Rivals have fallen away and while it's taken a long time to be adopted very widely in the US, it's practically ubiquitous overseas. Apple's uphill battle to bring us Apple Pay was a fight that began publicly on September 9, 2014.

Tell the average American person or American company about Apple Pay and even more a decade on, they will invariably be more wary of its security than, say, Europeans. They need more convincing that it's safe and this is a direct but unfortunate consequence of how bad the current US financial transaction system is.

According to a Security.org report, 52 million Americans were victims of credit card fraud in just 2023 alone. Unauthorized purchases exceeded $5 billion that year.

More recent and directly comparable figures are hard to determine because of differences in banking systems and reporting. However, just as one illustrative example, Spendesk claimed that in 2016, the total value of credit card fraud across Europe was around $2 billion.

The US has traditionally suffered more in credit card fraud, partly because of the sheer scale of transactions made there. But the country has also been slow to adopt safer systems, such as the EMV (Europay, MasterCard and Visa) standard from the 1990s.

Digital payment systems like Apple Pay and Google Pay should improve matters, but there is still a stigma over the security of paying with any type of card.

Apple security

Nonetheless, Apple Pay is a genuine solution. That's at least in part because, in typical Apple fashion, the company worked to deal with all the security issues behind the scenes.

And it worked to produce a system that first compelled us to try it through its ease of use.

On September 9, 2014, Apple announced Apple Pay. This was at the same keynote where the iPhone 6 and the Apple Watch were revealed. And where U2 gave away an album on iTunes.

It was a big presentation. But while the iPhone 6 is now ancient history, and U2 has apologized, Apple Pay and the Apple Watch are bigger than ever.

Tim Cook said that Apple's ambition was to completely replace the wallet — and by implication also the handbag and the purse. The company was to start by tackling payments which Cook reported then meant 200 million transactions every day in the US and a total of $12 billion per day.

Today his explanation needs some more context, because later in 2019, the company launched Apple Card. It's a credit card that uses Apple Pay, but when Cook was explaining the service in 2014, he was referring to all credit cards.

Showing an image of one, he said that these transactions are: "based on this little piece of plastic. And whether it's a credit or debit card, we're totally reliant on the exposed numbers, and the outdated and vulnerable magnetic interface — which by the way is five decades old — and the security codes which all of us know aren't so secure."

Replacing the card

Cook then compared the regular way of paying by card at a store to how it now would be with Apple Pay. He did definitely over-sell how many steps the regular system takes but he was spot on about the speed of Apple Pay. Hold your phone or your Apple Watch near the payment machine and you're done.

"It's no wonder that people have dreamed of replacing these [cards] for years," continued Cook. "But they've all failed. Why is this?"

"It's because as it turns out most people that have worked on this, have started by focusing on a business model that was centered around their self interest instead of focusing on the consumer experience," he said. "We love this kind of problem — this is exactly what Apple does best."

You know how this works

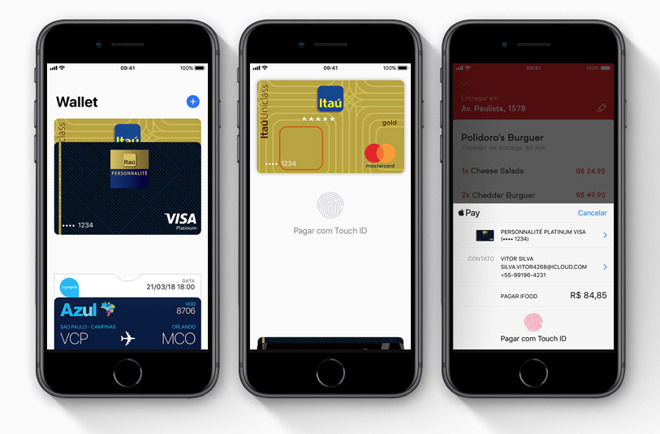

You can add your credit or debit card to Apple Pay and so have it available through your iPhone and Apple Watch. There's also the ability to use it on websites.

Though at launch that ability to pay directly on a website was the least promoted by Apple. Far more prominent in the company's press release was the fact that the service supported cards "from the three major payment networks, American Express, MasterCard and Visa" and issued by "the most popular banks including Bank of America and Wells Fargo".

There was also support right away in the US from retail stores such as Bloomingdale's, Duane Reade, Macy's and more. In total Apple Pay was to launch with the partners "representing 83 percent of credit card purchase volume in the US".

Wherever you bought anything using Apple Pay, you were paying with your credit or debit card but the vendor never sees that. You no longer give your number, expiry date, or codes, because instead Apple Pay creates a transaction code that's unique to your device and to this specific purchase.

This transaction code uses what's called the EMV Payment Tokenisation Specification. It's based on the same Europay, MasterCard, and Visa standard that has been protecting Europeans for decades.

For the transaction to work securely, there has to be confirmation that it is your device being used. And that is provided by Touch ID and Face ID.

Apple Pay works as advertised and it is as straightforward as Tim Cook claimed. That didn't mean it was welcomed by everyone or that it escaped critics, though.

Critics

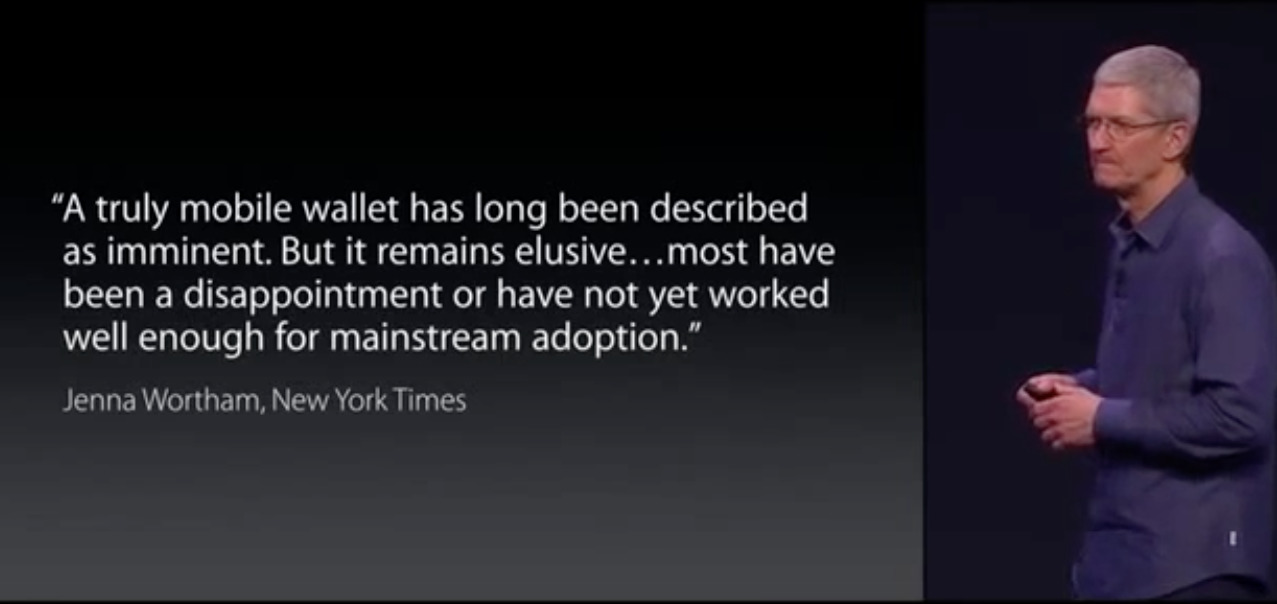

Writing for the New York Times, Neil Irwin claimed that Apple was overplaying the arduous difficulty of paying with your credit card.

"It's a dangerous business to bet against Apple's ability to make a product that you didn't think you needed as part of your daily life. But 'Apple Pay' looks as if it may be one of those offerings that don't live up to the company's hype."

Even so, Irwin acknowledged the security issues that Apple Pay improved on.

Still, Apple Pay would come in from harsher treatment from another group: the retailers involved in trying to create a different payment system.

MCX and CurrentC

Apple Pay's announcement came about two years after the creation of Merchant Customer Exchange, a company formed to create a mobile payment system called CurrentC.

It was a consortium formed by some of the best-known firms in American retail such as 7-Eleven, Best Buy and Walmart. Together they reportedly then accounted for around $1 trillion per year in sales.

Best Buy and Walmart stated that they would not accept Apple Pay at their stores. Others who were already using some contactless systems found that customers could already use Apple Pay on them without the stores doing anything. So CVS and Rite Aid did something: : they actively stopped Apple Pay working in their outlets.

It's hard to imagine any store refusing to accept a valid form of payment they were already capable to taking. But in this case, the companies arguably had no choice. Their contract with the MCX consortium forbade the use of any rival system.

That wasn't a big deal and certainly not reason to refuse to sign the contract, not back when it was launched in 2012 and there were no real alternatives.

Come 2014 when there was Apple Pay and CurrentC still wasn't expected for another year, though, this became a very big deal.

It was a big enough deal that eventually CurrentC simply died. It took years but in 2017 what remained of the consortium's technology was bought by JPMorgan Chase & Co.

Tim Cook had stated that other companies had failed because they put their self-interest ahead of any consideration about customers and he was entirely right. That's exactly what MCX did.

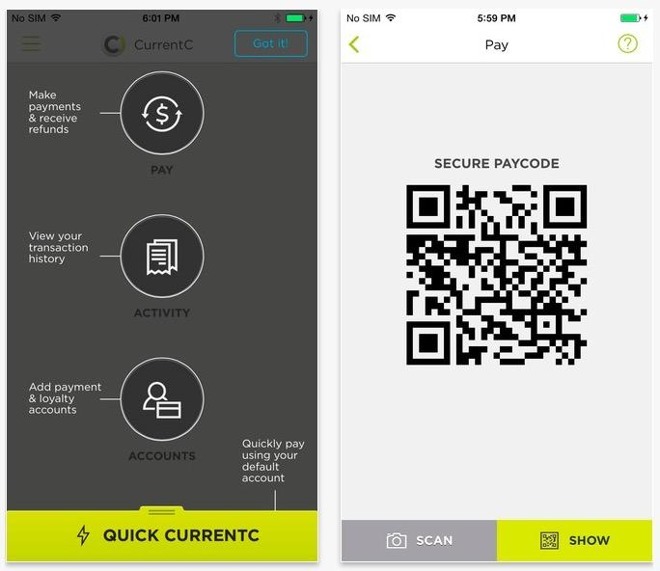

For its aim was not to create a payment system that was convenient and secure for users, but rather to get around companies having to pay credit card fees. Rather than accepting the costs involved when a customer uses a credit card, CurrentC would take money directly from their bank accounts through an ACH transfer.

There's nothing wrong with that, so long as the customer has agreed and is getting a benefit from it too. Plus in theory the customer could have got the same convenience that Apple Pay offers.

But in practice the system was a chore. You had to find the right QR code on your phone and show that to the merchant who would scan it.

You don't even have to look at the turnstile reader to use Apple Pay

If you've ever briefly held your iPhone over a card reader or wafted your Apple Watch over the turnstiles in the London Underground, you'll know how vastly better Apple Pay is.

Only, MCX had a point

It genuinely seems that Apple started with what would benefit customers but of course it wasn't altruism and naturally the company found its way to creating a gigantic benefit for itself.

Every time anyone uses Apple Pay, Apple gets some money. Obviously it does and so do credit card companies. While figures vary in different locations and while they are changed over time, the Financial Times reported in 2015 that Apple would take 0.15% of any purchase. (Article requires subscription.) By comparison, in 2025 SwipeSum reported that credit card companies take between 1.5% and 3.5%.

On the surface, that makes Apple Pay more attractive to retailers — but Apple Pay is ultimately just a way of storing your card on your phone. Depending on your card, your bank and quite how the transaction is done, you are effectively still paying by a card. Which means the retailers are can still be having to pay a fee to the card companies.

Then Apple does also have a way of presenting the best side of a feature.

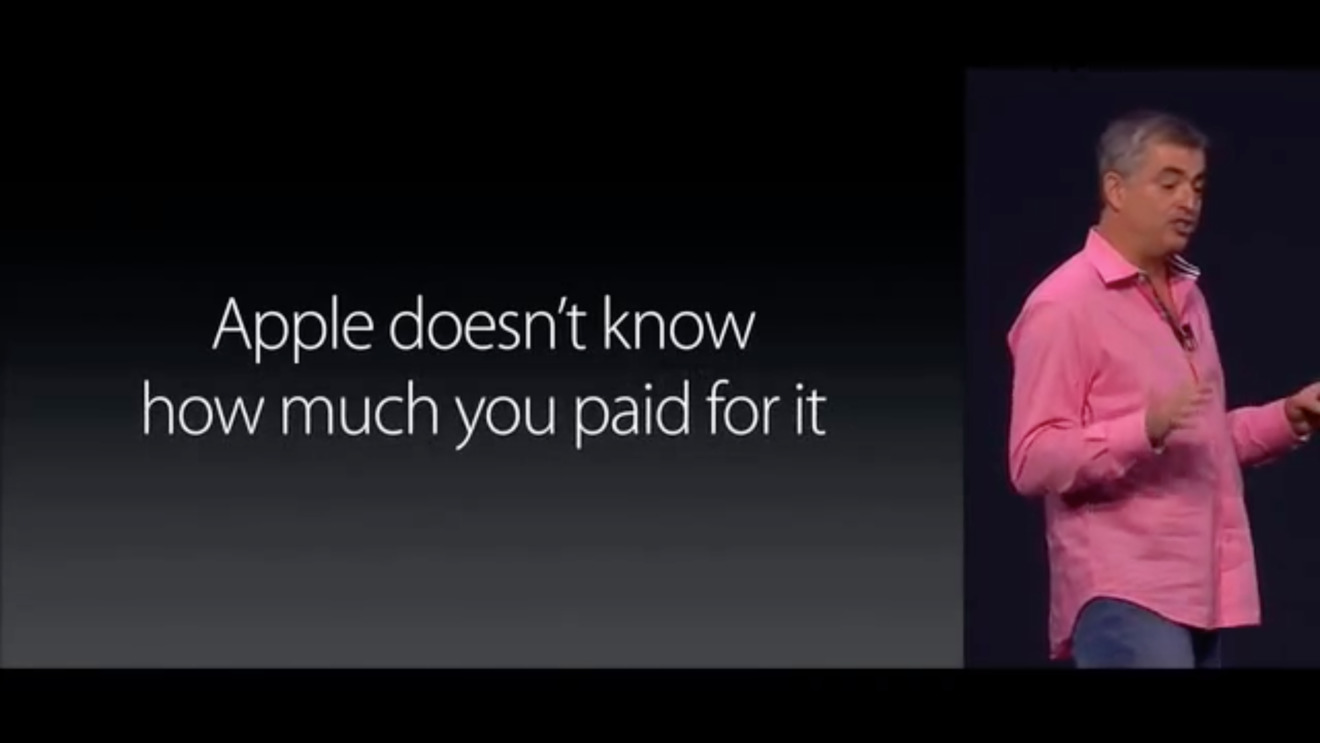

Over three slides at the launch presentation, Eddy Cue stressed how secure and private Apple Pay was. He said that Apple doesn't know what you bought, where you bought it or how much you paid.

What he didn't say is that it's at least partly because Apple also doesn't care. The company gets a transaction fee and overall it gets yet another reason for people to buy into the Apple ecosystem of software and hardware.

MCX's CurrentC was intended to handle loyalty cards and coupons, the kind of things that give stores an Apple-like way to encourage customers to stay with them. At launch, Apple Pay had none of this.

This was the retail equivalent of how developers on the App Store got no information about their customers. It has changed, though. In 2017, AppleInsider reported on how US restaurant chains were able to offer loyalty cards via Apple Pay.

So Apple Pay was steadily developing as well as expanding to more and more banks, more and more countries. That's more than can be said for Apple Card, which as of 2025 still remains a US-exclusive.

Speaking of Countries

Years after its launch, it is still news when a new bank or credit union signs up to support Apple Pay — or rather it is in the States.

Chiefly since other countries were already moving to contactless payments, it's more common that Apple Pay just works there.

You can easily add cards to Apple Pay. But not this one: the card has expired and I've changed banks, too.

In the United Kingdom, for instance, Apple Pay arrived in July 2015 and the company claimed that "over 250,000 locations will accept Apple Pay". In practice, contactless payment readers didn't see Apple Pay, they saw the cards you had stored on it and so they simply worked immediately.

Consequently Apple Pay was instantly accepted just about everywhere in the UK. We're hesitating over saying definitively that it was absolutely every possible place you could pay money but if it wasn't that universal, with was incredibly close to it.

Which means that now, some years on from the launch, Apple Pay is just another form of payment. Ten years on, you do still occasionally get comments if you use it with your Apple Watch but not often.

There have been some changes since Apple Pay came to the United Kingdom, though. Initially payments were limited to amounts under 30 Sterling (approximately $40 US) but that was because so were all contactless payments.

Now many places will accept any amount through Apple Pay. Unfortunately, there's no way to know which these places are until you try.

There are exceptions

There are places where Apple Pay is not available and they are significant. Even a decade on from its launch, Apple Pay cannot be used in India, a simply giant market, and it appears that situation won't improve any time soon.

There are many issues preventing the service working there and they are a mixture of technology and financial ones. Apple is reportedly concerned about having to store customer data within the local country — though it does this with China.

And the National Payments Corporation of India has allegedly been distrustful of fingerprint technology such as Touch ID and would prefer people enter a passcode.

There are also improvements

Back at that 2014 launch of Apple Pay, Tim Cook said that the company's aim was to replace the wallet and that it was starting with payments.

It's true that you can now — and we regularly do — leave home without carrying any cards at all.

Except that only works if you are solely going to be paying companies like retailers. When you need to pay a friend because you're splitting the bill in a restaurant, Apple Pay is no use to you.

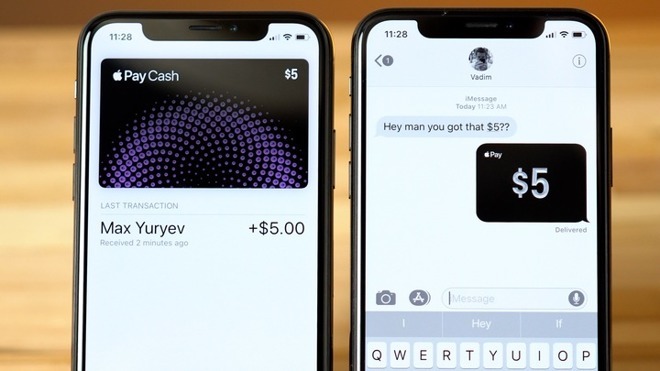

Or rather, it wasn't. From iOS 12, you could use Apple Pay Cash to effectively send money over text message.

Next, with iOS 18, Apple added Tap to Cash, to both iPhone and Apple Watch. You can split that bill, or pay a friend for anything we need, just by holding your devices together.

Apple Pay is still being developed and improved, and it is still a boon to Apple users.

But what it isn't anymore, though, is the only way to use your Apple devices to make payments like this. Due to the Digital Markets Act in the European Union, Apple has been forced to open up its iPhone NFC technology to rival payment systems.

It's still early days for this, and while rivals have said they're ready to start as Apple Wallet alternatives, it remains to be seen just how much users in the EU prefer them to Apple Pay.