Battle of the billion dollar buybacks: Apple, Inc. vs Microsoft Corporation

Daniel Eran Dilger

Daniel Eran Dilger

Over the past fifteen years, both Apple and Microsoft have invested in Apple, while Microsoft has also invested in itself. Here's a look at how those investments worked out, with particular attention to stock buybacks, a panacea certain billionaire investors are prescribing for Apple.

Apple invests in AAPL

A decade ago, Steve Ballmer's Microsoft's demonstrated no faith in Steve Jobs' ability to turn Apple around, effectively walking away from an $11.5 billion opportunity.

However, in 1999, just as Microsoft was getting ready to bail out of its purported "bailout," Apple's board of directors authorized its executives to perform up to a $500 million stock buyback. Apple's shares were around a split-adjusted $10 per share, but shot up to $34 per share at the height of the 2000 dotcom boom before crashing back down to around $10, territory where it remained for the next three years (below).

Apple's dotcom boom. Source: Google Finance

By 2003, Microsoft had sold its remaining AAPL shares while Apple had acquired 6.55 million of them for $217 million under its stock repurchase plan, or about $16.50 each relative to today's share price. At the end of that year, it looked like Microsoft had been smart to get out when it did, while Apple's buyback appeared ill-timed.

Following Apple's 2005 stock split and rapid growth since, the current value of those shares today would be about $6.6 billion, representing a 3000 percent return on investment, even though today's shares are down from their 2012 peak by nearly 29 percent.

Under its then chief financial officer Fred D. Anderson, Apple essentially reinvested a fifth of its $1.1 billion ARM Holdings windfall from the 1990s into itself, leveraging, on behalf of its shareholders, one of the highest returns on investment possible in the 2000s.

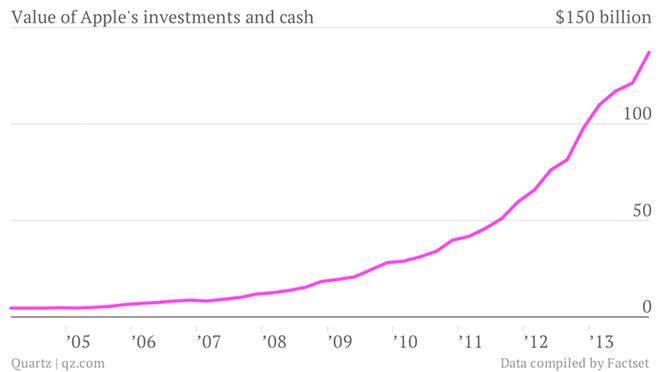

Apple grows a cash pile as Steve Jobs defends "thinking big"

In 2010, some Apple shareholders were upset to hear Steve Jobs rebuff their desire to have the company distribute its $40 billion in cash via either a stock buyback or dividend plan.

Jobs explained Apple was holding the cash for future growth opportunities, and said that buybacks or dividends were unlikely to have any significant affect on Apple's stock price, an idea many shareholders and analysts scoffed at. "When you take risks, it's like jumping in the air. When they don't work out, it's nice to know the ground is always there" - Steve Jobs

Distributing Apple's cash, Jobs said, would leave it without the capital it needed to do "big" things, and after the cash was gone, he pointed out, there would be no big pile of assets to resist the market's efforts to devalue Apple into oblivion.

"When you take risks, it's like jumping in the air. When they don't work out, it's nice to know the ground is always there," Jobs told Apple's shareholders. Cash was Jobs' bulwark against outsiders seeking to destroy the company's stock price in order to buy up the company for salvage.

Interestingly, a report by Reuters noted at the time that "Jobs offered few details on the iPad" that had been newly announced but had not yet gone on sale, adding that the "tablet computer is trying to bridge the gap between smartphones and laptops, but consumer demand for a 'third category' of devices remains unclear."

As it turned out, iPad quite clearly helped contribute to Apple's bottom line. Over the past three years, Apple's cash holdings grew from $40 to over $140 billion, leading its chief executive Tim Cook ready to admit that Apple now had more cash than it needed to operate, even if it continued to think big.

Apple again invests in AAPL

In March 2012, Cook stated "we have used some of our cash to make great investments in our business through increased research and development, acquisitions, new retail store openings, strategic prepayments and capital expenditures in our supply chain, and building out our infrastructure.

“Even with these investments," he added, "we can maintain a war chest for strategic opportunities and have plenty of cash to run our business. So we are going to initiate a dividend and share repurchase program.â€

Apple's chief financial officer Peter Oppenheimer outlined a three year plan to use $45 billion of Apple's domestic cash to pay dividends and initiate a $10 billion share repurchase starting in 2013.

Source: Google Finance

At that point in March (the starting point above), Apple's shares were valued at $585. Prior to the start of 2013, Apple's stock subsequently hit $700 in September but then crashed. Apple took advantage of the panic by buying up 4.1 million shares for $1.95 billion, at an average share price of $478.20 during the first calendar quarter of 2013.

Apple invests even more in AAPL

The company then increased its upper limit of its buyback program by $50 billion in April 2013.

Taking advantage of the long, sustained plunge in Apple's share price that effectively wiped out all the appreciation that had occured in 2012, the company indirectly used its credit-polishing cash pile to buy back another $16 billion worth of stock during the second calendar quarter, at an average price of $444 per share.

That's 27 times what the company's stock cost a just decade ago when it bought back shares at around $16.50. However, unlike Microsoft, Apple didn't have an extra $16 billion to spend back then.

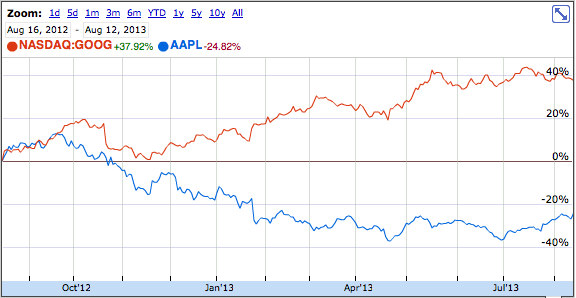

If Apple's stock were to, say, recover to levels comparable to Google's (both companies were effectively tied last year, but Apple has been punished with a 25 percent drop in share price as it reported net earnings of $30.25 billion and paid out $10 billion in dividends, while Google's stock has appreciated by nearly 38 percent after reporting total net earnings of $9.46 billion and paying no dividends over the same three quarters), that would result in a doubling of the value of Apple's $18 billion self-investment over just the last two quarters.

Note that AppleInsider does not provide any recommendations or advice related to stock transactions in the extremely volatile and often irrationally unpredictable market.

Source: Google Finance

Additionally, Apple didn't buy back those shares with its cash. It floated a bond, borrowing against its credit to fund the buyback at interest rates very close to zero. Just after it sold those bonds, the debt market sank. This suggests that Apple may have a time machine at the disposal of its Executive Committee.

Not only was Apple's $1.1 billion ARM windfall from the 1990s dwarfed by the performance of the $6 billion payoff of its stock buyback in the 2000s, but both will very likely be greatly overshadowed by what appears to be a rather easy route to an $18 billion return on its current stock buyback programs of the 2010s.

Apple's successful stock buybacks leveraged the company's artificially low valuation by the market. There was no real change in the company's fundamentals, in the outside competitive landscape or in Apple's ability to deliver innovative products.

However, Apple's $18 billion in stock buybacks and over $10 billion in dividends in the year and a half since they were first announced haven't been able to boost the company's stock price (below), despite being accompanied by industry leading profits and expanding sales.

Source: Google Finance

So while it appears to be a safe bet that Apple's remaining $40 billion budget for buybacks could be well spent eating up shares that remain nearly 30 percent below their peak from one year ago, there's no compelling evidence that Apple desperately needs to dramatically expand its buyback program, and particularly not if the goal is to raise the stock price, because so far they haven't been doing that very effectively.

Microsoft invests in MSFT

Stock buybacks' failure to lift a stock's price isn't limited to observable data on Apple, because the company wasn't the only one buying back its shares over the last decade.

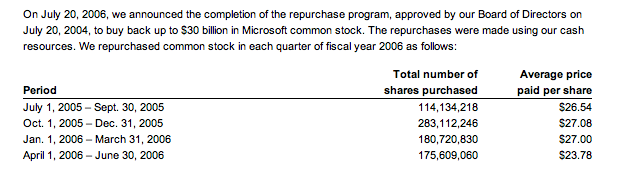

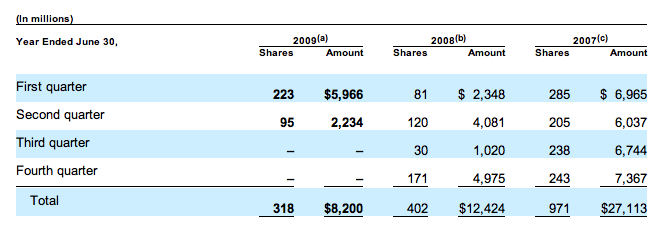

In July 2004 Microsoft announced plans to buy back up to $30 billion of its shares using cash. Over the next year, it spent $8 billion buying 312 million shares at about $25.64 per share. In fiscal 2006 it more than doubled its share buying speed, spending $20 billion on 753 million shares, at around $25.50 per share.

Source: Microsoft Annual Report

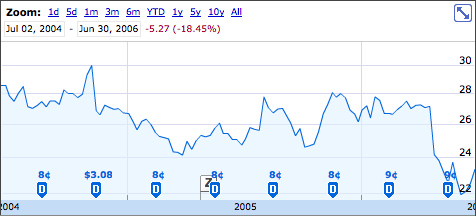

Despite two years of nearly $30 billion in share buybacks, MSFT shares actually dropped 18.45 percent, a bit worse than Apple's did over the past year of spending $18 billion on buybacks.

Source: Google Finance

Microsoft invests more in MSFT

In the first quarter of its fiscal 2007 (which started in July 2006), Microsoft announced plans to buy back $20 billion more (and then raised the authorized figure to $36 billion in new buybacks), while also floating a tender offer for up to $20 billion in stock.

Throughout fiscal 2007, the company bought 971 million shares at an average of $27.90 each, spending $27.1 billion.

The next year it bought 402 million shares at an average of $30.90 each, spending $12.4 billion. In fiscal 2009 it bought 318 million more shares at an average of $30.90 each, spending $8.2 billion.

Source: Microsoft Annual Report

In total, after five years of at least $77.7 billion in share buybacks, MSFT shares had actually dropped 18.27 percent.

Source: Google Finance

Microsoft invests even more in MSFT

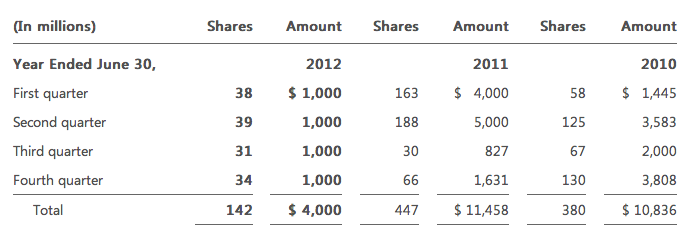

In September 2008, Microsoft announced plans to allocate another $40 billion for a third wave of buybacks in the decade, through September 2013.

In fiscal 2010, the company bought 380 million shares at an average price of $26.86, spending $10.8 billion. The next year it bought 447 million shares at an average of $25.63 each, spending $11.5 billion. In fiscal 2012 it bought 142 million shares at an average of $28.17 each, spending $4 billion. That's a three year total of about $26.3 billion.

Source: Microsoft Annual Report

In total, after eight years and significantly more than $100 billion in share buybacks, MSFT shares went up 7.46 percent. Microsoft's shares should have appreciated more than that without buybacks.

Source: Google Finance

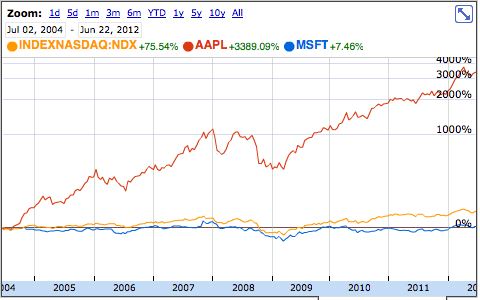

Microsoft's performance over that period of $100 billion in buybacks is noticeably lower than the NASDAQ composite and absolutely crushed by an innovating company like Apple, which over that period of time invested just $216 million in buying back its stock, less than 2 percent of the cash Microsoft had shoveled into its own shares.

Source: Google Finance

This indicates that buybacks themselves don't necessarily have a significant, positive impact on share price, even when huge dollar amounts are involved over a long term. They principally appear to have value when there's an opportunity to take advantage of irrationally low stock prices.

Andrew Orr

Andrew Orr

Amber Neely

Amber Neely

William Gallagher

William Gallagher

Malcolm Owen

Malcolm Owen

Mike Wuerthele

Mike Wuerthele

28 Comments

Personally, I don't think that paying dividends was a good idea. Buyback ok, but dividends... The Wall Street's guys seem to be particularly greedy about them, and we all know they are, (almost) all, bad guys. And it's not only that the stock price is lower than it was in September 2012, also the "perception" of Apple is changed. For the worse. And, it seems to me, that some pundits "justify" the low stock price since, according to them, Apple is less innovative than it was in the past. I disagree, but this perception is quite strong.

I think Microsofts choice to sell AAPL was more political than with regard to investment. I think they did the right thing both for them self and for Apple.

I'll say it.... What is APPL? Did you leave of the E or were you referring to the stock symbol AAPL?

"When you take risks, it's like jumping in the air. When they don't work out, it's nice to know the ground is always there" - said Steve Jobs over and over again.

Honestly, why does every new AI article have repeating sentences? This is a consistent problem that needs to be addressed.

[quote name="CustomTB" url="/t/159077/battle-of-the-billion-dollar-buybacks-apple-inc-vs-microsoft-corporation#post_2381302"]I'll say it.... What is APPL? Did you leave of the E or were you referring to the stock symbol AAPL?[/quote] APPELL PETE CORP (APPL) - going cheap in OTC for $0.00