While doubts as to whether Apple (AAPL) deserves to hold the second largest market cap in the U.S. continue to mount, one thing it is clear: Apple has closed the revenue gap on Microsoft (MSFT), and looks to assume full supremacy over the software company. And though Apple still has a ways to go to compete with Microsoft in terms of net income due to Microsoft’s stunning operating margin, many will be surprised to learn that Apple will actually post more revenue than its rival in the 2010 and 2011 fiscal years.

In fact, when Microsoft reports second quarter calendar results after the bell this afternoon, its likely that Apple will have surpassed Microsoft in revenue for the first time in the company’s recent history - and that it will continue to do so in the future. Apple reported $3.25 billion in net income ($3.51) on a whopping $15.7 billion in revenue on Tuesday, smashing analyst expectations, and reporting more or less in line with my forecast.

Microsoft, on the other hand, is expected to earn $4.1 billion in net income ($0.46 in EPS) on $15.26 billion in revenue when it releases results after the bell today. That is nearly $500 million less than what Apple reported in revenue this quarter. And while Microsoft also regularly reports upside surprises making it very possible that it could edge out Apple in revenue, the gap between consensus estimates and Microsoft’s actual results is nowhere near as wide as it is with Apple’s results.

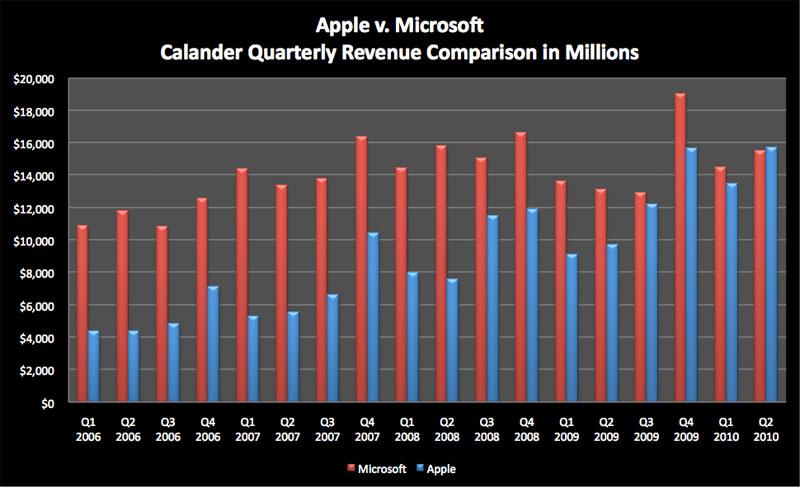

The chart below details a quarterly revenue comparison of Apple and Microsoft over the past few years. As one can see from the chart, Apple looks to surpass Microsoft’s quarterly revenue for the first time in recent history. More importantly, while Microsoft’s revenue growth appears to have slowed in recent years, Apple continues to post one record quarter after another. Since Microsoft and Apple are on a different fiscal year, the chart realigns their results to make them comparable on the calendar year.

So the big story in tech earnings this week is whether history will be made in the decades-long battle between Apple and Microsoft, or whether Microsoft will postpone the inevitable and maintain its dominance over Apple for at least one more quarter.

And even if Apple doesn’t beat Microsoft in sales this quarter, it will certainly do so next quarter and by quite a large margin. For the September quarter, analysts expect Apple to generate approximately $18 billion in revenue compared to a projected $15.16 billion expected out of Microsoft.

So even conservative analyst estimates already put Apple ahead of Microsoft by nearly $3 billion next quarter. My estimates put Apple ahead by $3.8 billion as I expect Apple to record nearly $18.9 billion in revenue.

What’s even more surprising is that Apple will likely far surpass Microsoft in revenue for the entire 2010 and 2011 fiscal year. In fact, I’m looking for Apple to record $81.6 billion in revenue in 2011 – that’s about $11.6 billion above the $70 billion I’m expecting out of Microsoft. Even the 2010 and 2011 conservative analyst consensus puts Apple well ahead of Microsoft. Thus, it’s looking increasingly likely that this quarter sets the beginning of a new age where Apple will regularly post higher revenue than Microsoft going forward.

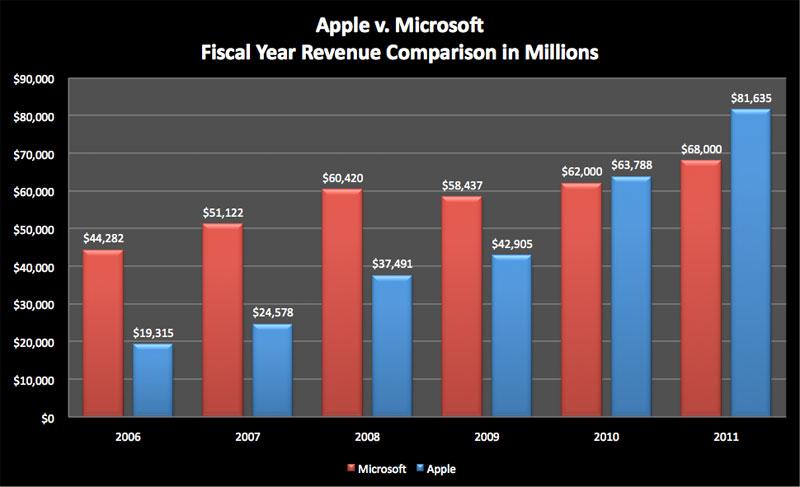

The chart below compares Apple and Microsoft’s annual fiscal revenue for the past several years. While quarterly data must be compared on the calendar year to show a side by side comparison over a particular 3-month period, yearly data can be analyzed on the fiscal year.

Yet, when it comes to questions as to which company ought to have a larger market capitalization, total revenue is but a single of several factors that should be considered. Net income growth, total net income, total net cash, cash flow, book value, total assets and the economic sensitivity of each company’s primary operations are just a few of those other key factors.

So while Apple will be surpassing Microsoft in revenue in the near future, that in and of itself doesn’t necessarily mean that Apple automatically ‘ought’ to have a larger market capitalization. Though under closer scrutiny one will find that within the next year or so, Apple will soon not only record more revenue than Microsoft, but will earn more in net income, generate a larger amount of cash, and out-pace Microsoft in terms of growth in net income and revenue.

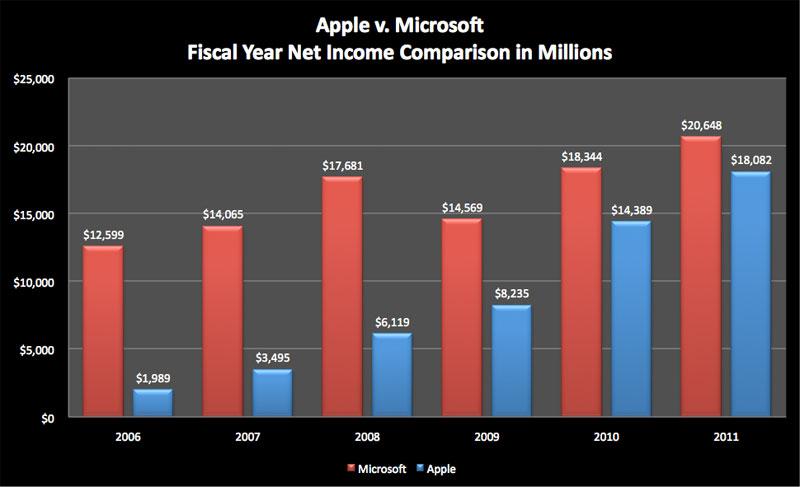

Still, Apple does have a ways to go before it will surpass Microsoft in net income. Due to Microsoft’s extraordinarily high operating margin, the only way Apple can beat Microsoft in earnings is by simply outpacing it in sales. Since Microsoft pushes more of its revenue to the bottom line, Apple will have to significantly outpace Microsoft in revenue to win on the net income front – something that Apple will probably do in 2012. The chart below compares Apple and Microsoft’s net income for the last several fiscal years, and offers projections for 2011.

Though these two companies no longer really operate in the same space as they once did in the past, Apple turning its focus on the consumer and Microsoft on enterprise spending, both companies are dominating their respective industries. Yet, several Microsoft investors have argued that it’s somehow inappropriate to compare Apple to Microsoft since Apple is a device maker and Microsoft an enterprise software maker. Nothing can be further from the truth.

Such arguments not only reek of the highest level of financial irrationality, but they are also rooted in a dangerously mislead ideology. Any two companies that make money are automatically comparable. For while the comparison may or may not be appropriate in a cross sector analysis, any two publically traded companies can in fact be compared on a fundamental return on equity basis. That much is clear. If a multi-trillionaire wanted to buy either of these companies, a fundamental comparison is not only appropriate but required for sound due diligence.

Moreover, even in a cross sector analysis where an investor wishes to determine which company is best in breed, Apple and Microsoft do in fact participate in the technology sector despite the little operational overlap between the two companies. It’s not as if Apple is a pharmaceutical company, and Microsoft an oil refiner. In fact, I’m actually shocked that I have to spell out such a rudimentary concept of finance to the average investor. If you believe that these two companies aren’t comparable, you should reconsider whether participating in the equity markets makes the most sense.

Thus, what’s left to be decided is which of these two tech giants deserves to be crowned the supreme leader of the tech sector as a whole? The answer to that question will be addressed in future articles I’ll be writing over the next few weeks. Stay tuned.