After pullback, even 'value' investors should eye Apple stock - report

Neil Hughes

Neil Hughes

Analyst Brian White with Ticonderoga Securities issued a note to investors on Monday noted that it's a good time to look at AAPL stock, given the pullback in shares last week after the announcement last week that Jobs would take a medical leave of absence. Even without Jobs, White sees Apple's stock rocketing to a new high of $550 in the next 12 months, based on a strong product lineup and growing sales.

"Jobs's medical leave of absence... overshadowed a big December quarter print and March quarter outlook," White wrote. "Although there could be further selling pressure, we believe the risk-reward is becoming so favorable that even value investors should begin buying the stock."

The analyst said he believes Jobs has been building a strong team that will be able to successfully lead Apple into the future. He also believes that were it not for concerns about Jobs' health over the last few years, AAPL stock would never be trading at "such a discount."

"With Apple's hot product portfolio, we expect the company to continue outperforming the tech sector over the next several years," he said.

For fiscal year 2011, Ticonderoga Securities is projecting 56 percent revenue growth and 54 percent earnings per share growth. That growth will be driven by the new CDMA iPhone 4, set to debut on the Verizon network in the U.S. on Feb. 10, followed by anticipated launches of the iPad 2, new MacBook Pros, and the iPhone 5.

In particular, White sees strong sales of the iPhone and iPad driving the much documented "halo effect" that drives new consumers to the Mac platform. White said the Mac appears to be going through a "renaissance," and he expects that performance to only improve in the coming years. He sees Apple selling 16.7 million Macs and 27.4 million iPads in fiscal year 2011.

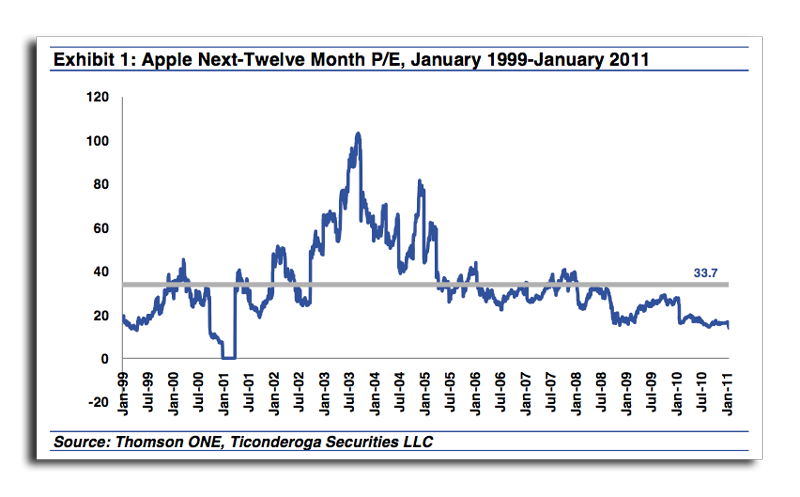

Ticonderoga Securities' $550 price target is based on an earnings per share estimate plus net cash per share of $63.98. White's numbers equate to a straight price-to-earnings ratio of 22x, which is below the 26x multiple AAPL stock has seen over the last six years.

Wesley Hilliard

Wesley Hilliard

Mike Wuerthele and Malcolm Owen

Mike Wuerthele and Malcolm Owen

William Gallagher

William Gallagher

Amber Neely

Amber Neely

Malcolm Owen

Malcolm Owen

76 Comments

try WOZ

I'd like to think he's right, but the numbers don't reflect current realities. He's looking for AAPL to appreciate faster than their EPS (67% vs. 54%). The truth is, over the last several years, the opposite has occurred. Why he thinks multiples will actually increase at this stage is hard to figure.

I'd like to think he's right, but the numbers don't reflect current realities. He's looking for AAPL to appreciate faster than their EPS (67% vs. 54%). The truth is, over the last several years, the opposite has occurred. Why he thinks multiples will actually increase at this stage is hard to figure.

If you don't already, read Asymco - http://www.asymco.com/

Today talking about a hypothetical about acquiring Apple due to its vast undervaluation in terms of trailing earnings. Its not serious about a takeover or going private but does interesting analysis of APPL and its very low valuation vs. comps and outlook.

If you'd taken Apple private 2 years ago, you'd have paid off most (80%) of the debt incurred by now. Today you could do it in 4yrs at current trends. With the lack of a cap on Apple's growth in all product lines (tiny market share today, massive growth in emerging and new APPL markets, brand, satisfaction rates, strategy, etc.) there is little real reason to doubt it would be plausible (if highly improbable).

Anyway - main point - Asymco is brilliant (and filled with some of the best commenters on the Web) - Don't ruin it, y'all ;-)

try WOZ

I think Woz is visionary in a different way -- he looks for things he wants to do/have.

Jobs looks for things he wants that are what others will buy!

I think this goes back to the garage days -- Woz built a computer for the challenge and to have a computer of his own -- Jobs wanted a computer to sell.

I'd like to think he's right, but the numbers don't reflect current realities. He's looking for AAPL to appreciate faster than their EPS (67% vs. 54%). The truth is, over the last several years, the opposite has occurred. Why he thinks multiples will actually increase at this stage is hard to figure.

Apple growth has been rather unusual in that large companies generally hit a plateau and become investment stocks instead of growth stocks. The iPhone turned them into a growth company almost overnight, but that is going to level out pretty soon I would imagine.