At the time, Apple's Chief Financial Officer Peter Oppenheimer explained that the reason for subscription accounting was that the company had big plans to aggressively deliver a series of rapid software updates for the upcoming new iPhone. However, rather than planning to make money on these updates, the company wanted to deliver them to users for free to help ensure that users would actually install and use the latest updates rather than balk at upgrade fees.

It had already been proven that smartphone users were not quick to upgrade their software. In fact, few mobile software vendors had ever delivered regular new software updates to subscribers before. Instead, most vendors simply reserved new updates for the latest phones. RIM's BlackBerry OS, the Palm OS, and Nokia's Symbian OS occasionally delivered upgrades for users, but in many cases end users only got the latest update when buying a new phone with that software installed.

Microsoft had somewhat uniquely attempted to set up its Windows Mobile platform to deliver regular new upgrade releases that users could pay for because unlike Nokia, Palm, and RIM, Microsoft didn't directly make any money on hardware sales. But this plan didn't work out as expected. Few users opted to buy upgrades, and in many cases every new major release of Windows Mobile advanced its requirements to the point where it couldn't really run on any existing phones anyway.

Having surveyed the historical smartphone software landscape, Apple plotted out a series of major OS updates it planned to deliver for the iPhone along with minor update releases that would be issued in between. This strategy was patterned after the company's Mac OS X releases, although by 2007, Apple's desktop operating system had matured to the point where its annual pace of new reference releases was being relaxed to about every year and a half (at the request of third party developers who were breathless from trying to keep up with the rapid-fire updates Apple had been releasing, below).

While Apple had long charged $129 for its major new reference releases of Mac OS X, it did not expect to be able to charge anything significant for its iPhone OS updates, in keeping with what it had observed with other mobile platforms. Instead, the company determined that it would be better to offer free software updates, which would help ensure that the iPhone's user base would upgrade to the latest release as quickly as possible.

Enron and the Sarbanes-Oxley Act of 2002

Apple's plan to sell the iPhone and then deliver free updates for it throughout its two year lifespan brought the company under relatively new American accounting rules that had been signed into law five years earlier: the Sarbanes-Oxley Act of 2002. This law had been put into place in response to high-profile corporate fraud involving Enron, Arthur Andersen, WorldCom and Tyco, which had erupted around 2000 in tandem with (and helping to cause) the dotcom bubble burst.

One of the problems that the Sarbanes-Oxley Act attempted to address was "mark to market accounting," which Enron had adopted in the early 90s to record its natural gas profits. Instead of recording its actual costs and revenues at the time of selling its gas (as it had previously), Enron convinced the US Securities and Exchange Commission to allow it record estimated profits for long term contracts at the current value of net future cash flows. Essentially, Enron was counting chickens before they hatched.

This accounting scheme allowed Enron to meet or exceed investors' expectations by simply signing new contracts. It became so easy and addictive to report fantastic profit projections that Enron applied the scheme to other types of business as well. For example, in 2000 Enron partnered with Blockbuster Video to sign a twenty year agreement to provide on-demand TV services. While analysts were skeptical of the deal, its technical viability and consumer demand for the services, Enron estimated it would make over $110 million and immediately began booking these future estimated profits. Even after things fell apart and Blockbuster pulled out of the deal, Enron continued to book those future profits that would never materialize.

This scheme, along with a variety of other accounting tricks, was blessed by Enron's Anderson auditors, who also worked to silence any criticism of the tactics. Once the SEC began investigating, Anderson scrambled to shred all the evidence. While some of the principles involved were sent to prison over the scandal, it resulted in a disastrous impact upon Enron's investors, including former employees who had pensions held by the company. Enron alone lost $74 billion in stock valuation over four years, $45 billion of which was attributed to fraud.

Based on research into what allowed this to happened, the Sarbanes-Oxley Act was instituted to require certain minimum standards of financial accountability. Among its many rules is a provision that states that companies can't immediately book revenue for a product if the complete product has not yet been fully delivered. If a software upgrade materially changed the features of the product, the vendor would have to charge extra for that upgrade because delivering it for free could result in Enron-style accounting games where companies would sell unfinished products and simply promise to finish them in a later upgrade that might never be delivered, falsely inflating their reported revenues as Enron had.

On page 2 of 3: Apple, 802.11n, and Sarbanes-Oxley.

The first products Apple delivered that were impacted by the new rules were MacBooks with 802.11n WIFi hardware features. Apple sold the notebooks and recognized revenues at their time of sale, but it did not advertise the equipment's latent capacity to support the higher speed wireless networking because the technology was still undergoing the final stages of its draft specification.

Once the final draft for 802.11n was completed at the end of 2006, Apple released new AirPort base stations and MacBooks with faster 802.11n WiFi features and offered its existing MacBook users the ability to activate the secret feature on their own notebooks for a $5 fee (later reduced to $1.99), citing Sarbanes-Oxley regulations.

The company was assailed for charging the nominal fee as lots of accountants lined to testify that the law does not specifically require payments for such upgrades, but only forces companies to estimate the value of any post-sale upgrades and withhold the booking of that revenue, something that Apple had not done when it first sold the MacBooks with better hardware than advertised.

The iPhone and subscription accounting

In response to the heated imbroglio that erupted in the tech press over Apple's $2 fee for its optional 802.11n software driver upgrade, the company decided to account for new hardware it expected to upgrade over time on a subscription basis instead.

As Oppenheimer explained in Apple's FQ2 2007 conference call, "Since iPhone customers will likely be our best advocates for the product, we want to get them many of these new features and applications at no additional charge as they become available. Since we will be periodically providing new software features to iPhone customers free of charge, we will use subscription accounting and recognize the revenue and product cost of goods sold associated with iPhone handset sales on a straight line basis over 24 months."

This decision invoked the wrath of shareholders, who suddenly realized that the massive revenues Apple would be earning on iPhone sales would not show up immediately in the company's revenue reports. Instead, the revenues would slowly appear over time, delaying their ability to make short term profits. Had Apple instead recognized this revenue immediately, its stock would be expected to rise rapidly as iPhone revenues poured in immediately.

Apple blows a reverse revenue bubble

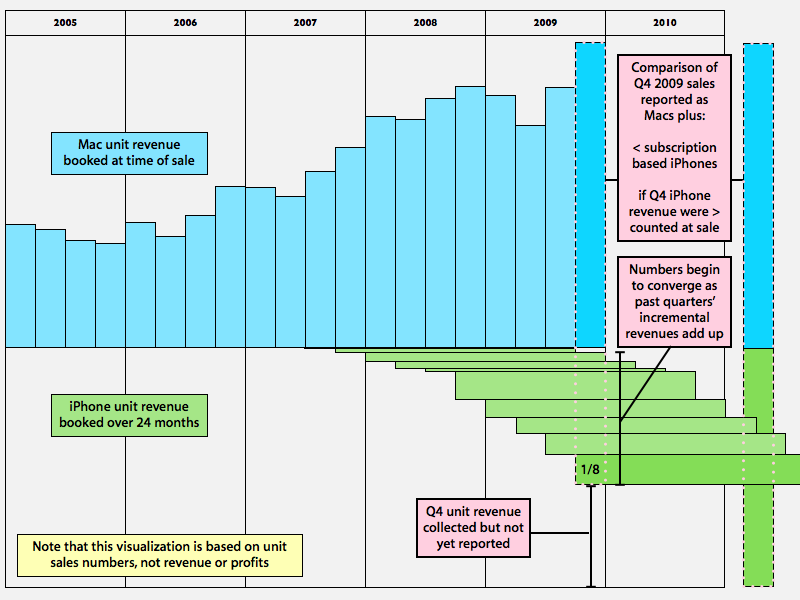

There was nothing extraordinary about Apple's subscription accounting; magazine publishers similarly accept annual subscription fees and then book monthly revenue as they deliver each issue to their readers. This results in the exact opposite of Enron's scandalous "mark to market accounting." Rather than booking lots of future revenue that may or may not appear, subscription accounting results in a company sitting on collected revenues that it does not immediately recognize (and therefore does not show up in the company's reported earnings).

While Apple announced blockbuster sales of iPhones, its reported revenues (and related metrics such as its profit to earnings ratio and earnings per share) only reflected a eighth of that quarter's revenue. This problem would eventually work itself out as Apple sold enough quarters of iPhones to begin adding up these fractional quarters' earnings together. However, because sales of the iPhone kept expanding so dramatically, the fractional installments of earlier quarters simply didn't add up fast enough.

The result was that by the end of 2007, Apple was realizing that subscription accounting was hiding vast millions in revenues from investors, the exact opposite problem of Enron. That encouraged the company to introduce the iPod touch using normal accounting, and to simply offer those users the ability to upgrade later at a nominal fee. The idea of charging $9.95 per year for an optional OS upgrade for the iPod touch again invoked the outrage of bloggers and pundits who found this outrageous.

Mr Jobs goes to Wall Street

In 2008, Apple really began paying for its decision to use subscription accounting on the iPhone. As the US dipped into recession, pundits began identifying Apple as a likely casualty of the sour economy because the company sold higher priced, premium computers and gadgets like the new iPhone and iPod touch. Additionally, they began to identify legacy iPod sales as weakening rather than simply being converted into iPhone sales, both in terms of units sold and in booked revenue.

This panic resulted in Apple's stock diving from nearly 200 to 113 in just two months ending in February 2008. Once it became clear that this fear was irrational, Apple again climbed back up to 188 in May 2008, followed by a second precipitous drop that drove the stock down into the 80s throughout the end of the year and into the first quarter of 2009.

This insanity drove Chief Executive Steve Jobs to make an uncommon appearance in the company's Q4 earnings call in October 2008 to implore investors and analysts to look at Apple's valuation based on its sales, not simply upon its officially recorded revenue under GAAP (Generally Accepted Accounting Principles) rules. The company for the first time presented non-GAAP figures that showed what Apple's revenues would look if the Sarbanes-Oxley accounting rules weren't hiding $3.78 billion of the $4.6 billion in iPhone revenue from that quarter alone.

"I would like to go back and talk about the non-GAAP financial results because I think this is a pretty big deal," Jobs explained. "In addition to reporting an outstanding quarter, today we are also introducing non-GAAP financial results which eliminate the impact of subscription accounting.

"Because by its nature subscription accounting spreads the impact of iPhone’s contribution to Apple's overall sales, gross margin, and net income over two years, it can make it more difficult for the average Apple manager or the average investor to evaluate the company’s overall performance. As long as our iPhone business was small relative to our Mac and music businesses, this didn’t really matter much. But this past quarter, as you heard, our iPhone business has grown to about $4.6 billion, or 39% of Apple's total business, clearly too big for Apple management or investors to ignore."

Jobs also outlined that in terms of revenue, the company had become the world's third largest phone maker in just 15 months, behind Nokia and Samsung, but ahead of Sony Ericsson, LG, Motorola and RIM.

On page 3 of 3: How the new rules will affect iPhone users.

Beyond the iPhone itself, Jobs also drew attention to the new App Store by saying, "We’ve never seen anything like this in our careers. There are now over 5,500 applications offered on the App Store in 62 countries around the world and the rate of new applications being submitted is increasing every week. Competitors are scrambling to copy our App Store but it’s not as easy as it looks and we are far along in creating the virtuous cycle of cool applications begetting more iPhone sales, thereby creating an even larger market which will attract even more iPhone software development."

Unstated was the fact that a significant element behind the App Store's success was that the vast majority of the 13 million iPhones sold up to that point were all running iPhone 2.0 firmware and therefore capable of accessing the iTunes App Store, because Apple was able to offer the new OS upgrade for free because of subscription accounting. Had Apple tried to charge any nominal fee for the 2.0 update, it would no doubt have resulted in complaints that would have overshadowed the App Store launch itself, in addition to preventing many users from even considering upgrading.

Subscription accounting was both helping and savaging Apple. Everyone knew it, nothing cold be done, and yet analysts kept assailing the company and its prospects as the recession deepened. The only thing the company could do is plug away at its business until the naysaying was proven wrong by a series of blockbuster quarterly earnings reports. And in time, the record breaking iPhone sales would add up to the point where even the fractions that were being reported under subscription accounting would make an undeniable impact on the company's officially stated performance.

That began to happen earlier this year, despite efforts by rival investors to portray the iPhone as dead and soon to be vanquished by the new Palm Pre. By the middle of the year, when it became apparent that the Pre was not going to damage the iPhone, and that Apple had not been idle in its own software development plans either, investors began to see the benefits of subscription accounting at least in terms of encouraging large numbers of iPhone users to upgrade to the latest 3.0 software release. The number of iPod touch users who chose to pay a fee to upgrade turned out to be much lower.

Subscription accounting gets a makeover

In the company's most recent earnings report, a full year after Jobs appeared and begged the world to give Apple a fair shake, the company reported that it had successfully worked to convince regulators to change the rules so that it could begin to recognize the majority of iPhone revenue, and yet still provide users with free updates going forward by deferring a small part of each iPhone sale's revenue.

"On September 23, the Financial Accounting Standards Board ratified EITF 09-3, which will change the way that we account for iPhone and Apple TV today," Oppenheimer announced. "Under EITF 09-3 only the estimated sales value of future upgrade rights to iPhone and Apple TV software are required to be deferred at the time of sale with the balance of the iPhone and Apple TV sales price being recognized immediately as revenue.

"The deferred amounts will be recognized over the 24-month estimated lives of the product, similar to the way we have applied subscription accounting to these product sales today. We don’t know at this time the specific amount of revenue deferral for each iPhone and Apple TV sold under EITF 09- 3, but we do believe that a substantial portion of the revenue will be recognized for these products at the time of sale.

"We are very pleased with the FASB adoption of this new rule as we believe it will enable us to more closely align our reported results with the economics of the iPhone and Apple TV sales. We will be required to adopt the new accounting rule no later than the first quarter of our fiscal 2011, a year from now, but we do have the option of adopting earlier than that some time in our fiscal 2010. We are currently assessing the impact of the new rule on our accounting and reporting system and processes. Making this change will be complex and as of now we are uncertain as to the timing of our adoption. Therefore, we don’t have anything more specific to discuss with you today about this change.

"The guidance for the December quarter that we are providing today is based on a subscription accounting treatment that we have applied to-date for the iPhone and Apple TV sales. In other words, it is based on the assumption that the full amounts of revenue and product costs for past and future iPhone and Apple TV sales continue to be recognized ratably over the estimated 24- month lives of the product."

How the new rules will affect iPhone users

While the accounting changes will not immediately affect Apple's reported earnings, it will eventually allow the company to stop being penalized for subscription accounting while still being able to offer free updates so that users continue to upgrade promptly and maintain satisfaction with their smartphone without having to pay anything extra. This also helps third-party developers confidently target the latest version of the iPhone OS without fear that there is a large population of potential users that haven't and won't upgrade.

And of course, it also simplifies the buying experience of the App Store, as users don't have to check to see if their apps are compatible with their operating system version. Instead, Apple can force developers to certify their apps against the latest version and simply delist them from the App Store if they fail to do this, as it did in the upgrade to 3.0.

This provides the company with a competitive advantage over other mobile software platforms, where many users simply can't upgrade to the latest version because of compatibility issues with their phone. For example, Microsoft only certifies its latest Windows Mobile 6.5 to work on new phones introduced this year, despite being characterized by the company as a relatively minor update.

T-Mobile/HTC's original G1 phone similarly has hardware limitations that Android developers have warned will prevent it from being upgraded to the latest software update at some point in the future, but likely before its two year life span is up. It is believed that its early adopters will not even be able to upgrade to Android 2.0.

Daniel Eran Dilger is the author of "Snow Leopard Server (Developer Reference)," a new book from Wiley available now for pre-order.