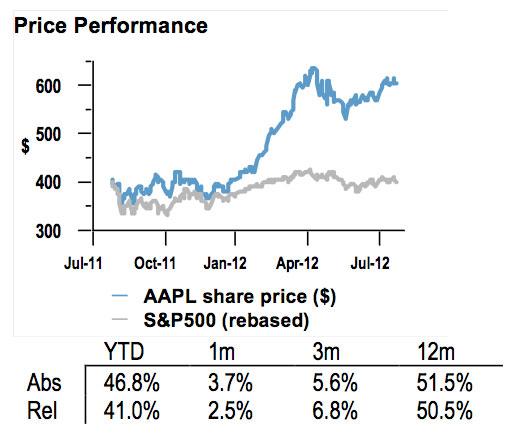

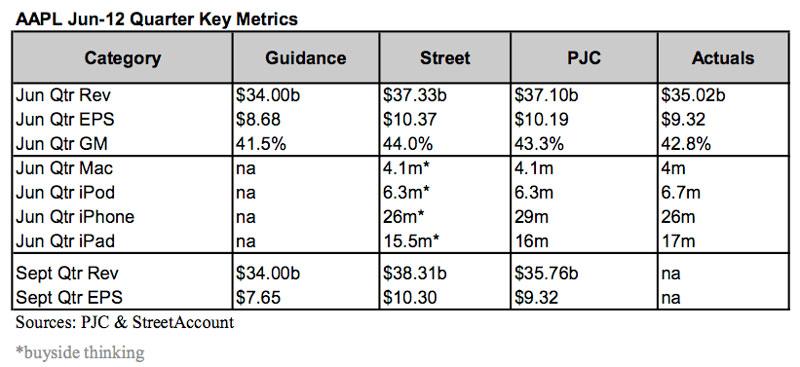

In what the market viewed as a rare miss, Apple reported sales of 26 million iPhones, 17 million iPads and 4 million Macs on Tuesday, resulting in a profit increase of just over 20 percent to $8.8 billion. Though the iPad sales represented a new all-time record, they were about in line with investor expectations, while iPhone and Mac sales fell short.

In reaction to Apple's third quarter of fiscal 2012, a number of analysts have lowered their price target for AAPL stock. Market watchers generally remain optimistic about Apple's near-term future, but await the anticipated launch of a next-generation iPhone and the lucrative holiday shopping season.

Morgan Stanley

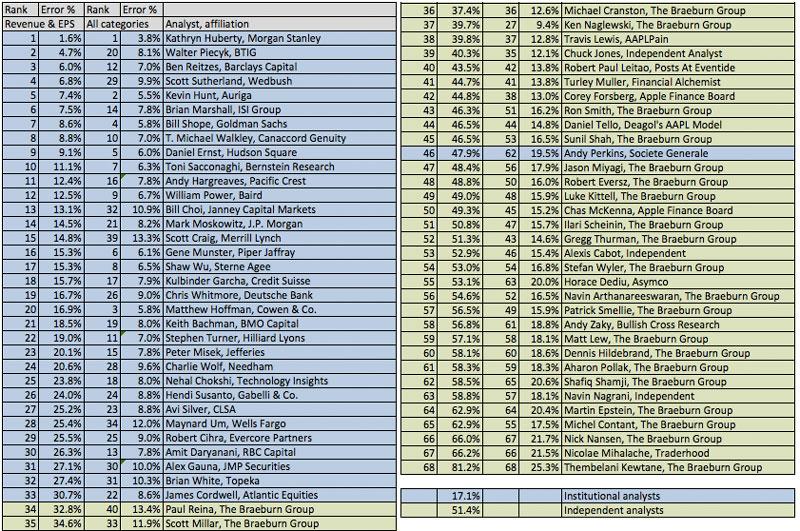

The most accurate prediction ahead of Tuesday's earnings report, according to tracking from Philip Elmer-DeWitt of Apple 2.0, was Morgan Stanley's Katy Huberty, who was off by 1.6 percent on revenue and earnings per share and 3.8 percent on all categories, including product sales.

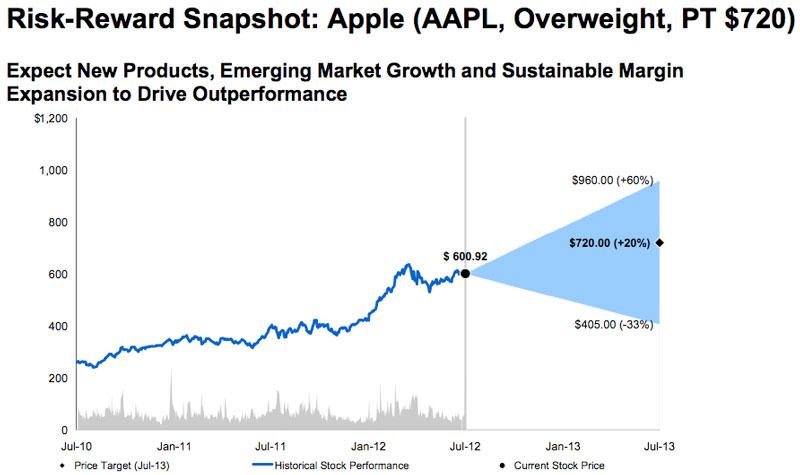

Huberty issued a note to investors after Tuesday's earnings call in which she said Apple's "near-term pain" will be "offset by long-term gain." She sees a base-case valuation of AAPL stock at $720, with a bull-case of $960.

Huberty believes that investors should own AAPL ahead of the new iPhone product cycle. In past years, shares of AAPL have increased 30 percent on average and outperformed the S&P 500 by 27 percent in the three months leading up to iPhone product announcements.

"We expect similar strong performance ahead of iPhone 5 which we believe will feature LTE connectivity and a new form factor (thinner, new casing)," Huberty wrote. "While weaker than expected Jun/Sept (quarter) results are disappointing near-term, it potentially sets up for even stronger sequential results in the December quarter."

With the launch of a new iPhone expected to come about a year after the debut of the iPhone 4S, Huberty and other analysts are already overlooking Apple's current September quarter. But they also expect that Apple will have launched its next-generation iPhone before the company reports September quarter results in mid-to-late October, which should help offset any potential future disappointment.

Barclays

Analyst Ben A. Reitzes ranked third in Elmer-DeWitt's comparison, missing revenue and earnings per share by 6 percent, and all categories by 7 percent. Reitzes said in a note to investors that he believes the below-consensus results reported by Apple were a result of a "pause" in iPhone sales, as well as weaker-than-expected gross margins, at 42.8 percent.

He also noted that Apple has gone back to being "very conservative," and issued cautious guidance for its fourth quarter of fiscal 2012. Apple has projected revenue of about $34 billion, which is below his estimate of $38.2 billion, as well as market consensus of $38 billion.

"Although we believe that investors were prepared for typically conservative guidance on the top line in Apple's range, Apple's (earnings per share) expectations seem to reflect lower-than-expected gross margins, which may raise some concerns," he said. "We believe the next big product cycle with the iPhone 5 will have a bigger impact in the December quarter."

He believes investors will be disappointed by Apple's results in the near-term, but he's already looking forward to the next iPhone launch.

"We still believe that Apple is perhaps the most disruptive company in tech and is poised to gain more share in smartphones, tablets and PCs, but we will be watching the developing situation closely," Reitzes said.

ISI Group

Analyst Brian Marshall questioned whether Apple may be entering a cycle of "180 Days of Enlightenment" vs. "180 Days of Darkness." He ranked sixth on Elmer-DeWitt's calculations, and has reiterated a "buy" rating for AAPL stock, albeit with a price target reduced from $750 to $710.

Now, he believes Apple's business model could have two distinct patterns, in which half of the year the company seeks breakout growth, and the other half is not as strong.

"The 'flip-switch' of these two periods being the timing of the launch of the new iPhone model (e.g., we still expect the iPhone 5 in early October)," Marshall wrote.

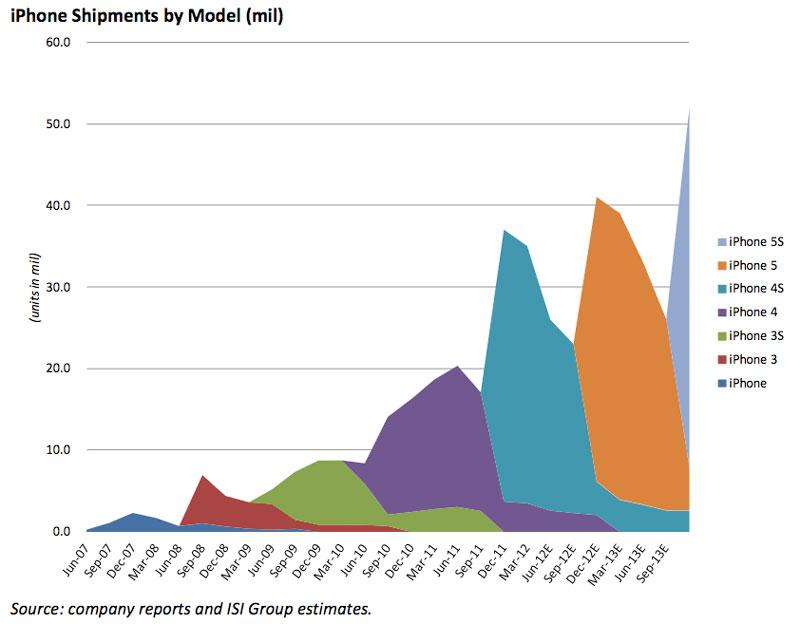

When the next iPhone launches, Marshall now believes Apple will sell a total of 41 million units in the holiday quarter. That's down from his prior prediction of 51 million, a more cautious forecast due to anticipated adoption of in-cell touch panels, a macroeconomic slowdown in China, and a weak European economy cited by Apple Chief Executive Tim Cook on Tuesday.

J.P. Morgan

Analyst Mark Moskowitz, who was ranked 14th by Apple 2.0, said he expects shares of overweight-rate AAPL stock to "cool off" and potentially remain in a "holding pattern" until the launch of Apple's next-generation iPhone. He said Apple's earnings miss announced on Tuesday was driven by slowing iPhone sales ahead of a next-generation launch, higher mix of lower-margin iPad sales, and weak macroeconomic conditions in Europe, Australia, Brazil and Canada.

"We think that Apple's commentary on last night's call provided support for the stock's respective bull and bear camps," Moskowitz said. "In the near term, we think that the bear camp wins, likely pressuring shares of Apple. Unfortunately, as investors look beyond Apple, we think that the company's commentary supporting the bear camp could result in broader selling pressures in tech stocks and beyond."

Moskowitz lowered J.P. Morgan's price target on AAPL stock on June 28 to $695, the first time the firm had lowered a target for Apple since 2009. Moskowitz said on Wednesday that revision wasn't low enough, and reduced his price target once again to $675.

"While lowering our estimates and price target again, we think that our long-term thesis on Apple remains intact," he said. "We are concerned that the ride could be bumpy in the near term, though, particularly given lingering macro risks and questions related to the (average selling price) trends."

Piper Jaffray

Analyst Gene Munster expects that investor concern about the September quarter will ease as the launch of Apple's next-generation iPhone draws closer. Munster came in 16th in Elmer-DeWitt's breakdown of analyst forecasts for Apple's quarter.

"While the concern is legitimate, we believe it is largely irrelevant because iPhone will rebound in the (December '12) quarter as it has in the past," Munster wrote. "Importantly, (September '12) will likely be reported after the iPhone 5 release which should more than outweigh the September iPhone number."

Munster has adjusted his expectations to account for Apple's September quarter guidance, and also for a longer-term shift from the Mac to the iPad. He now believes the longer term Mac growth rate will be around 10 percent, as iPads take some sales to Macs.

He also does not believe that Apple's guidance hints at a launch of the next-generation iPhone in September. He continues to believe that Apple's next iPhone will debut in October, about one year after the launch of the iPhone 4S.