Apple has been dealt another blow to its stock price, as analysts at Piper Sandler have downgraded AAPL to "neutral" over concerns of handset and macro weakness in 2024.

As part of a much larger note seen by AppleInsider, Harsh Kumar of Piper Sandler is discussing the chip market and macroeconomic concerns. Factors specifically affecting Apple are a difficult first-half handset market, and signs of RAM and Flash chip pricing increasing.

"We are concerned about handset inventories entering into 1H24 and also feel that growth rates have peaked for unit sales," Kumar writes. "Handsets are ~51% of total revs."

Other concerns include a deteriorating macro environment on China, which is believed to impact Apple's higher-end iPhone business.

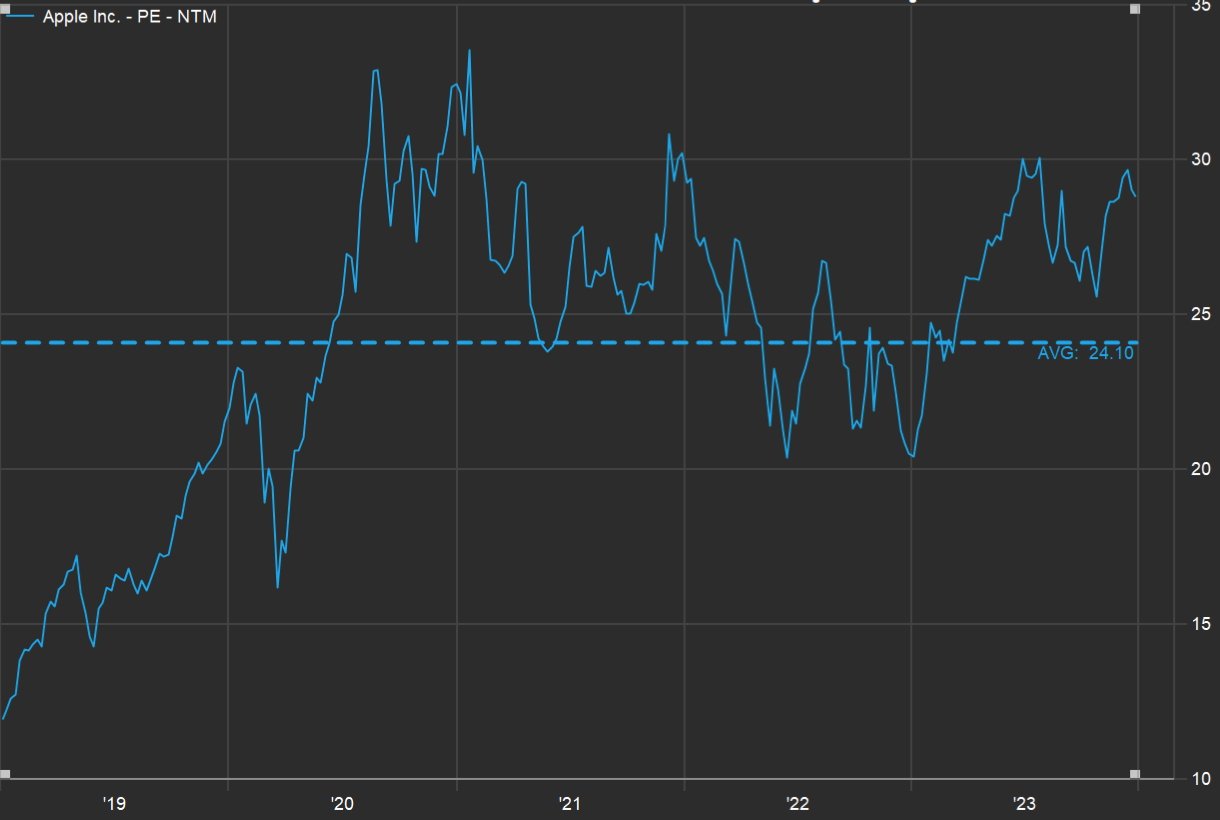

The firm also has valuation concerns, with Kumar noting that a forward-looking price-to-earnings ratio is 29x. This is compared to a five-year price-to-earnings ratio of 24x — which is mathematically impacted by a lower P/E in 2019 and 2020, versus the last three years.

Apple's profit to earnings ratio for the last five years

Furthermore, a difficult comparison from the previous year continues. Kumar expects constant currency headwinds to continue, and interest rates are predicted to remain elevated.

While positive for companies like Micron, supply cuts and inventories of DRAM and NAND will impact Apple's pricing as well. It's unclear if Apple has locked in previous memory pricing as it has in the past when it predicted a cost increase, though.

Overall, Piper Sandler sees Compute-focused stocks like Nvidia and AMD to come out ahead in the foreseeable future. The firm believes that 2024 handset growth in the back half of 2024 is already baked into suppliers' stocks.

Piper Sandler's AAPL price target sits at $205, a $20-plus premium over Thursday's pre-market price of about $182.80.