Apple Pay sparks inter-bank battle to be consumers' default choice

AppleInsider Staff

AppleInsider Staff

Major U.S. banks are set to engage in an advertising dogfight — Â designed to sway consumers' choice of their default Apple Pay card — Â as they look to take advantage of the simple one-touch mobile payment flow found on Apple's next-generation iPhones to boost profits.

"It's a healthy competition," JPMorgan Chase marketing chief Kristin Lemkau told the Financial Times. JPMorgan Chase launched Apple Pay-centered marketing campaigns on the same day as the service's unveiling, and similar campaigns from Apple's other partner banks quickly followed.

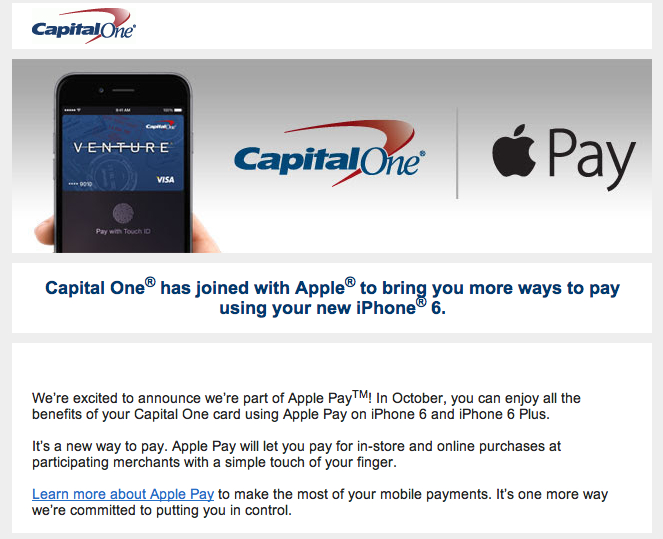

Capital One, for instance, has begun targeting customers using email blasts. With every bank having budgeted significant amounts for this purpose, advertising is likely to appear nearly everywhere — Â though Apple is said to be doling out "strict guidelines" for initiatives featuring its long-awaited payments entry.

"You want to create an incentive for people to download their card in Apple Pay and use it as their default card," Lemkau added.

To pay using Apple Pay — Â using the default card — consumers simply hold their finger on the iPhone 6 or iPhone 6 Plus's Touch ID sensor, then wave the device near an NFC reader attached to the merchant's point of sale terminal. A slightly longer process is involved to choose a different card, and banks appear to believe that users are unlikely to change cards often.

Adoption of Apple Pay is expected to be swift, given Apple's clout with retailers and the sheer size of their consumer market. Major banks — Â seeking to reduce fraud by pushing biometrically-authenticated mobile transactions — have swarmed aboard, and Apple Pay will be compatible with the lion's share of debit and credit cards issued in the U.S. once it is officially released in October.

Uptake for rival systems that predate Apple Pay, like Google Wallet, has been comparatively sluggish. Some have suggested that banks are reticent to hand over consumer data to Google, whose main business is advertising; Apple, in comparison, makes money by selling hardware and has little interest in logging customers' spending data, instead choosing to strike financial deals with banks.

Despite giving up a small portion of their revenue to Apple, banks seem convinced that reductions in fraud and, later, the possibility of increasing the volume of small transactions — the kind that are now settled mostly in cash — Â will lead to a net increase in profits with time.

Chip Loder

Chip Loder

Andrew Orr

Andrew Orr

Marko Zivkovic

Marko Zivkovic

David Schloss

David Schloss

Malcolm Owen

Malcolm Owen

William Gallagher

William Gallagher