Apple broke its own quarterly record for revenue in the September quarter, but it fell short of what Wall Street was predicting largely because of supply chain constraints affecting the entire industry. Here's what analysts had to say about the results.

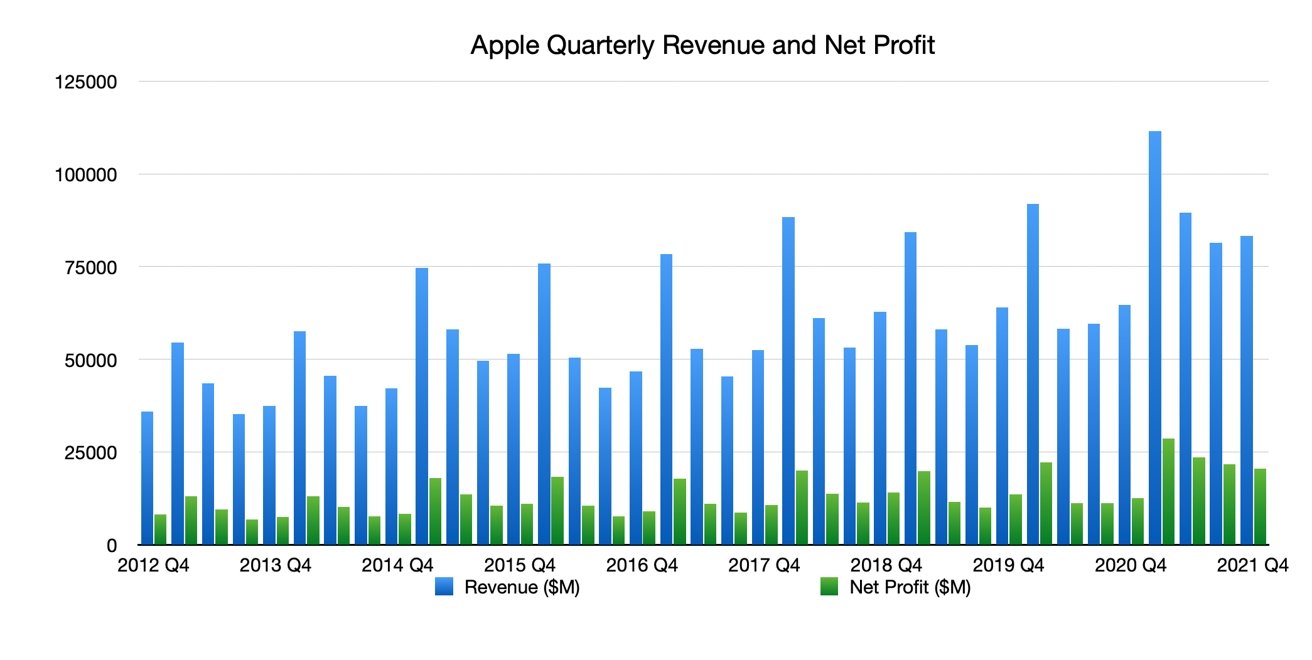

The Cupertino tech giant reported quarterly revenue of $83.4 billion, missing Wall Street expectations of $85. Apple attributed the revenue miss to chip shortage and manufacturing problems, which the company says cost it $6 billion.

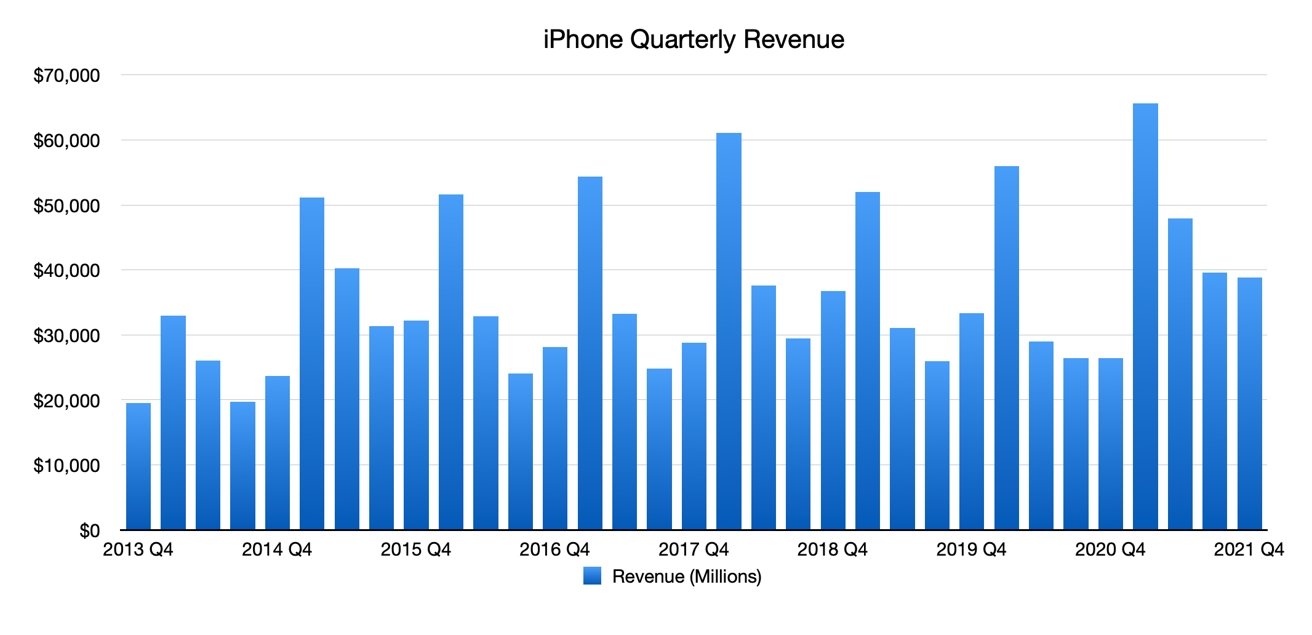

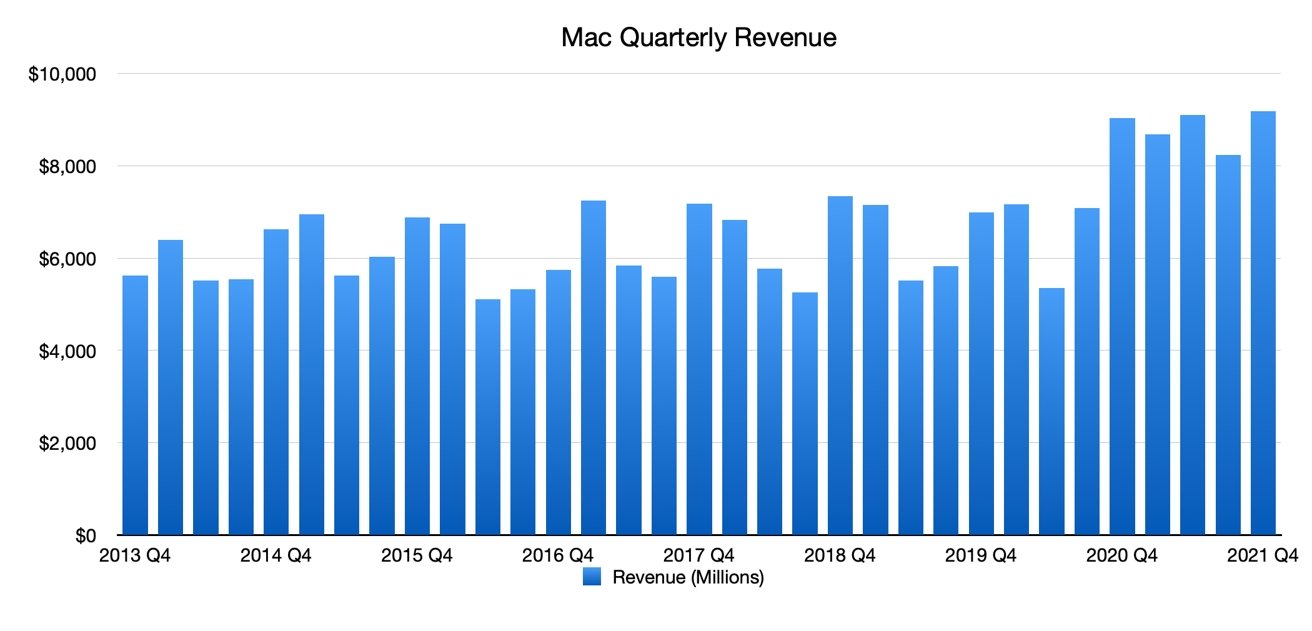

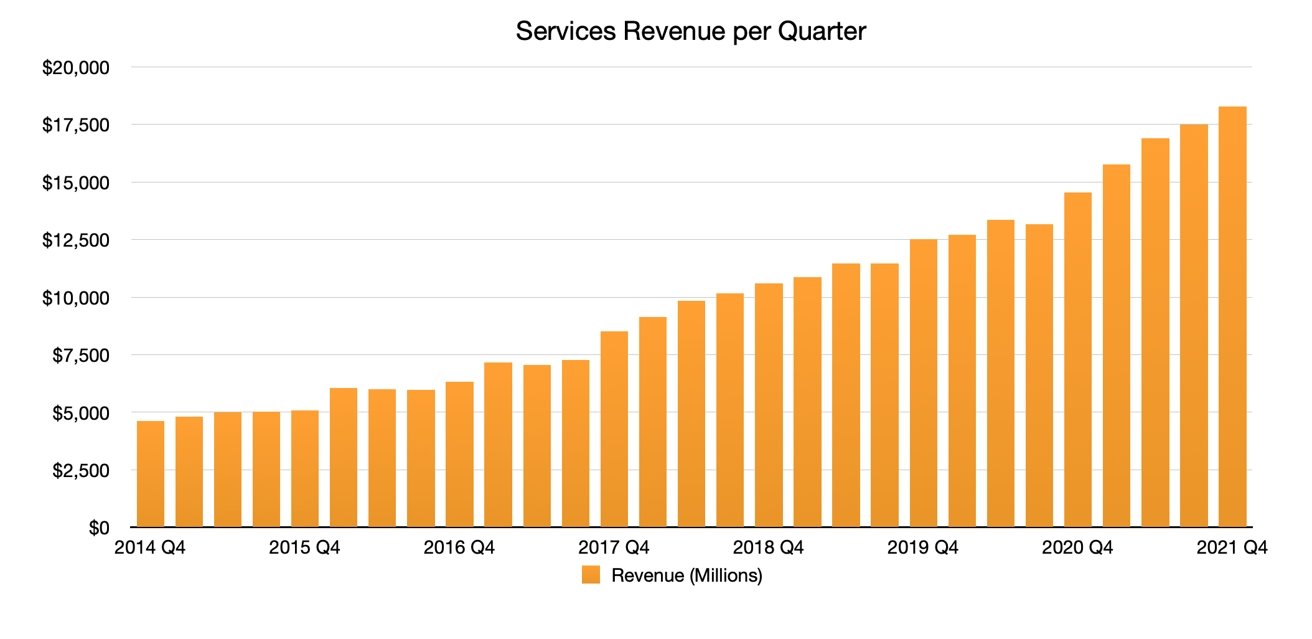

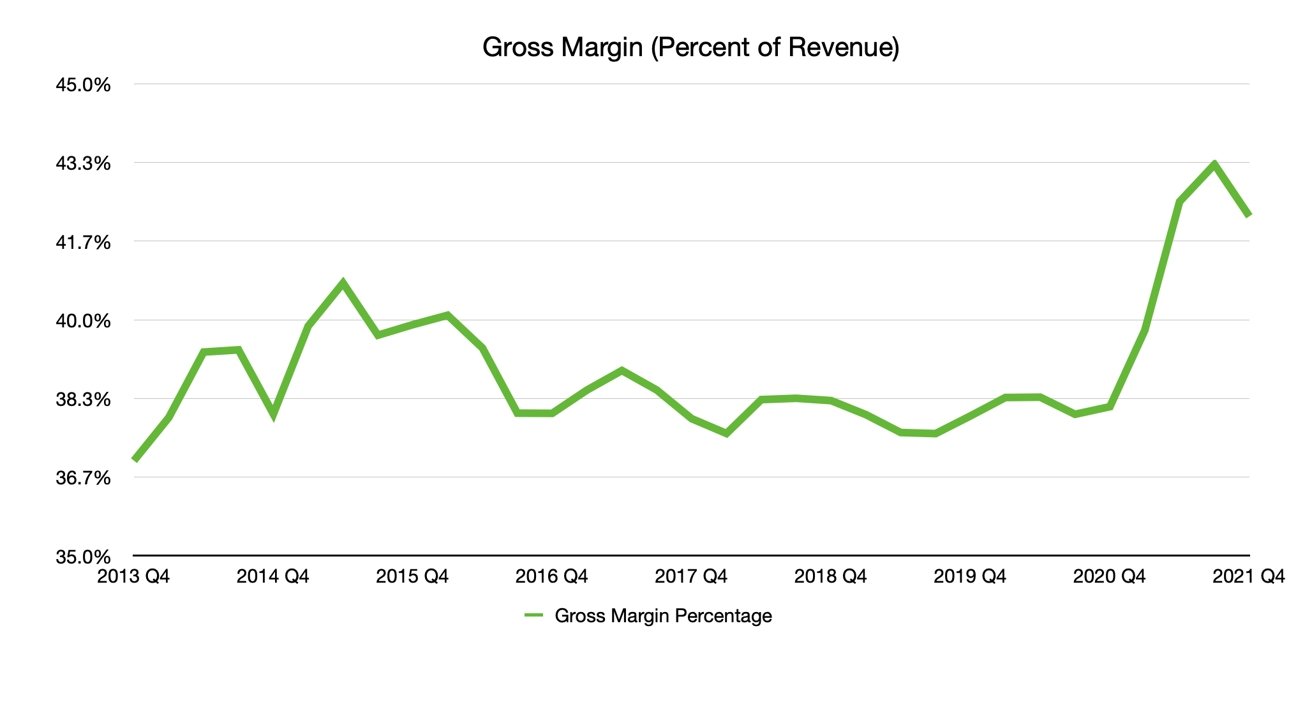

Despite the overall revenue miss, many of Apple's other products hit or exceeded expectations. While iPhone revenue also missed analyst targets, it was still a hefty increase over 2020. Apple's iPad, Mac, and Services revenue also rose year-over-year, with the latter two product categories reaching all-time highs.

Annually, Apple reported total 2021 sales of $365.8 billion, up a massive 33% from $274.5 billion the previous year. Although the company did not provide formal revenue guidance for the December quarter, it said it still expects healthy demand.

Here's what financial analysts thought about Apple's revenue miss, and what they believe the company's future will look like in the following quarters.

Katy Huberty, Morgan Stanley

Apple's September quarter was in-line with expectations "under the hood," according to Morgan Stanley's Katy Huberty. That's once you take into account the supply chain headwinds Apple faced during the quarter, she says.

While supply chain issues will likely dominate headlines, Huberty says the more important factors to the Apple stock are robust Services growth, guidance suggesting an in-line December quarter, Chinese demand outpacing other regions, and signs that point toward a stronger-than-seasonal March quarter.

On the back of the revenue miss and ongoing supply snarls, Huberty has lowered her 2022 revenue and earnings-per-share estimates to $387.7 billion and $5.76, respectively.

Her 12-month Apple price target has also fallen to $164, from $166. However, she maintains her Overweight rating of the Apple stock.

Daniel Ives, Wedbush

The main issue affecting Apple is not demand for its products, but its ability to meet that demand with supply, says Wedbush analyst Daniel Ives. The analyst calls the current supply chain situation a "black cloud" that's affecting every tech, auto, and consumer company.

Ives believes Apple is seeing demand outstrip supply by about 10 million iPhone units globally. However, beyond the total revenue and iPhone revenue, the analyst notes that Apple's other products and its Services business still came out ahead of his expectations.

The analyst believes the issues are transitory, and in no way affects his long-term bullish view on Apple. Ives still expects the company to hit a $3 trillion market capitalization in 2022.

Ives maintains his 12-month Apple price target of $185 and his Outperform rating for the stock.

Krish Sankar, Cowen

Apple's fiscal results for the September quarter were "overshadowed" by the $6 billion revenue miss, and a similar impact on the December quarter will likely be a main focus going forward. Despite that, Krish Sankar of Cowen believes that robust demand can still drive healthy growth.

The company's revenue results were 2% below expectations, though EPS was in-line with Wall Street expectations. Sankar notes that the $6 billion in lost revenue was higher than supply constraint estimates of about $3 billion, and primarily affected the iPhone, iPad, and Mac.

Despite all of that, Sankar believes that strong consumer demand and a higher average selling price (ASP) can still growth 7% year-over-year growth in the fourth calendar quarter of 2021, which corresponds to Apple's first quarter of the year and the busy holiday shopping season.

Sankar has revised his December quarter sales estimate to $119.1 billion, and his EPS forecast to $1.90. He maintains his 12-month Apple price target of $180.

Samik Chatterjee, JP Morgan

Apple missed both consensus revenue expectations and JP Morgan's Wall Street-high forecast. However, lead analyst Samik Chatterjee says that Apple's guidance of a "very solid" growth in the December quarter should tell investors that the effects are only temporary.

More than that, the supply constraints will likely only push the timing in revenue and demand into future quarters, Chatterjee says. He believes that the component pressures aren't likely to affect overall demand for the iPhone or Mac.

To reflect that, Chatterjee has raised his quarterly revenue and earnings estimates for the upcoming fiscal periods, particular Q1 2022. Although the timing of the strong iPhone 13 cycle has been delayed, the analyst believes the magnitude of upside on Apple's stock remains unchanged.

Chatterjee maintains his Top Pick rating for Apple and 12-month price target of $180.

Harsh Kumar, Piper Sandler

Apple's revenue miss in the September quarter is a rare occurrence, says Harsh Kumar of investment bank Piper Sandler. Despite the supply chain constraints bleeding into the December quarter, Kumar still believes Apple is well-positioned to see year-over-year growth and revenue records.

While the supply issues were larger than expected in Apple's Q4 2021, there are signs that it will have a relatively mild effect on the company. Kumar points toward the better-than-expected Services revenue, as well continued strong demand for its hardware products.

Kumar says that Apple's focus on the consumer, as evidenced by CEO Tim Cook's answers to analyst questions, is why the company's installed base grows each quarter. It's also why he believes that demand for the company's products won't perish amid the supply snarls. In other words, the revenue miss won't have a "material impact" on Apple's business.

The analyst maintains his 12-month Apple price target of $175, and says the firm is a buyer on any Apple stock weakness.

Gene Munster, Loup Ventures

Stripping out the noise of supply problems reveals a sustainable growth trend for Apple, says Gene Munster, analyst and partner at Loup Ventures. He says the quarterly earnings played out as expected, with favorable demand muted by tight supply.

However, behind the headline news of the problems continuing into the December quarter is the reality that "Apple's business and outlook are stronger than ever," Munster says. He believes Apple will grow comfortably ahead of Wall Street expectations in 2022.

Normalizing for supply headwinds, Munster says Apple is seeing underlying growth in the mid-teens. Because of those factors, the analyst believes the big picture of Apple driving the digital acceleration is unlikely to change.

Munster maintains his 12-month to 24-month Apple price target of $200.