Mikey Campbell

Mikey Campbell

With Apple's shareholders meeting a wrap, buzz returns to the company's growing $137 billion cash hoard, which one analyst believes will play a vital role in what could be a trying two-year period for the tech giant.

In a note to investors on Wednesday, Jefferies analyst Peter Misek said the push into developing mobile markets, necessary technology development spending, and financial factors could put Apple in a tough place over the next two years.

The analyst pointed to four main concerns: capital expenditure requirements, a move into prepaid cellphone markets like India, slowing international iPhone sales, and "white box smartphones."

As for Apple's Capex requirements, Misek expects costs to double in the next two years, adding an additional $10 billion a year to the bottom line. High on the list of responsibilities is the possibility that Apple may have to finance the build-out of chip fabrication facilities as its current suppliers, specifically TSMC, are lacking the capital to expand production to nominal levels. It was reported in January that TSMC had been contracted to manufacture the A6X SoC used in the fourth-generation iPad, and is rumored to be spearheading production of next-generation A-series chips for future iOS products.

Also of concern in regard to a rise in capex spending are display manufacturing and costs related to iCloud data centers.

Apple is also forecast to make an aggressive push into burgeoning wireless markets like India and China, the former being a largely prepaid subscribership. CEO Tim Cook called the India initiative a "multi-layer distribution" model where carrier subsidies are replaced by installment plans. The company recently introduced payment plans to boost iPhone sales in the region, a move that is part of a larger "more aggressive" strategy for the developing market. The tactic appears to have gained traction as sales grew 400 percent over the last three months.

While Apple may be making inroads in India, Misek said International iPhone sales are "slowing dramatically, particularly in lower GDP per capita markets." The analyst believes alternative distribution models like those used in India could generate higher turnover, though the installments are less flexible than carrier subsidies, making it difficult to change tack if sales falter.

Finally, addressing so-called "white box smartphones," or low-cost handsets made by smaller manufacturers that are targeted at developing markets, Misek said that high-quality products are forcing Apple to invest in next-generation technology.

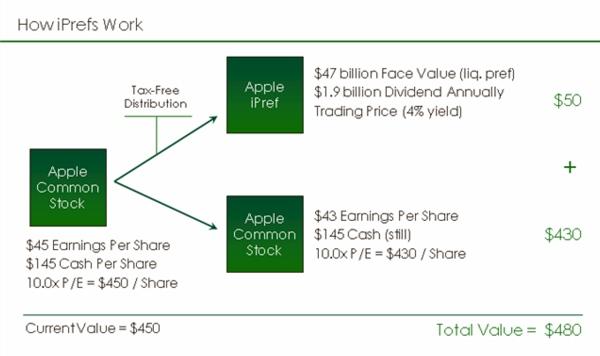

The Konka Expose, an example of a "white box" smartphone.In regard to the hot button topic of Apple's $137 billion cash hoard, the analyst noted that it could be used for traditional dividends and stock buybacks to increase "strategic flexibility" and return value to shareholders. The view contrasts that of hedge fund manager and AAPL holder David Einhorn, who floated the idea of issuing preferred shares, dubbed "iPrefs," in conjunction with common stock, to mete out some of the cash to investors.

Misek expects Apple to double its current dividend and repurchasing commitment, which stands at $45 billion over the next three years, to $90 billion over an extended period of time. Another option would be to decrease the schedule to 18 months, but in either case he sees an acceleration of traditional returns rather than the issuance of preferred stock.

The analyst has given AAPL a "Hold" rating with a price target of $500.

-m.jpg)

Charles Martin

Charles Martin

Wesley Hilliard

Wesley Hilliard

Stephen Silver

Stephen Silver

William Gallagher

William Gallagher

Marko Zivkovic

Marko Zivkovic

63 Comments

At this point Apple could sell an iPhone to every last Chinese citizen, and analysts would still shrug. Idiots.

I'm getting fed up with these a$$hats. They are totally trying to seed FUD to manipulate AAPL. Apple is making boatloads of cash, will have even more in the bank in two years, yet these clowns keep thinking that Apple's best years are behind it.

Shame the SEC doesn't clamp down on this.

I would like to opt out of all articles that contain the word "analyst". Is there a way to filter the RSS stream from this site?

I'm not trying to only hear the good news, but this isn't even news. Nobody can predict the next two years in tech.

A fairy tale. A silly one at that.

Is this moron serious? Apple just had the most profitable calendar year in human history and yet they will hit the Mariana's trench within two years?