Low-cost iPhone predicted to boost both Apple's margins & international sales

Neil Hughes

Neil Hughes

Despite potentially offering a lower entry price, Apple's anticipated low-cost iPhone may actually boost the company's gross margins in the smartphone space while also increasing international market share, a new prediction suggests.

From the June quarter of 2012 until the same period in 2013, Apple's gross margins declined from 42.8 percent to 36.9 percent. Analyst Brian Marshall of ISI Group believes this was largely caused by Apple's "forced" limited production of the iPhone 4 and iPhone 4S, as the market has gravitated toward lower end devices.

But he sees a new low-cost iPhone, rumored by some to be dubbed the "iPhone 5C," potentially carrying gross margins of about 40 percent, higher than the company's current average. This implies a hardware bill of materials at around $160, and a wholesale price of about $340, thanks to parts and construction costs potentially lower than the iPhone 4S or iPhone 4.

In this way, Marshall believes the new low-cost iPhone could prove "crucial" to Apple going forward. He sees the device actually improving Apple's overall margins, and also driving market share gains in international, emerging markets where cheaper smartphones are preferred.

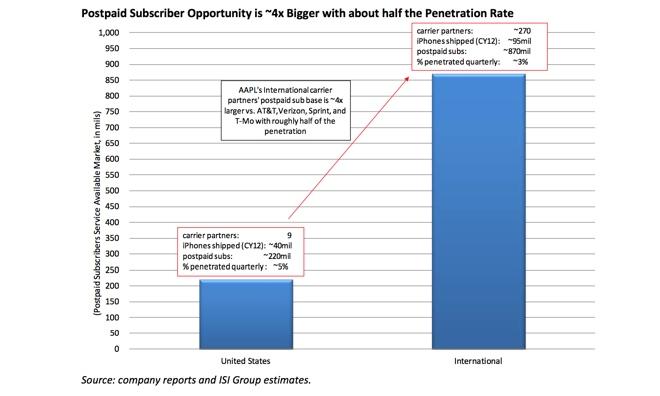

Currently, the penetration rate of the iPhone is much higher in developed regions where smartphone subsidies with two-year contracts are the norm. Marshall estimates that Apple's penetration rate was about two times greater in the U.S. versus international markets in the June quarter.

In addition, the analyst noted that Apple has "glaring holes" in its global carrier partner base, most notably China Mobile, which is the largest wireless provider in the world with about 740 million subscribers. Another key missing partner is Japan's NTT DoCoMo, which has about 62 million subscribers.

Marshall is hopeful that Apple will be able to ink deals with those major carrier in the near future, allowing the company to access a large number of new potential customers. ISI Group remains bullish on AAPL stock, reiterating its "strong buy" recommendation with a price target of $600.

Amber Neely

Amber Neely

Thomas Sibilly

Thomas Sibilly

AppleInsider Staff

AppleInsider Staff

William Gallagher

William Gallagher

Malcolm Owen

Malcolm Owen

Christine McKee

Christine McKee

19 Comments

They are certainly not making new iPhone to lower market share or margins :)

It's more effective to design a lower cost iPhone than to sell a previous full-featured product at a reduced price point as Apple has been doing with the 4 and 4S models. Their glass and stainless steel construction isn't cheap (or easy) and doesn't get much better with volume, since they were high volume products to start with. I don't expect Apple to offer a low end product as such, but a new iPhone model with plastic case and the electronics package skewed toward the cost effective end of the spectrum could offer much better margins than the 4/4S, all while opening up a previously underserved market segment.

This is the second analyst in as many days that has suggested a $350 price point for the iPhone 5c. Can you imagine if they could actually send it out the door at $300? It would wipe out half of Androids sales. Where I live the standard alternative to buying an iPhone for $200 (along with a heavy, expensive, three year contract with many limits on data and services) on one of the "big three" carriers, is buying an $300 off contract Android phone with a totally cheap, and completely unlimited month to month service. A $300 off-contract, buy it in the Apple store phone, would be absolutely huge here.

It's more effective to design a lower cost iPhone than to sell a previous full-featured product at a reduced price point as Apple has been doing with the 4 and 4S models. Their glass and stainless steel construction isn't cheap (or easy) and doesn't get much better with volume, since they were high volume products to start with.

I don't expect Apple to offer a low end product as such, but a new iPhone model with plastic case and the electronics package skewed toward the cost effective end of the spectrum could offer much better margins than the 4/4S, all while opening up a previously underserved market segment.

I agree but I kind of don't believe the "larger margins" part of this story without something to back it up. Conventional wisdom to this point has been that they can't even offer the phone below $450, now everyone seems to be switching to $350, and saying that at that price point it has even larger margins? If it has even larger margins and it's high volume product, then why not offer it at $300 or $250. The cheap iPhone is a volume product and a market share play, and their margins overall are better than the rest of the industry by far. Why worry about margins when you are flooding the world with volume?

iPhone 5C is made for Apple stores and sales channel. It is a phone which should make Apple less dependent of carriers terms and moods thus bringing more flexibility with introduction and bigger margins.

On the other hand, customers will get 0 EUR/USD/XYZ contract iPhone without making carriers nervous about profitability.

I really wouldn't want to be Samslung or anal-lyst now... :)