Investment firm Needham & Company cut its price target for shares of Apple from $710 to $595 on Monday, citing growing competition in both of the company's key markets: phones and tablets.

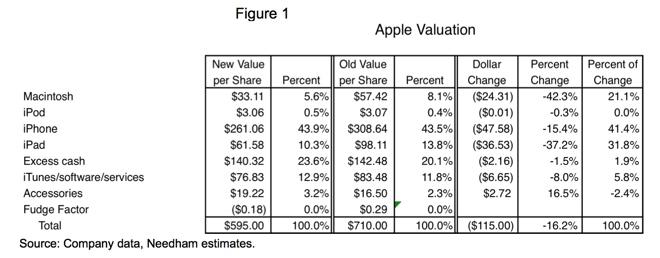

Analyst Charlie Wolf cited "increasingly hostile" competition, which led him to reduce his estimated fair value for all of Apple's major operating segments. The largest hit came in Apple's Mac business, where Wolf cut 42.3 percent of its value, citing a transition in the PC market to tablets.

The analyst also trimmed the value of Apple's iPad business by 37.2 percent, largely due to lower margins on the iPad mini. And he cut the projected value of the iPhone business by 15.4 percent, citing more competition in the global smartphone space.

Wolf has a different approach to than his colleagues, as he will only re-evaluate a company's price target twice per year. As such, his previous prediction of $710 has remained steady since February, when it was also reduced from $750.

Wolf's "Apple Valuation" model assigns a value to each of the company's businesses, with each weighted based on how important they are to the company. Those values are then added up to reach a total share price target.

In his latest model, the iPhone accounts for $261.06 of the $595 price target, or 43.9 percent. iTunes, software and services are the second most important part of Apple's valuation, in Wolf's eyes: He's given that business segment a value of $76.83 per share, representing 12.9 percent of the projected value.

The iPad is the third most valuable segment, at $61.58, or 10.3 percent of the price target. Also built in to Wolf's model is Apple's excess cash, which he pegs at $140.32 of his price target, or 23.6 percent.

A lot can and change in six months, and as a result Wolf told investors he expects to revise his projected valuation for AAPL shares once again come February 2014. He said those revisions will depend on the acceptance of new iPhones and iPads that Apple is expected to introduce this fall.