Apple had a pretty good quarter despite China weakness, defying analysts' doom-and-gloom predictions. Here's what some of them think on the morning after.

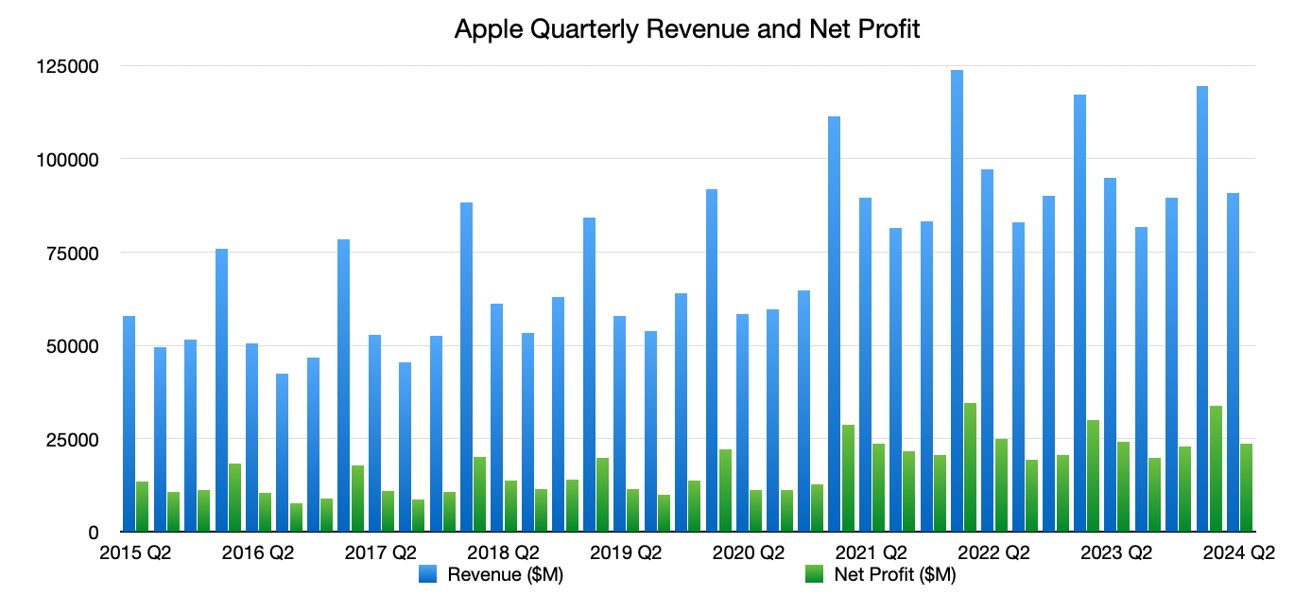

Thursday saw Apple CEO Tim Cook and CFO Luca Maestri speak to investors and analysts in the post-results conference call for Q2 2024. For the quarter, Apple's revenue was down 4% from $94.8 billion one year ago to $90.7 billion, with an increased earnings per share of $1.53.

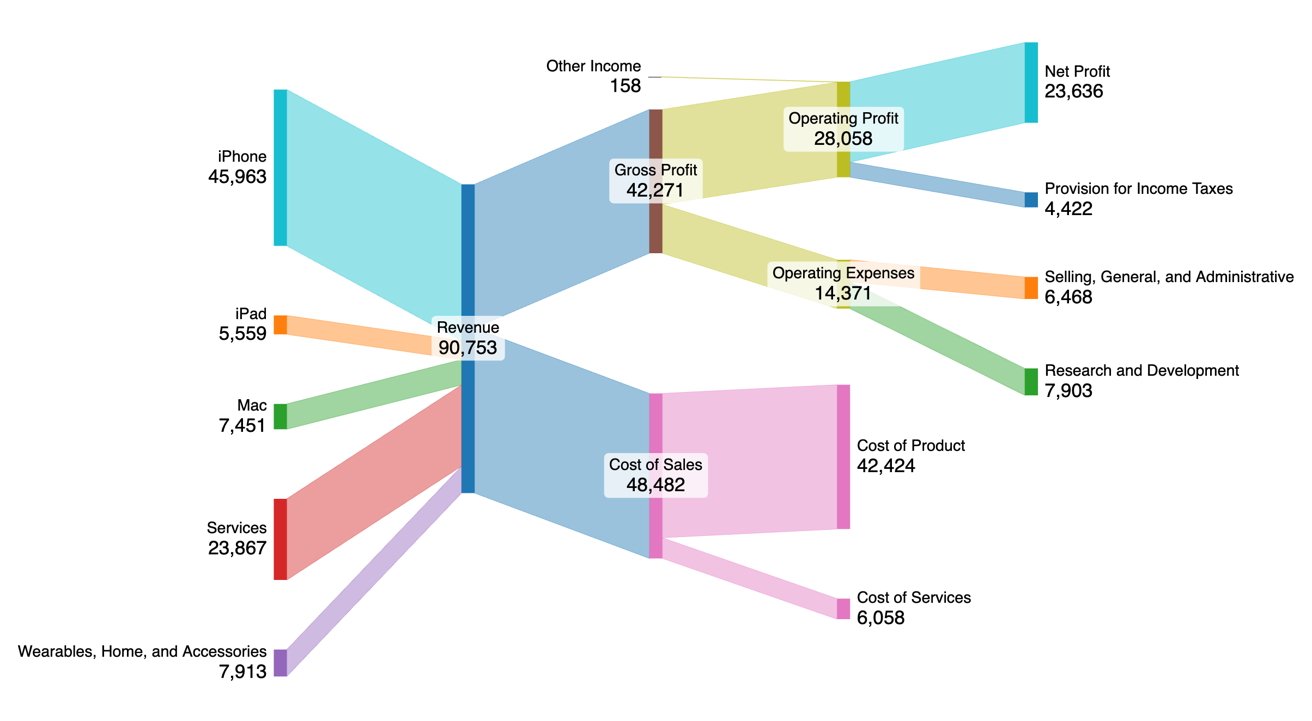

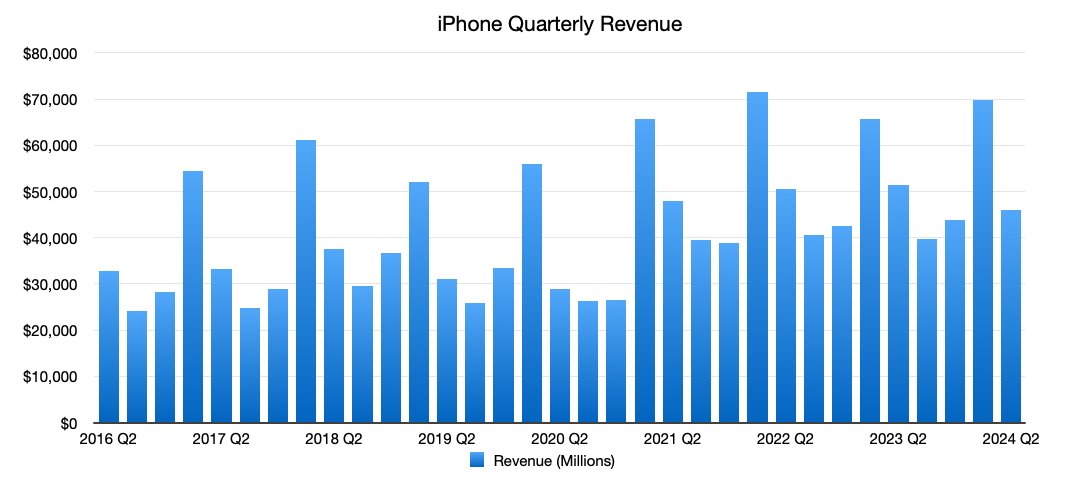

For Q2 2024, iPhone brought in $45.96 billion, down from $51.3 billion for Q2 2023. Mac saw a minor increase, going from $7.2 billion one year ago to $7.45 billion this year.

Revenue from iPad dropped from $6.7 billion to $5.56 billion. Wearables, Home, and Accessories did the same going from $8.76 billion in Q2 2023 to $7.9 billion.

Services continued to be a growing segment, beating its Q2 2023 figure of $20.9 billion by growing to $23.9 billion.

Apple Revenue and Net Profit, as of Q2 2024

Apple also announced more share buybacks, to the tune of $110 billion. This is Apple's biggest share buyback announcement, and subsequently the biggest in US history.

Cook and Maestri also had to field many questions about AI. While there were many deflections, the CEO did express that Apple already does use AI in its products.

Right after the results, the share price was given a considerable boost by investors. In just 30 minutes of aftermarket trading, Apple went from $173.03 to $185.75.

Following the results release, analysts started to offer their hot takes on the results and Apple's future.

TD Cowen

The results were in line with TD Cowen's own Wall Street consensus, "a positive given stabilizing fundamentals and despite bearish market sentiment." Continuing Services growth and cost controls helped support "near record margins."

Apple's 2024 Q2 as a Sankey chart

The iPhone revenue was also in line, adjusting for about $5 billion of "catchup demand." The expansion of financing and trade-in programs to more countries is "essential for affordability," with Latin America, India, and Indonesia potentially underpinning medium-term growth.

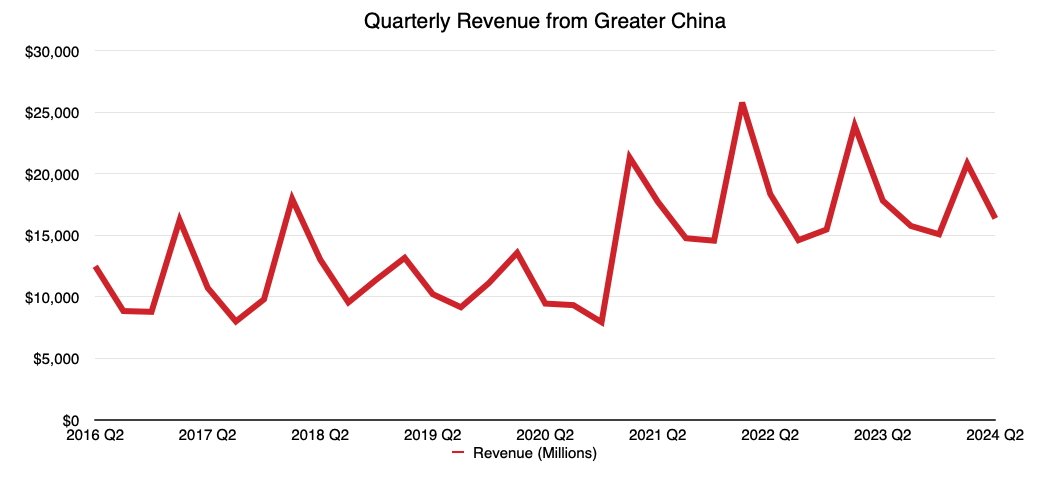

On China, the 8% year-on-year drop was mirrored by claims there was still growth in mainland China, and so there could be "better momentum" in the future.

Piper Sandler

In Piper Sandler's opinion, the results were "in line" with the highlight being "fundamental strength in the services business."

While China's a worry for investors, the analysts say the iPhone segment was down 8% sequentially in March. This is said to be an improvement on the 13% decline in December.

Apple's revenue from Greater China

The 14% year-on-year growth of Services was "exceeding expectations," with Mac also "above expectations." iPhone and iPad were "below expectations." The strong after-market performance was aided by Apple's share buyback announcement.

"Fundamentally we would like to see further improvements in iPhone trends," the firm states, before reiterating its "Neutral" share declaration.

Counterpoint

After seeing a 19% decline in March-quarter sales in China, Counterpoint offered some closure. The year's iPhone sales in the region were leaning more towards new models as well as a raised average selling point.

This combination would explain reduced unit sales while maintaining good revenue.

Apple's iPhone revenue

"Mostly it's the shift in product mix that's supporting the revenue number," the firm says. Apple's global ASP for March is believed to be $900, which is a high for the quarter.

"New models accounted for around 80% share in Q1 2024 versus only two thirds in Q1 2023, pushing ASPs higher"

Deepwater

Deepwater's Gene Munster commented that Apple's June quarter guidance was a win, since Street expectations were for flattish growth or worse. "Big picture: things get easier for Apple in the back half of the year," he mused.

The continued growth of Services was a sign that Apple wasn't really feeling the effects of the EU changes impacting its digital offerings. On the frequently discussed AI, Munster says "The speed that Apple has shifted their message on GenAI is remarkable and the right decision."

The Department of Justice probe is still a dark cloud for the company, Munster believes. However, if the probe ends up being minimal in impact, he offers that Apple's stock could trade above $200.

Wedbush

In a note from Wedbush, China was the "black cloud culprit" for the Street's anticipation of a bad quarter. "Instead Cook & Co. delivered a much better than feared Jalen Brunson-like quarter," the note starts.

The June guidance was the "star of the show" with expectations of low single-digit growth versus the Street's guess of a decline. Signs iPhone demand "turning the corner in China" and robust Services performance were cited as good indicators for the future.

Turning to AI, Wedbush anticipates a strong WWDC showing, ahead of an "AI-driven supercycle" for the iPhone 16 this fall. The analysts say Apple's strategy will involve of an AI App Store, which will be a "foundational starting point" for the coming years.

Morgan Stanley

On Friday, Morgan Stanley responded to Apple's earnings by raising its price target for Apple's stock to $216. It did so after previously dropping it on April 22 from $220 to $210.

"Apple guided to an above-Street June Q, alleviated concerns about China iPhone [sales], reached an all-time Services rev & GM record, authorized its largest incremental buyback in history, & hinted at Gen AI announcements to come in weeks," wrote analysts. "It's hard not to be more bullish after that."

Morgan Stanley dismissed the falling iPhone sales figures, saying that the decline was much less than expected. It also noted that year over year, the iPhone actually grew in mainland China, but added that more needed to be done in the country.