Wall Street expects Apple's 'risky' iPad to sell 1M-5M in first year

Neil Hughes

Neil Hughes

Across the board Thursday, analysts were bullish in their reactions to Apple's newly announced multi-touch iPad. First-year sales predictions range from 1 million to 4 million, with potential for growth even further as the market expands and further iterations of the product improve.

Analyst Charlie Wolf with Needham & Company called the iPad "another winner," noting that the device's true potential will not be realized until developers create new software for it on the Apple App Store.

"Apple is a company willing to take risks and define new categories of products," Wolf said. "The iPad is not a revolutionary product. But it has the potential to become one once the creative juices of content providers are unleashed."

Acknowledging that reaction from the tech community has not been particularly enthusiastic, analyst Mike Abramsky with RBC Capital Markets quipped that "not everyone initially liked the Ten Commandments either — but they endured."

RBC Capital Markets

Abramsky said the $629 starting price for the 3G-enabled iPad, along with an absence of what he called "hoped-for features," may leave some investors skeptical of the iPad — but they shouldn't be.

"With iPad, Apple creates a revolutionary e-reading, browsing, media, gaming experience," Abramsky wrote to investors Thursday. "Newspapers, Web pages, books 'come alive' with video, animation, color and fullscreen touch."

He did note that the lack of Verizon compatibility, absence of a camera, and inability to multitask were disappointing. But Abramsky believes the simplicity of the iPad will be its greatest strength.

He has forecast first-year sales of 5 million, adding 30 cents earnings per share to AAPL stock with an average iPad selling price of $600.

Kaufman Bros.

Analyst Shaw Wu noted the $130 premium for the 3G-connected iPad could be a deterrent for potential buyers. He believes the Wi-Fi only version of the hardware could ultimately prove to be the best seller.

In addition to hardware price, Wu said 3G speeds are typically too slow for primary Web browsing. Plus, he said consumers will likely be reluctant to buy an additional data plan if they already have one with a smartphone.

"We see iPad as a new product category that is superior as a shared device in a group setting (such as a living room or meeting) or as an ultra-portable computer," Wu wrote. "Sure, there could be some cannibalization, but it doesn't quite replicate the functionality or for m factor of either device."

The analyst had hands-on time with the device and came away impressed. Wu did not forecast first-year sales, but noted that supply chain checks indicate Apple intends to build 5 million units in its first 12 months, and as many as 10 million units in its second year.

Needham & Company

Wolf has taken a long-view with the iPad, noting that the iPod and iPhone both got off to relatively slow starts before they experienced explosive growth. But the iPad has an advantage, he said, due to its access to more than 140,000 applications on the App Store.

Because Apple is defining a new category of devices, sales of the iPad are likely to ramp slowly," Wolf said. "But the $500 starting price point is low enough to attract a sizable portion of the early adopter crowd, consisting of iPhone and iPod owners.

"It's noteworthy that the iPad's initial price is below the iPhone's initial price and not much higher than the price of the first iPod, introduced in 2001. Our best guess at this time is the Apple could sell four million iPads in its initial year on the market, which translates into at least $2 billion of revenue."

Initial plans are for the iPad to only be sold through Apple's online and retail stores. However, Wolf said he would expect the device to see wider availability in the future.

Oppenheimer

Analyst Yair Reiner noted that although the iPad was revealed in a presentation that lasted over an hour, its true use and potential will take some time to be realized.

"It won't happen overnight," he said, "but in time, we believe that what looks today like a big iPhone or amputated netbook or a souped-up photo frame will be revealed as a revolutionary new media device."

He noted that copycat devices will inevitably crop up, but Apple's advantage lies in the iTunes ecosystem. Competitors will have a hard time replicating the 125 million active iTunes accounts with credit cards that Apple has in its camp.

Reiner has included sales of 1.1 million iPad units in the first year in his projections, a total he said is conservative. For the second year, he has forecast 4 million, while checks with suppliers indicate Apple is prepared to ship 10 million units.

Oppenheimer has increased its price target for AAPL stock to $265, from $255.

Broadpoint.AmTech

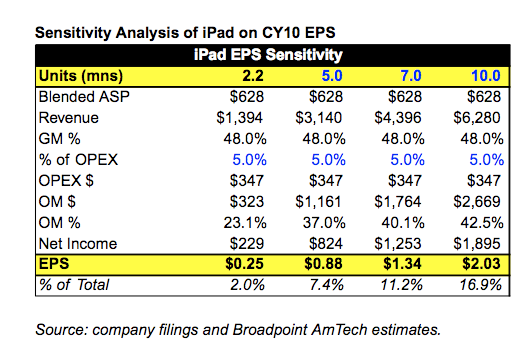

Analyst Brian Marshall said he believes Apple "surpassed expectations" with the iPad reveal. He had initially forecast 2.2 million shipments in the first year, but said he now believes "an order of magnitude higher number is likely more accurate."

Marshall did a breakdown of hardware costs for the device, and believes the $499 model would cost Apple $290.50 in to manufacture. The high-end $829 model has an estimated component cost of $383, resulting in a gross margin of 54.4 percent.

With margins that high, Marshall said Apple could add as much as $1.34, or 11.2 percent, to its earnings per share with sales of 7 million iPads at a $628 average selling price. The average gross margin of 48 percent would add $4.4 billion in revenue, or $1.3 billion in net income.

Marshall said he did not fully appreciate the iPad until he had a hands-on demo with it.

"While we were impressed with the specs during the briefing given by Mr. Jobs, it was not until we actually used the iPad for ~15 minutes we were convinced this will be another grand slam product for AAPL," he said. "The ergonomics and 'media' experience of the device (i.e. Internet browsing, e-reading and watching videos on the 9.7" screen) stood out the most to us."

Caris & Company

Buy, don't sell, on the news, is the recommendation of analyst Robert Cihra. Like all other analysts, he believes the iPad will be a success, based on Apple's ability to leverage the unique in-house core abilities ranging from hardware and software engineering to the existing iTunes ecosystem.

"We believe investors should be buying AAPL share, not 'selling the news,' with consensus numbers too low and valuation quite compelling," Cihra said.

He noted that Apple doesn't do cheap, it does different, and the $499 competitive price of the iPad will be a strength to kickstart the platform. He also has high expectations for the iBooks app and its accompanying iBookstore.

"Taking a page out of its own playbook, we see no reason why the new iPad+iBookstore can't do for print media what iPod+iTunes did for music," he said, "while we think gaming also holds potential as a long-term homerun."

Amber Neely

Amber Neely

Thomas Sibilly

Thomas Sibilly

AppleInsider Staff

AppleInsider Staff

William Gallagher

William Gallagher

Malcolm Owen

Malcolm Owen

Christine McKee

Christine McKee

242 Comments

The iPad is at the moment a niche product. The "analyst" are making predictions based off tech chatter and just the companies history.

I feel this device will evolve (obviously) but not until 2011. Apple has left the door wide open for future upgrades and much of the features that individuals want can easily be enabled through a software update

Who's to say by March/April Apple will announce more features for the device which will make it more appealing?

The iPhone was introduced in 2007 and during the initial keynote "YouTube" was not shown in the demo but during the release of the product, we had YouTube on the device.

Apple conceived the iPad for the EDUCATION MARKET, MEDICAL INDUSTRY, AND CASUAL TECHNOLOGY USERS.

I'm pretty sure we will hear more about what will be on the iPad. Though as it currently stands it's a niche product due to the lack of content. That may not be the case when it is released. Devs have 60/90 days to design for the device. CHECK OUT THE BEHIND THE SCENES VIDEO OF JOBS AND MOSSBERG FROM ALL THINGS D The video is on the right.

http://kara.allthingsd.com/20100128/...or-an-ipod-xl/

Jobs said that publishers have held back from Amazon and their not happy with their current business model for the distribution of their content

"In addition to hardware price, Wu said 3G speeds are typically too slow for primary Web browsing. Plus, he said consumers will likely be reluctant to buy an additional data plan if they already have one with a smartphone."

That's an excellent point. Since I'll already have my iPhone along with me, does it really make sense to spend $130 + monthly charges to have slow 3G access?

I think i'll grab WiFi only version now then pick up a LTE one in 2 years.

In 60 days I think Apple will have multitasking fleshed out in the OS ready for shipping iPads. We may even see Flash 10.1.

And in the next 2 month, developers will have some time to come out with some killer apps that will demonstrate the true potential of the iPad.

In 60 days I think Apple will have multitasking fleshed out in the OS ready for shipping iPads. We may even see Flash 10.1.

.

Seriously doubt that.

And in the next 2 month, developers will have some time to come out with some killer apps that will demonstrate the true potential of the iPad

But agree with that.

We regularly mock these analysts, but for me, they seem to have got the point better than half the armchair experts on this an similar sites.

The iPad is about moving information consumption in the home away from the traditional television and general purpose computer. Our laptops etc. are like early cars. Big, complicated, and need constant fettling to keep them running sweetly. Nowadays, the car industry has matured, and the most popular cars are essentially appliances (step forward, Toyota Corolla). You're average Corolla (or Auris, or whatever they're called now) have no idea how their car works. They just know that when they get in their car, it will just work. There are niche drivers who want the latest and greatest performance (buy an Ariel Atom) -- build your own PC types -- and others who are cheapskates and buy some cheap and nasty Korean thing -- or a netbook in the computer world.

This is where I think computing appliances are now heading. We will end up with a number of appliances in the house that do a few different things, but do each of them well. The iPad is not the destination, it is the beginning of that new journey. It's not about the hardware (well, except maybe the damn camera!), it's not really just about the software either. It's about the whole user experience. How you interact directly with the device; what information and media you can consume on it; the eco-system through which this information is gathered or disseminated.

I think that as of right now the iPad does a lot of the things that I want out of a living room infomedia appliance. I think that once the devs and accessories guys get hold of it, it'll allow us to do some amazing things that we've never thought about. Remember, the iPhone didn't do that much new when first launched. It wasn't so much what it did, but the way it did it. I suspect that the iPad will be just the same.