After monumental delays, the Coin "smart" credit card finally started shipping out to customers in April, offering users the flexibility of carrying up to eight swipeable credit, debit a rewards cards that — for now — are accepted at more locations than touchless NFC solutions like Apple Pay.

The first thing we noticed out of the box is Coin's strikingly thin profile. Coin, the company, managed to stuff an e-ink display, Bluetooth radio, functional electronics and a battery good for two years of normal use into a chassis no thicker than a traditional credit card.

As AppleInsider reported when Coin was announced in 2013, the device replaces multiple swipe-based cards by storing account information and outputting card data to point of sale terminals via a dynamically programmable magstripe. Current models don't support chip-and-pin security and lack the necessary NFC modules for contactless payments, but with near universal acceptance of swipe-to-pay POS systems, Coin's form factor is currently more flexible. That is if it works as advertised.

Setup is fairly straightforward, though we did run into some problems swiping in new cards. Pairing is completed by first registering through Coin's website, downloading and logging in through Coin's app, then authenticating and linking your unique card to an iPhone on first sync. Coin itself is personalized to each user and comes with your name etched on the back and an area for signature entry.

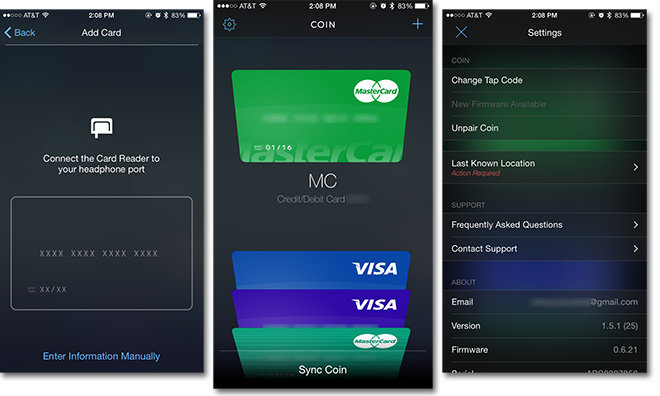

Using Coin's iOS app and the provided magstripe reader dongle, we were able to load up our most-used cards with relative ease. Coin's dongle hardware is similar to Square's product in that it uses iPhone's headphone jack as an interface. Like older Square models, Coin's reader stores its magnetic bits in one side of the housing, meaning cards must be facing a certain direction when swiped.

Some credit cards require authorization before being provisioned for use, a simple process of tapping in the CVV number located on the card's back, which is then cross-checked against data on a given provider's network. Our debit cards also needed to be authenticated by providing a correct PIN. We did have trouble with one pesky credit card that refused to cooperate with Coin's reader even after multiple swipes at different speeds. In that case, we resorted to punching in our details manually.

Tapping "Sync Coin" in the iOS app brings up a list of stored cards available for transfer (up to eight), as well as options for "Lock and Find" and changing your tap code, a unique six-tap Morse code-like sequence entered upon initial setup. "Lock and Find" is Coin's security option that uses an iPhone's Bluetooth and GPS capabilities to keep tabs of where and when Coin was last seen. The feature also uses BLE proximity features to alert users when they leave a card behind. Total card information and device settings transfer time clocked in at around ten seconds.

As long as a host iPhone is within Bluetooth range, Coin automatically unlocks when its lone button is depressed. Alternatively, the device can be unlocked using your tap code, though we found this method unreliable. A tactile click should be felt each time the button is pressed, though the mechanic was inconsistent and at times "mushy" on our unit. Luckily, a small green LED located just to the left of the button offers a secondary indication that inputs are being recognized.

Coin's green LED indicator is just barely visible.

Once unlocked, users are able to cycle through stored cards, identified by their abbreviated name (MC for Mastercard, VISA for Visa) and the last four digits and expiration date. Coin can be used at practically any magnetic card reading terminal, including ATMs. After use, the card automatically locks and powers down, monitoring for Bluetooth wake signals from a host iPhone.

We have yet to test Coin in the wild, but are anxious to do so since a majority of retailers in our small town do not accept Apple Pay. Touchless NFC payments are starting to see wider adoption thanks in large part to efforts from tech companies like Apple and Google, but swipeable cards are for now the de facto form of credit and debit payments. Here, at least, traditional cards are unquestionably the most accepted option.

In the U.S., EMV chip-and-pin systems will roll out in October, making current Coin models useless. However, POS terminals must be upgraded before that happens, so Coin has some time before becoming completely obsolete.

Those interested can preorder Coin through the company's website for $100.