case study."

In it, Hiltzik mocked his future self, writing "it's fair to say that on the way to the peak as well as to the trough [of Apple's stock price swings], the punditry — indeed, even the purportedly 'factual' reporting on Apple — has been little more than myth-making."

Along those lines, shortly after Apple Pay premiered last fall Hiltzik also wrote, "What is the problem for which Apple Pay is the solution?" That article conveys a rather clear failure to understand what Apple Pay is, and why banks in the U.S. fell all over themselves to provision a million cardholders before Hiltzik had a chance to rub out another arrogant dismissal of something he doesn't even understand this week.

In any case, a primary antagonist to Apple Pay has managed to poison the internet with ignorant rubbish, all because old media journalists don't care about doing their jobs as long as they can get paid to crank out reams of incompetent garbage. I can't wait to see what they write about Apple Watch tomorrow.