Wells Fargo resumes coverage of Apple ahead of 'biggest product cycle' ever

Josh Ong

Josh Ong

Analyst Maynard Um reinitiated coverage in a note sent to AppleInsider, rating Apple as Outperform with a valuation range of $640-660. The investment bank believes shares of Apple are currently undervalued and will see growth after its expected "biggest product launch" in both company and industry history with the next-generation iPhone, which is expected to arrive in October.

"We believe Apple's combination of brand, innovation, and ecosystem are unmatched and see the company as well-positioned to continue to take value share in its core smartphone, tablet, and PC markets," the analyst wrote.

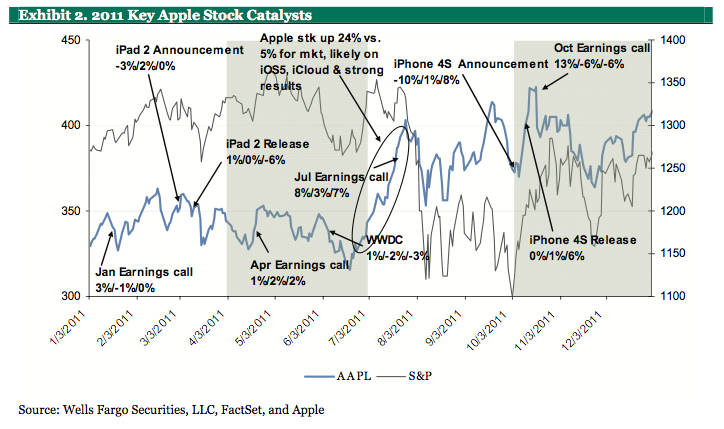

Wells Fargo research has shown that Apple stock jumps 23 percent on average from the date that a new iPhone is launched to the day after earnings results for the handset's first quarter are announced. Um expects Apple's next iPhone to include a "complete form factor redesign" and "true 4G" cellular technology. He believes the handset's launch will be boosted by an anticipated more-rapid carrier rollout than previous years and buzz from the device possibly being one of the last products that late CEO Steve Jobs had a hand in designing.

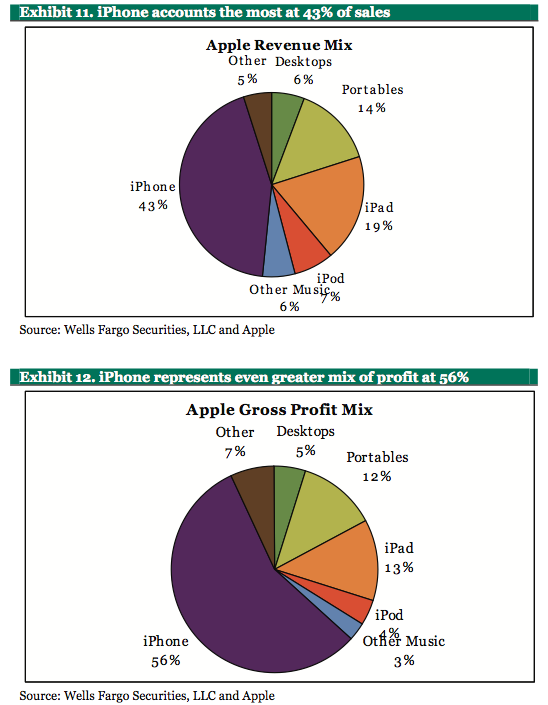

Apple's iPhone line accounted for 43 percent of its revenue and a whopping 56 percent of its gross profit in 2011, according to Wells Fargo's estimates. The firm believes Apple is on track to continue a "healthy pace" of growth in iPhone unit shipments.

In addition to the iPhone, Um expects Apple's other upcoming products to contribute to growth. He believes a so-called "iPad mini" is on its way, as well as new iMac, Mac Pro and iPod models. A much-rumored "iTV" Apple television set is not expected by the firm until calendar 2013 at the earliest.

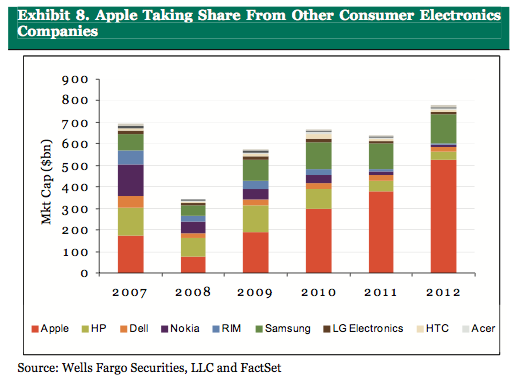

An analysis of the TV market by the firm came to the conclusion that Apple could take as much as $50 billion in market capitalization from other television makers if it released its own model. Since the arrival of the iPhone five years ago, Apple has taken large chunks out of mobile phone vendors' market caps, especially those of Research in Motion and Nokia.

Apple is expected to continue to grow market share in the PC market as a result of an increase in "overall consumer adoption" of the company's products, spurred in part by an iPhone and iPad halo.

The analyst also pointed out that Apple has a "cushion" for its gross margins in the form of its product warranty costs. The iPhone maker has apparently been over-accruing product warranty costs as compared to its actual expenditures. If the company experienced downward pressure on its gross margins, it could reduce the amount it accrues and thereby raise its net revenue.

Though Wells Fargo sees Apple in a very strong position, it did mention several potential risks that the company faces. For instance, drop in the average selling price (ASP) of the iPhone due to decreased demand or a reduction in carrier subsidies, could have a drastic impact on Apple's revenue and margins. Apple's growth could also slow because it faces tougher comparisons as a result of the impressive growth it posted in previous quarters.

Other risks highlighted by Um included: evolutionary rather than revolutionary innovation, Apple's numerous legal disputes, the possibility of higher operating expenses, potential for supply constraints and the threat of broader macro-economic slowdown.

Malcolm Owen

Malcolm Owen

Amber Neely

Amber Neely

Marko Zivkovic

Marko Zivkovic

David Schloss

David Schloss

Wesley Hilliard

Wesley Hilliard

Mike Wuerthele and Malcolm Owen

Mike Wuerthele and Malcolm Owen

23 Comments

I think the next iPhone is going to blow the doors off all previous iPhone launches. With an expected increase in screen size coupled with 4g/LTE, a huge number of current iPhone users still under contract will go for the gusto and suck up the price to upgrade anyway, many more than normally would. At least that's my opinion.

At the same time those older 4's and 4S's may not carry the expected resale prices that iPhones traditionally have. They certainly won't be as attractive with a completely new form factor on the market. That's of no consequence to Apple of course.

Their iPad revenue and profit seems low to me.

I've seen a few notes lately that iPad sales may not be as robust as might be expected. I have no idea if there's facts behind those comments.

It's apparent this analyst is not looking at Apple's current or potential share of addressable markets in determining the price target.

How do these guys keep their jobs when they can't even project, within any range of reason, Apple projections over the next year? How is that possible?

Much as we like to bag on “analysts,” that all sounds pretty reasonable.

(I bet iPhone 4 and 4s will still sell OK: the years-old iPhone 3G design still sells like hotcakes! And it looks like the iPhone 7—by my count since there were two iPhone 4 versions which even had different placement of side buttons, even prior to the 4s—will be in the same styling family as the iPhone 4/4s, so they won’t really look “old.” Pretty much timeless designs.)