Apple Card is the subscription that pays you to use it

Daniel Eran Dilger

Daniel Eran Dilger

Apple Card works just like any other Apple Pay account, but the software experience Apple is creating around it to enhance digital banking represents both a new Services venture and also an additional reason for users to keep buying hardware. That's why Apple is paying its customers to use it.

Apple Card and the reverse subscription

Compared to the other new Services Apple announced in March — Apple Arcade video games, News+ periodicals and TV+ original content — Apple Card isn't a subscription. Apple Card is actually the opposite of a subscription: using it pays you back via Daily Cash rebates.

This "free money" comes from the merchants who accept credit cards. Whenever you pay with any card, the merchant accepting your payment pays the card-issuing bank a fee. It's common for card issuers to offer buyers "cash back," which returns part of the fee collected to the buyer.

The cash back idea — along with no annual fee — was devised by Sears in the mid 80s when it introduced Discover in an attempt to break into the card business. By offering users cash back, it could attract customers otherwise happy with their existing cards. Additionally, the cash back promotion served as an incentive to spend more.

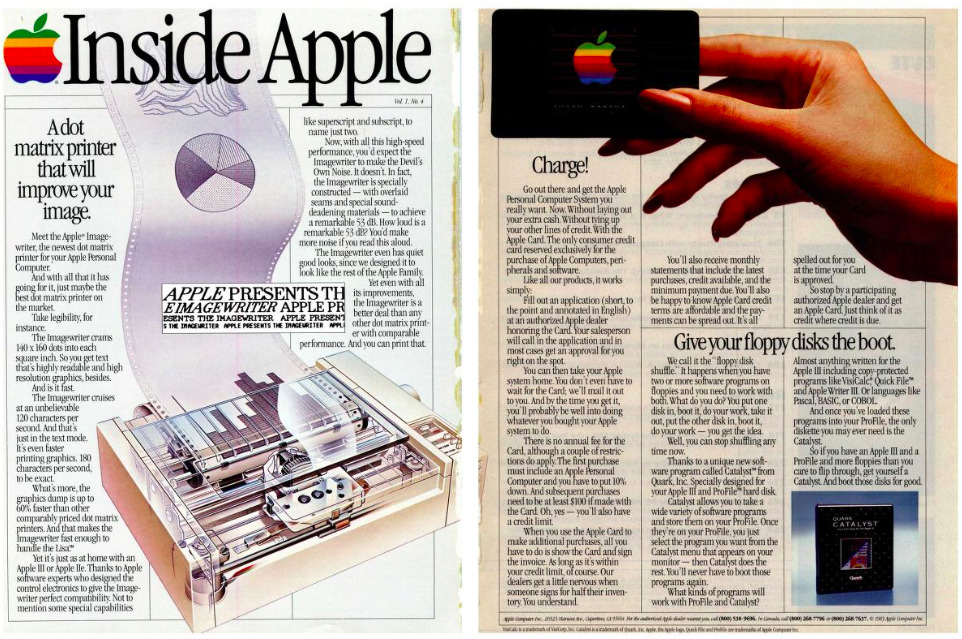

The idea of using credit to not just finance but incentivize consumer behavior was also explored by Apple. A 1984 Byte advertisement outlined "Apple Card," a credit card exclusively for buying "Apple Computers, peripherals and software." Twenty years later, Steve Jobs proposed a vanity credit card that paid out points for use in buying iTunes songs. Today a variety of cards offer some system of rewards in the form of points, airline miles, cash back or other incentives.

Apple's original spin on the idea of cash back is to make rebates immediate and obvious, so you are aware that you are "getting money" every time you use it. But it also has a second component: rather than simply applying your cash back to your account, the Daily Cash credits are loaded onto your separate Apple Pay Cash account. That's the personal spending account Apple earlier set up with Discover to enable free person-to-person Apple Pay transactions similar to PayPal or Venmo.

Offering its vast installed base of the world's most affluent buyers a new Apple Card account is therefore a two-pronged strategy to induce Apple Pay transactions: when you make a purchase, a small rebate is applied to Apple Pay Cash, encouraging you to use that money to pay a friend or split a tab using a second Apple Pay transaction.

Apple wants to encourage NFC Apple Pay transactions, but more importantly it wants to make using Apple Pay routine. The company has previously noted that in countries where there's an NFC transit system driving a critical mass of transactions, Apple Pay is more rapidly adopted as a payment system for other purchases, too.

Apple Pay and NFC vs the Mag Stripes

Apple Pay has been working to push the world toward more secure NFC transactions, which never expose your account number and protect the near field wireless transaction with an encrypted conversation between the terminal reader and a device's silicon "secure element."

However, much of the world — including a lot of the United States — is still stuck in the really old world of 1960s-era magnetic stripe transactions, which requires a physical card with a stretch of old cassette tape stuck on the back that can be read by a magnetic head in a credit card swipe machine.

That status quo at the launch of Apple Pay in 2014 informed Samsung's plans to acquire LoopPay, a company that had developed a way to fake a magnetic swipe by generating an encoded magnetic field conveying the same data recorded on physical credit cards.

Apple — like Google — focused entirely on NFC, meaning that if you have a card enrolled in Apple Pay and a vendor doesn't accept NFC payments, you have to pull out your physical card to either swipe it or insert it to use the card's EMV chip.

Apple wasn't simply trying to move all transactions to its devices; it was purely interested in promoting NFC as the payment solution. One of the benefits of only supporting NFC is that unlike Samsung, Apple doesn't have to include and support a second mag stripe reader system on its devices, now and into the future.

Apple is notorious for killing legacy and aggressively dragging its users kicking and screaming into the future. If the world were being lead by Samsung, we would never need to phase out mag stripes, and probably wouldn't. But by shifting its large, affluent base of users exclusively to NFC payments, Apple can make the future happen sooner, just as it did back in 1998 with USB, and now with USB-C.

Many pundits found it very convincing that Samsung would outperform Apple in mobile payments by offering legacy support for the once-ubiquitous old mag swipe readers. Three years after it adopted LoopPay's technology on its Samsung Pay enabled phones, however, Samsung's share of mobile wallet transactions was at 17% compared to 77% for Apple Pay.

Certainly part of that disparity is due to Apple's much larger installed base of premium users. Virtually all modern iPhones in use support Apple Pay; Samsung Pay is limited to the company's higher-end Galaxy S and Note flagships, a much smaller base of users that's only about a sixth of all Samsung phone buyers. That's another example of how Samsung's impact on the future of tech is far lower than its shipments would suggest.

However, NFC use isn't simply a matter of technology availability. Google pioneered NFC support for Android long before Apple Pay was introduced, and yet despite broad support for NFC on various Androids, the same report noted that Google Pay adoption was only at 6%.

The real challenge for inducing NFC adoption wasn't merely rolling out technology. It was changing behavior, both in convincing buyers to use it and in convincing banks and merchants to support it. That's been the task of Apple VP Jennifer Bailey, the executive in charge of Apple Pay.

It certainly helped Apple that Google had spent years and tons of money trying to promote NFC. However, Bailey's group has also worked to promote Apple Pay to users. Most recently it has worked to link Apple Pay to common transactions, notably transit fares and the area of "access," which uses NFC to enable campus, hospitality and enterprise Wallet app ID cards to open doors as well as make payments.

NFC is used at Apple Park to control access. Apple has also issued NFC badges to attendees at its Worldwide Developer Conference, but these aren't loaded into Wallet because it appears there's currently no way to install a globally unique, non-transferable pass to a specific device. We will likely hear more about Apple Pay and NFC at WWDC19, which is now just over a week away.

The next article takes a closer look at the physical Apple Card that users will be issued and how even this legacy shim acts to promote Apple Pay as the preferred transaction system.

Mike Wuerthele and Malcolm Owen

Mike Wuerthele and Malcolm Owen

Amber Neely

Amber Neely

Bon Adamson

Bon Adamson

Andrew Orr

Andrew Orr

Malcolm Owen

Malcolm Owen

33 Comments

I’m in the market for a new 27 inch iMac. Doesn’t have to be the fastest processor but I do want SSD storage. The day I get my Apple Card is the day I get my new iMac.

Can the Apple Card be used by companies as their access card to let employees get into offices that are behind doors which are unlocked by cards and card readers? Just an idea.

My only complaint is the titanium card. I mean it’s cool and all, but I don’t really want to have something in my wallet heavier than a plastic card. But I’m in Canada so it probably will be a long time before it’s available here anyways. Still waiting for Apple Pay Cash ffs.

The Marriot Bon Voy App seems to be doing this as well, or at least it appears to be. I open the app, tell it that I want to unlock my hotel room door, it says it’s ready, and I place my X against the door sensor - rrrrr-click! And I’m in! Slick shit!