Apple's Services business is vastly undervalued by the market, and not considered part of the larger whole by investors according to investment bank Morgan Stanley.

Recognizing an 8-percent growth in annual growth over the last five years, largely driven by iPhone sales, an investor note received by AppleInsider note suggests this will not be sustainable. Anticipated extensions to device replacement cycles, as well as a slowdown in growth of the iPhone user base, could lead to the Services business becoming the main growth center for the company.

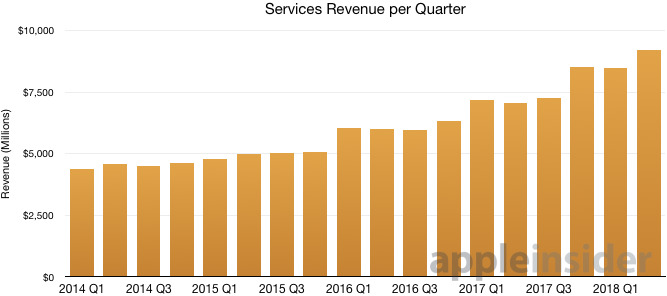

"We already see the early stages of this transition," writes Morgan Stanley analyst Katy Huberty, with normalized Services revenue growth accelerating from 18 percent year-on-year to 31 percent in the last five years. Over the same period, Huberty believes the iPhone unit growth averaged year-on-year increases of just one percent.

The growth is enough to prompt Morgan Stanley to adjust its stance on Apple's shares. Rated as "Overweight" but "Attractive" to investors, the investment bank has raised the stock target price for Apple from $200 to $214 per share.

"We acknowledge that iPhone data points remain relevant to the Apple thesis, but we believe investors instead ought to focus on understanding the drivers and growth trajectory of the Services business," states the analyst. The App Store is believed to be the "largest and most significant contributor to Services growth," with a claimed correlation between App Store performance and Services revenue.

Apple's inclination to avoid providing data points about the Services arm's activities is also identified as another sign of the App Store's importance, as the amount of detailed third-party data available for analysis is claimed to provide a "better understanding of the underlying trends" in the store. This third-party data, and the linked performance, apparently makes the App Store's fortunes a suitable barometer for Services analysis.

It is estimated users have spent over $40 billion in the App Store in the last 12 months, and by the 30-percent cut Apple takes from transactions, equates to more than $12 billion in net revenue, up 29 percent year-on-year. Games and related apps are believed to represent only 30 percent of downloads, yet make up close to 75 percent of revenue.

China, the United States, and Japan are said to make up 77 percent of App Store revenue, accounting for between 80 and 90 percent of App Store revenue growth over the last three years. While the three countries are important for future growth, all other regions are expected to grow by 40 percent year-on-year, helping the App Store revenue grow by 26 percent annually through to 2021.

While Morgan Stanley hears from investors suggestions that faster-growing and lower-margin Services businesses like Apple Music, iCloud, and Apple Pay will "drive negative mix shift" away from higher-margin and more established businesses like the App Store, the bank disagrees, as the App Store has a larger revenue base to grow from, and will continue contributing the highest proportion of incremental growth for the next few years.

It is speculated the App Store will provide 45 percent of Services operating profit growth over the next five years.

Investors are also warned to recognize "the fundamental shift in structure" for the company, due to the more accessible and considerably larger cash balance and a far larger Services business when compared to five years ago.

"By FY22, we believe Services will account for 27 percent of Apple revenue and just under 40 percent of gross profit dollars," predicts Huberty.

The opinion of Morgan Stanley follows similar declarations from Loup Ventures analyst Gene Munster, that Apple was entering a "new paradigm" where it needs to be looked at more as a service provider. Munster suggested Investors should shy away from the annual product cycle hype and "disappointment," and instead look at the Services business as a predictable growth engine for the coming years.