Morgan Stanley: New carriers to offset impact of longer iPhone upgrade cycles

Josh Ong

Josh Ong

Analyst Katy Huberty issued a note to investors on Friday addressing the "debate" over carrier subsidies. She identified uncertainty about the sustainability of carrier subsidies as "not a new concern."

Spain's top two carriers, Telefonica and Vodafone, recently announced that they would not subsidize devices for new subscribers. However, Huberty said she believes Spain's situation to be "unique in some ways" because Vodafone has higher acquisition and retention costs than the rest of Europe. The analyst also noted that the "macroeconomic backdrop in Spain is weak" and wireless revenue for the two carriers has been declining.

Apple CEO Tim Cook said as much late last month during a quarterly earnings conference call. He attributed "weak" performance by Apple in Spain to a "terrible economic situation" there. Cook also pointed out that carriers have kept subsidies for their existing customers.

Huberty wrote in her note that she doesn't expect U.S. carriers to drop subsidies. "We believe all three US carriers that currently sell the iPhone are required under contract with Apple to provide specific subsidy levels," she wrote. She also noted that their contracts were "unlikely to expire in the same year," so the carriers weren't set up to make a "joint push" to negotiate new terms.

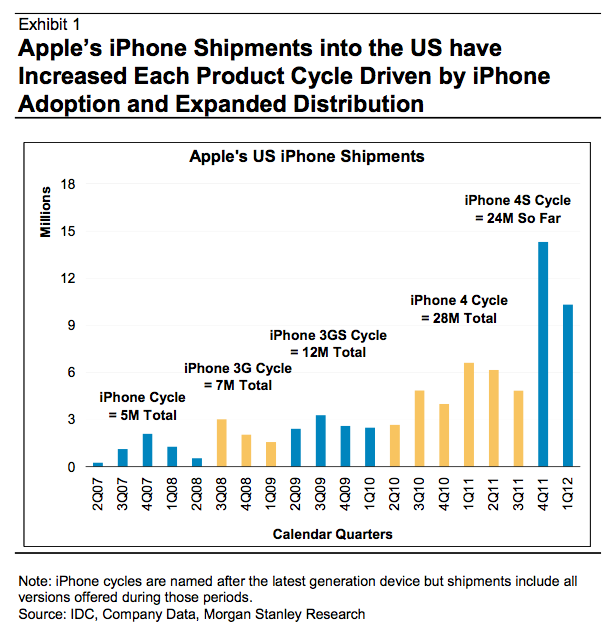

Carriers are, however, drawing out their upgrade cycle that could nominally affect iPhone sales. For instance, AT&T now requires iPhone subscribers to have finished 20 months of their contract, up from a requirement of 18 months for the iPhone 4 and iPhone 3GS cycles. According to the firm's calculations, every 3-month lengthening of the iPhone upgrade cycle would reduce U.S. shipments by 1.3 million units and global shipments by 3.5 million units during the fourth quarter of 2012.

Huberty sees iPhone growth as robust enough to overcome the longer upgrade cycle, especially since, historically, shipments of Apple's iPhone have continued to grow in spite of fluctuating upgrade terms. The analyst speculated that the addition of T-Mobile, expected to come in late 2012 or 2013, would add three to five million units annually, enough to offset any downsides from the longer cycle.

"AT&T, which has had the iPhone longer than any other carrier, recently lengthened their upgrade cycle for the iPhone from 18 months to 20 months. So far, it does not appear to have a significant impact on demand," she said.

According to Morgan Stanley's calculations, the firm's estimate of 165 million iPhone units in fiscal 2013 could even accommodate up to a 24-month upgrade cycle from AT&T and similar "long-serving iPhone carriers in predominantly post-paid markets."

The second part of Huberty's note explained why the firm's estimates are more conservative than current consensus projections. She pointed out that the June 2012 quarter is only the second quarter since 2008 where "Apple guided both revenue and earnings per share below consensus more than historical averages." The only other time was the September 2011 quarter, when Wall Street mistook Apple's warnings about the iPhone transition.

Huberty also looked to Apple's 10-Q as further evidence supporting Apple's conservative estimates.

"Historically, off-balance sheet commitments for manufacturing and components with a one-quarter lag have had a high correlation (95% r-squared) with revenue," she wrote. "Commitments of $13B disclosed in the March quarter 10-Q imply roughly $39B of revenue for the June quarter, which is only 3% higher than consensus."

The analyst concluded by noting that iPhone channel inventory suggests June quarter shipments of 25-28 million units, compared to the consensus estimate of 30 million. She said a sequential decline was consistent with reports from "Apple's key suppliers," who expect iPhone shipments to drop 15-20 percent quarter over quarter in the June quarter.

Malcolm Owen

Malcolm Owen

William Gallagher

William Gallagher

Christine McKee

Christine McKee

Michael Stroup

Michael Stroup

William Gallagher and Mike Wuerthele

William Gallagher and Mike Wuerthele

Chip Loder

Chip Loder