Having downgraded its rating on Apple stock in January, Wells Fargo on Friday defended their neutral outlook for the company's near future, characterizing it as a long-term opportunity for investors that faces near-term hurdles while the industry transitions.

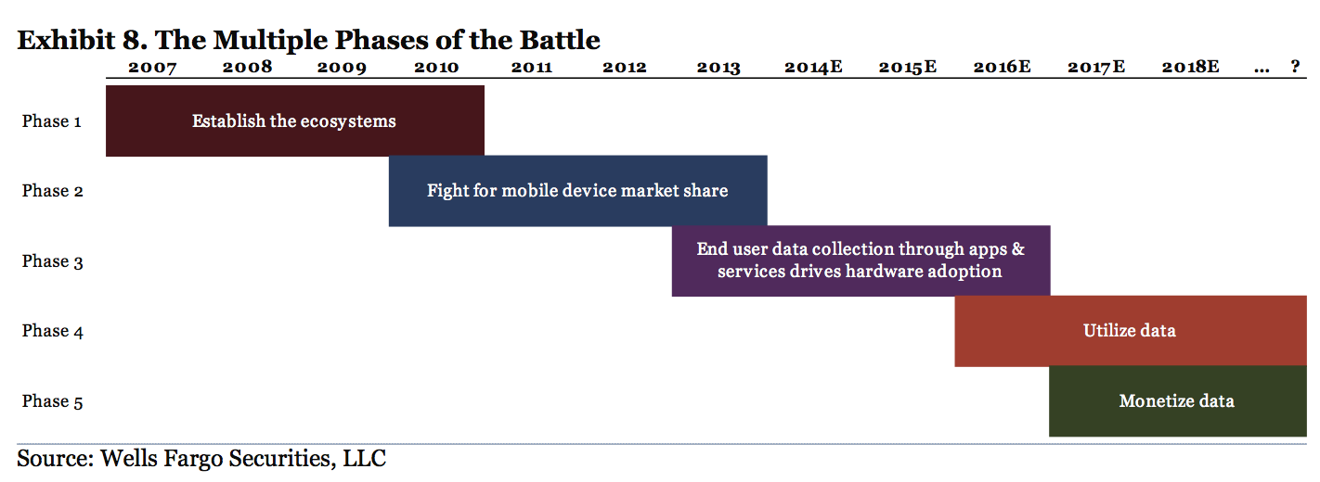

Analyst Maynard Um said in his latest note to investors, a copy of which was provided to AppleInsider that he believes Apple and its peers are in the midst of a transition phase — one where Apple may struggle in the short term. In his view, the rise of modern smartphones, which led to Apple's astounding success in recent years, has already gone through two phases: ecosystem creation (2007-2010), and a focus on establishing market share (2010-2013).

Wells Fargo sees downward pressure on Apple's margins in the near future, and has given the company's stock a "market perform" rating.

Um believes those phases are now in the past, while the industry is now in the midst of driving usage of applications, services, and the so-called "Internet of things." At the moment, companies are focusing on extending their ecosystem to include physical devices, which includes the recent interest in wearable electronics and connected devices.

This is what Um believes is "phase three" of the industry's transition, and he says it's now well underway.

In the near-term, Um believes Apple will join the trend and enter the wearable and connected device markets. He forecasts that devices like a rumored "iWatch" could allow Apple to learn more about its users in helpful ways that would further tie them into the company's ecosystem of devices.

In the current phase, platforms like Android Wear and other wearable devices are already seeking to tie users in to the ecosystem of devices by offering them new and meaningful ways of interacting with technology.

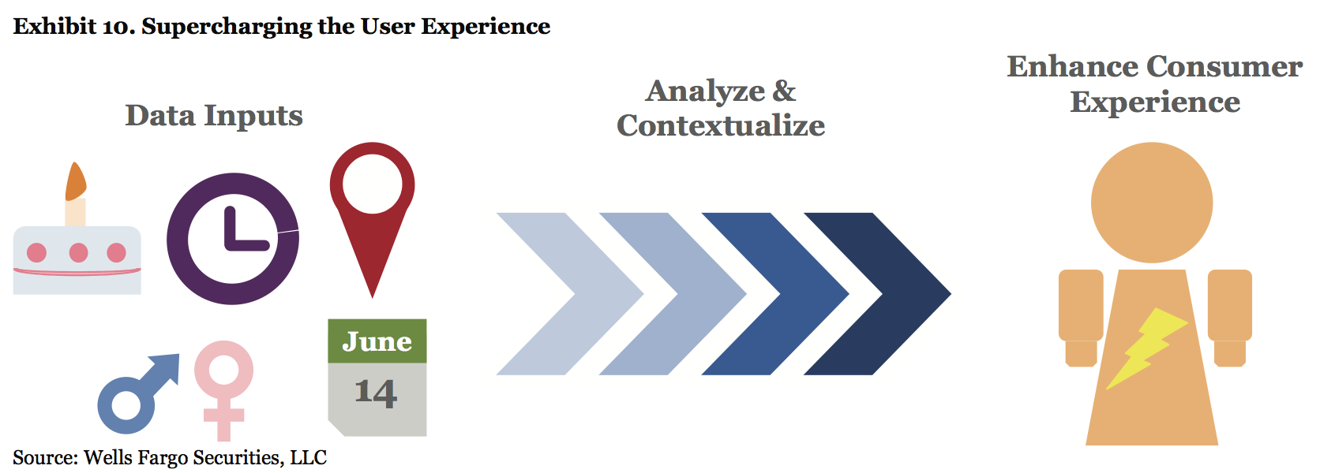

Um's anticipated "phase four" will be to enhance these ecosystems by leveraging "Big Data" collected from users. He sees these efforts being driven by machine learning, or artificial intelligence.

"By combining data points such as age, gender, location, calendar information, behavioral history, or even data mined from e-mails, like travel itineraries (and much more), Apple could effectively become a more proactive personal assistant," Um said. "Hence, the ultimate goal of this phase will be likely to offer a value-add service to not only simplify, but also become a more proactive personal assistant."

During this transition, Um doesn't believe the focus for many companies will yet be monetization. Instead, companies will be focused on making their ecosystem of services and devices more useful.

It's finally in Um's predicted "phase five" that monetization would become the focal point. However, he said companies could find other ways of profiting, and break from traditional monetization models.

One of the "radical" changes to how a company like Apple turns a profit, Um said, could be allowing users to give permission to applications and devices to access their personal data. Apple could then charge for this access and profit from other parties.

"For example, a user can allow a healthcare provider to access iWatch health and exercise data directly in-app to get lower premiums," he said. "In this model, we note that the distribution of 'ads' (or really, value) is driven by the distribution of apps. Hence, Apple's ecosystem provides a powerful distribution platform for companies that may be looking to use their own apps to drive targeted marketing opportunities."

It's in getting to this mythical "phase five" that Um sees hurdles and challenges for Apple. He said on Friday that there are certain changes that the company must implement if it wants to find success, including "improvements on user identification to authenticate data, more sophisticated and back-end data access, deeper analytics platforms, greater ad service capability combined with app creation capability, privacy, and security, to name a few."

Um said he sees "phase five" opening up more market-cap opportunity for Apple, though the interim phases will require "a lot of work" that may not be as profitable. For that reason, he has maintained is "market perform" rating bestowed upon Apple since January.

In the near-term, he's concerned about gross margins for the company's next iPhone, as margins have historically taken a hit with each of Apple's major smartphone redesigns. He also sees limited market capitalization opportunities in its current markets, as well as new areas of expansion such as television and a smart watch.

In its "market perform" rating, Wells Fargo has a projected valuation range for AAPL stock between $505 and $575. The company is currently within that range, trading at around $521 as of Friday morning.