While the fourth quarter was good for Apple, analysts only care about the holiday quarter's massive revenue. A period that will be heavily influenced by the rollout of Apple Intelligence.

On Halloween night, Apple offered a treat to investors in the form of its financial results. Its fourth-quarter figures for 2024 hit a lot of good notes for the company.

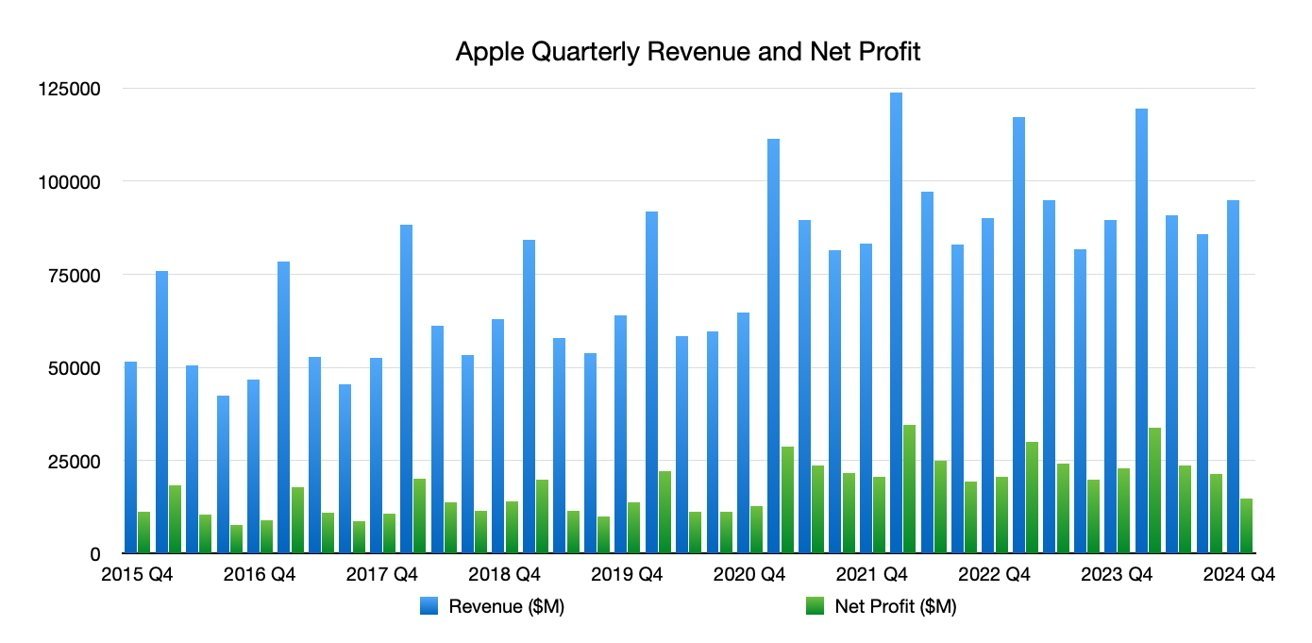

For a start, the $94.93 billion in revenue it reported for the period is a 6.1% year-on-year increase. In fact, it's higher than the $91.8 billion Apple reported in its Q1 2020 results.

Apple revenue and net profit, as of Q4 2024

This is impressive because the first quarter of the year is always Apple's highest-selling. Holiday shopping habits, along with the fall releases of new products, make Q1 a very lucrative period.

Likewise, the gross margin of $39.7 billion is up 8.5% year-on-year, as is the operating income of $29.6 billion, up 9.7%.

The net profit of $14.7 billion is a big dip of 35.8% compared to Q4 2023. However, the net profit frequently swings between an increase and a decrease over time anyway.

The main thing is that it's still a net profit, not a loss.

Product profits

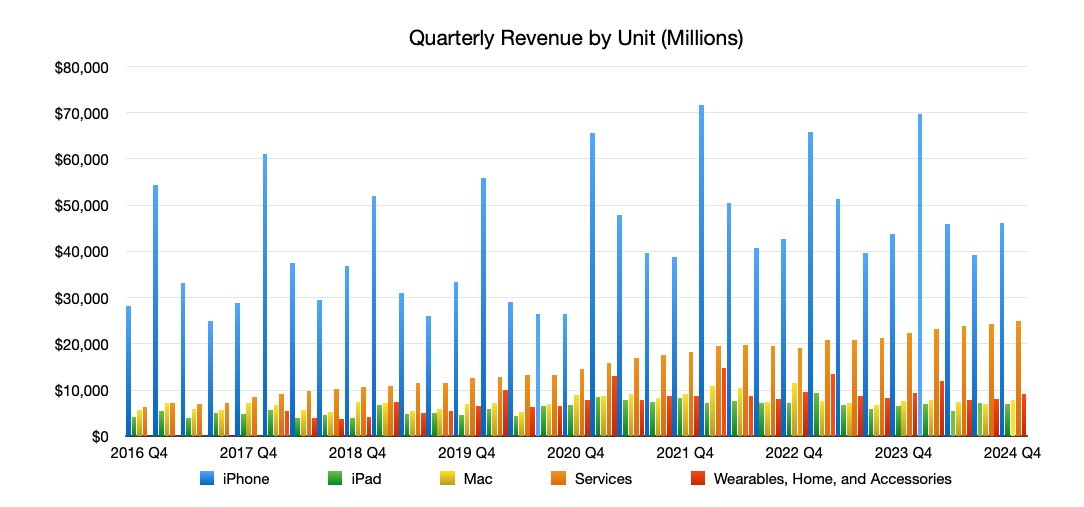

Apple's key product, the iPhone, saw an increase in sales during the quarter. At $43.8 billion, it's up 5.5% year-on-year, which is a good start for the iPhone 16 generation.

Apple revenue and net profit, as of Q4 2024

The key here is that the iPhone 16 range won't really have made much of an impact on the quarter at all. It was introduced so late that it may have had two weeks to move the needle.

This is also true for other products Apple introduced in its fall events, like the AirPods Max with USB-C and the Apple Watch Series 10. Sure, Apple enjoyed sales, but not enough to be enthusiastic about at that time.

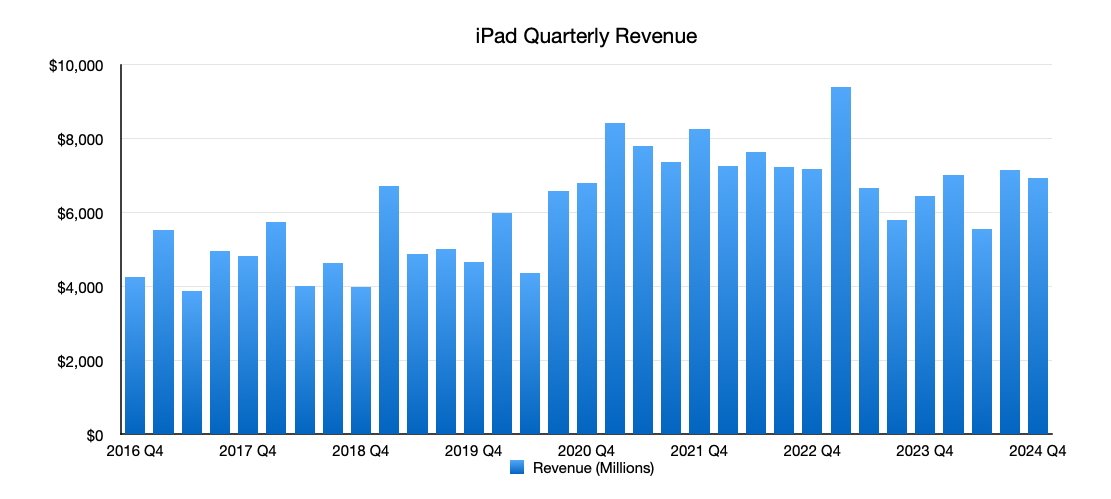

It will, however, see bigger changes from products it brought out in the third quarter. This pretty much consisted of an iPad love-in, with the M4 iPad Pro, M2 iPad Air, and the Apple Pencil Pro getting a full quarter of sales.

Apple units revenue as of Q4 2024

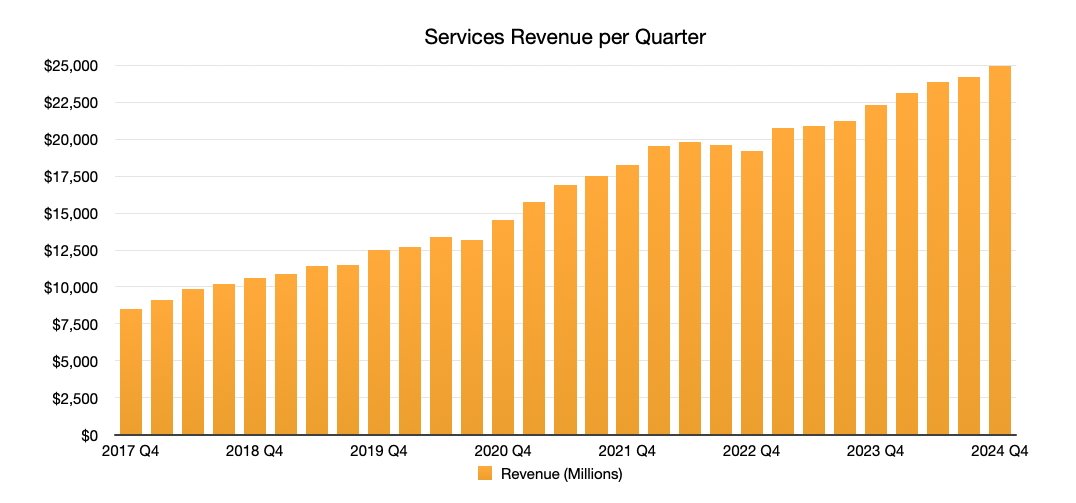

As a result, iPad sales reached $6.95 billion, up year-on-year by 7.9%. Services, Apple's consistently-growing segment, went up by 11.9% year-on-year to $24.7 billion.

Even though there were no Mac launches on Q3 nor Q4, there was still a very small rise of 1.7% to $7.74 billion.

Q1 2025 with a touch of Apple Intelligence

While Apple's Q4 product launches are important, they won't really matter until the first quarter of 2025. This is the three-month period when Apple makes the most of its money, and it times its product launches to match.

Not only will Apple benefit from the usual sales patterns at this time of year for the iPhone 16, but it should also enjoy more sales from the gradual rollout of Apple Intelligence through the period and beyond.

Apple Intelligence will also help in two other product categories which had launches in October, the start of the quarter. The iPad mini's upgrade to use Apple Intelligence adds another tablet to the range using the generative AI features, and at a more consumer-friendly price than the iPad Pro.

iPad revenue as of Q4 2024

Then there are the Mac launches from Apple's October week of announcements. The updates to the 24-inch iMac and MacBook Pro lines with M4 chips, along with the overhauled Mac mini, also offer more upgrade paths bumped up with the promise of Apple Intelligence.

As usual, Apple declined to provide actual guidance for Q1 2025 results. Commentary indicates that growth could be low for the period, to single digits year-on-year.

Even so, it will aim to beat its previous highs. For Q1 2023, it reported $119.58 billion in revenue, while its record is Q1 2022 with $123.95 billion.

Analyst opinion

Before Apple's results were released, analysts offered forecasts on what to expect from the results. After the release, the same analysts provide their reactions to the results, often justifying or glossing over their forecast versus reality.

Morgan Stanley

Morgan Stanley has mixed feelings, with the results offering something for bulls and for bears, "leaving the debate little changed." The Q1 outlook is "mixed" with lighter revenue than its buying expectations, but with a better gross margin than the consensus view.

Apple's quarterly Services revenue as of Q4 2024

For iPhone, the Q1 results could expect flat revenues. Bulls will pull for a possible supercycle in the iPhone 17, while bears will say the stock is expensive, the note to investors adds.

Morgan Stanley rates Apple as "Overweight" with a price target of $273.

Evercore ISI

In Evercore's note, Apple presented a "modest upside" to the Q4 results. The 6% revenue growth was thanks to a robust iPhone and Services performance, offsetting muted growth elsewhere.

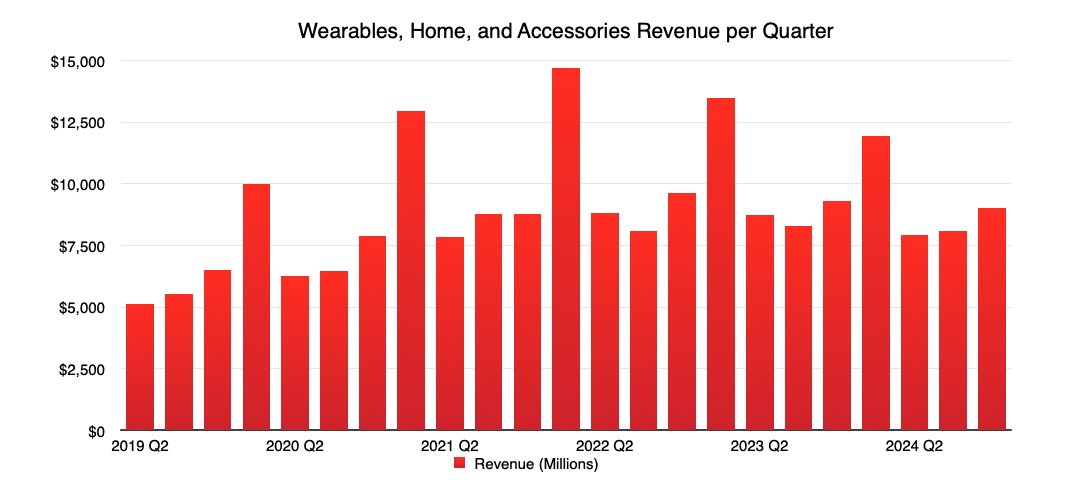

Apple's Wearables, Home, and Accessories revenue as of Q4 2024

It points to Apple's guide to single-digit growth in the Q1 2025 results and a more staggered iPhone cycle in sync with the Apple Intelligence rollout as things to consider. This could result in a "more tempered" seasonality in Q2 and Q3 2025.

Evercore maintains an "Outperform" rating for Apple, with a $250 price target.

Piper Sandler

The Piper Sandler note to investors on Friday said Apple delivered results slightly ahead of expectations, but with the December quarter set to be below consensus forecasts.

This could translate to muted iPhone growth, which is already apparently seen by Apple meeting supply-demand parity with the standard iPhone models. "Unless Apple Intelligence unexpectedly drives higher demand, we suspect iPhone unit upside over the next few quarters could remain limited," the note reads.

Apple's Wearables, Home, and Accessories revenue as of Q4 2024

Elsewhere, Mac was in line, iPad below expectations, and Services slightly missed consensus expectations.

Piper Sandler reiterates Apple as "Neutral" with a $225 price target.

TD Cowen

In its note, TD Cowen says the December quarter outlook is "sort of sufficient to appease investors who may have been fearing the worst." September quarter revenues were in line, with iPhone and flat China revenues "relative positives given the challenging macro."

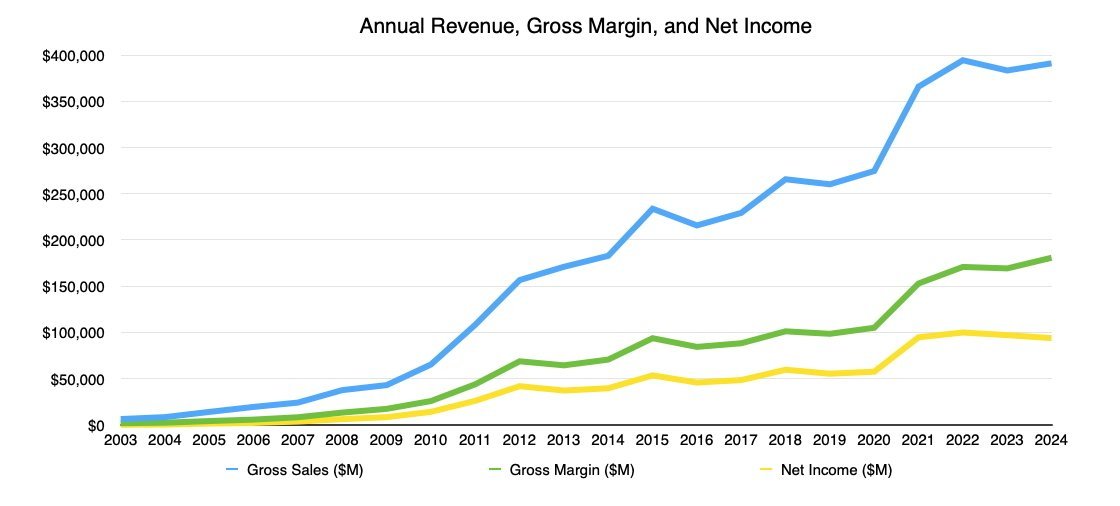

Apple's annual revenue, gross margin, and net income

iPhone was slightly above its consensus, with iPad still benefiting from the updated iPad Air and iPad Pro. Mac stands to gain from the recent launches and the potential for more generative AI features.

TD Cowen lists Apple as a "buy" with a $250 price target.