Daniel Eran Dilger

Daniel Eran Dilger

Since Apple announced its industry-leading earnings for fiscal Q3 on July 21, the company's stock price collapsed by about a third, encouraging facile analysts to predict further losses. In reality, Apple shares are being bought up at a massive discount by the company itself, in a clear bet on future appreciation.

This all happened before

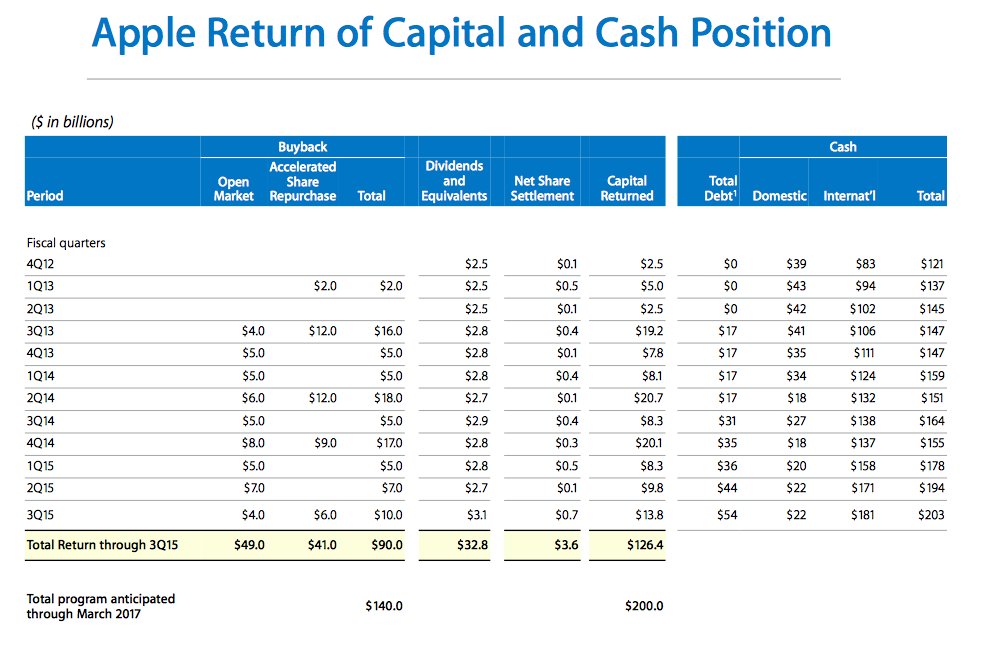

The last time Apple's stock nose-dived after an earnings release, in January 2014, the stock panic shaved less than (a split adjusted) $10 off of Apple's share price. The company responded by scrambling to spend an incredible $18 billion to take advantage of faithless investors' extreme gullibility on behalf of its loyal shareholders.

That action paid off tremendously. Apple bought up over 30 million shares at prices below (a split adjusted) $75, right before the stock again returned to more rational prices.

Over the current quarter, Apple's stock price has plummeted by as much as $25 at one point, effectively erasing any appreciation contributed by the blockbuster sales of iPhone 6 over the past year (albeit never reaching below $100, well ahead of the last buyback-inducing stock panic trough). It's not hard to imagine how Apple has responded to this opportunity.

Despite continued massive cashflow from operations, Apple continues to borrow money by the billions internationally, with only one possible intent: to again buy back as many shares as possible before the market comes to its senses.

Borrowing capital at interest rates below 2 percent to buy shares that are currently languishing at a price that analyst consensus targets expect to rise by around 30 percent over the next year (to $150, according to public market data) is a no-brainer, particularly for Apple's executives who fully grasp the potential of the company in the global markets it is operating across.

Source: nasdaq.com

Source: nasdaq.comIf Apple were actually facing a upcoming barrier of slowing growth and a collapse of demand in China, rather than buying back its own stock it would be scrambling to acquire other companies with an actual, apparent strategy the way Google has been almost blindly gobbling up its Alphabet soup over the past several years as Android has done nothing and every one of its hardware efforts have all imploded into embarrassing ruin.

Apple is also making acquisitions (albeit with a discernible strategy), but Apple's biggest ongoing acquisition over the past several years has been Apple itself, to the mind-blowing tune of $90 billion. That pace isn't expected to slow down. Instead, Apple says it expects to spend at least another $50 billion over the next seven quarters.

It's not just Apple buying back its own stock. In Q3 ending in June, Apple initiated another $6 billion in Accelerated Share Repurchase, a deal handled by bankers on the company's behalf, who themselves are are incentivized to buy up those billions of shares at as low of a price as possible.

So it's not just the smartest money guys in the room at Apple who are buying up Apple stock, it's also some of the smartest financial minds in the banking world who are buying up Apple at Apple's request. With all that going on, it probably shouldn't surprise anyone that there's a lot of talk floating about that's suggesting that Apple's stock price "ought to" probably dip some more, because no free advice is ever given that doesn't benefit those handing it out.

Over the past quarter when those billions in buyback ASRs were outlined, Apple's stock price was reaching toward all time highs, suggesting that those ASR buybacks really began to accelerate only after Apple's shares began to tank this quarter. It will be shocking if Apple does not also announce a new surge in buybacks this quarter, when it announces earnings in October. The only thing that could possibly hold the company back from doing so would be its inability to raise capital fast enough.Dips in Apple's stock price are a good thing for long term investors: it means that the company itself is concentrating the value of its outstanding stock

That highlights why dips in Apple's stock price are a good thing for long term investors: it means that the company itself is concentrating the value of its outstanding stock with capital in a market where prevailing low interest rates would otherwise provide little return on Apple's massive piles of money.

While U.S. tax law is currently making it unattractive for Apple to spend its foreign earnings on buybacks, that pile of overseas capital is effectively guaranteeing bonds that raise cheap capital Apple can use to buyback its shares at an extreme discount.

One indication that the market (and the consensus of analysts) haven't really grasped what's happening with Apple's buybacks is the fact that Apple's Earnings Per Share have consistently exceeded their expectations every quarter this year.

Source: nasdaq.com

Source: nasdaq.comApple vs Fantasy Apple

Apple's incredible growth (double that of the industry at large overall, and even greater when just looking at iPhones), which continues despite its now vast size as the world's most valuable public company, seemingly should be reflected in its stock price.

Instead, despite outperforming every peer over the past four quarters in terms of profit power, stock pundits have taken to instead comparing Apple to a magical imaginary Apple that grows even faster than the real Apple, shaking their heads in great disappointment that the world's best managed, most profitable company isn't as good at they estimated it could be.

Remember, it's not their estimation that's wrong, it's that Apple didn't achieve numbers they imagineered, numbers that were actually just wrong in the real world. But pay no heed, that's how the market works. Using "percentages of growth" and other logical/statistical fallacies, you can be disappointed with greatness and enraptured with failure, convincing investors to flee from mountains of strong profitability into the comforting arms of frivolously burning pits of the ashes of cash.

Imagine a sports match where athletes are not compared against each other or even against world record holders, but against whimsical imaginary targets invented by coaches that have never even performed as athletes and don't even fully grasp how the game is played. That's today's stock market, at least where Apple is involved.

Conversely, gold medals are being handed out to a series of athletic hopefuls who are bedridden and in some cases comatose, simply because those same coaches have an extremely optimistic credulity in their future potential to score points, regardless of their dismal past past performance.

Two companies, two standards for fundamentals

One simple comparison: Apple's launch of the world's most successful consumer product ever, with no real signs of slowdown anywhere but the imagination of analysts who are regularly wrong, effectually has had virtually no impact on the company's stock price appreciation between today and its launch due to the recent stock price collapse ostensibly related to incredibly pessimistic concerns that the next iPhone might not exceed its blockbuster performance by a large amount.

Amazon, on the other hand, completely botched its likely last opportunity to release a competitor into that same market with one of the biggest and most spectacular flops ever seen in consumer electronics. Across the death spiral of Fire Phone (and Fire TV), Amazon stock has appreciated by over 60 percent. This is a company that has essentially never turned a profit.

Well, last quarter Amazon did manage to earn $92 million (on revenues of $23.18 billion). Apple earned $10.7 billion on revenues of $49.6 billion. Amazon stock leapt while Apple's fell.

Bloomberg Business subsequently raved that Amazon was the stock everyone was now running to as they abandoned Apple, due to the current percentages of change in stock price for the year, without even mentioning either number for profit or revenue, or either company's outlook, or the fact that Amazon's P/E is infinity while Apple's is insanity. Look, the stocks have changed directions! Follow! We're a website with free insight!

Next quarter, Amazon said it hopes to earn $70 million, but warned that it might also lose $480 million, or more than five times as much as it earned in the previous quarter. So who knows, really. Pull out your Apple stock and hand it to Amazon to see what happens!

Amazon isn't even in the terrible Fire Phone business anymore, but Apple is plagued with making most of its money on iPhone sales, which sounds like a grievous problem because everyone keeps saying that it is. Even worse, Apple is making lots of money in China, something that no other U.S. tech company has to really worry about.

China Concerns

Unrest in China's stock market appears to be weighing on Apple's stock. Given that Apple is really the only tech company to have any real success in selling products in China, and given that success has been absolutely blockbuster, concerns regarding the vast Chinese market sensibly affect Apple more than, say, Amazon or Google, neither of which even have a foot in the door of the huge Chinese smartphone opportunity.

Of course, those two companies have also earned virtually nothing on their entire, global smartphone efforts outside of China either. Both inside and outside of China, Apple is the only company making any real money on the scale of Apple. And Apple is growing while everyone else is increasingly struggling to turn a profit at all.

If Apple's business in China involved massive spending on public infrastructure or investment income from its unwinding stock market, there might be cause for concern. However, in reality Apple is selling China's vast emerging middle class technology products that, while perhaps luxurious, are broadly affordable. Apple is selling China's vast emerging middle class technology products that, while perhaps luxurious, are broadly affordable.

Look no further than young wage slaves in the United States to consider whether people on a limited income (or even people carrying exhausting, crippling student loan debt) aspire to save money by depriving themselves of the latest iPhone.

Even China's minority with exposure to massive stock market losses is unlikely to decide that the most pressing economic concern in their lives is whether they're spending the equivalent of about $30 per month financing a new iPhone or not, given that Apple's brand in China is a status symbol unmatched by anyone, let alone a third rate knockoff smartphone.

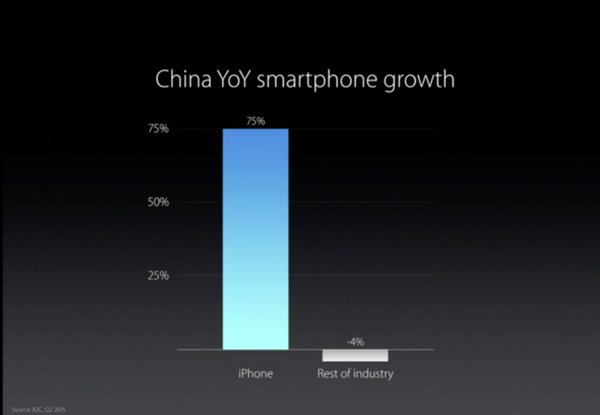

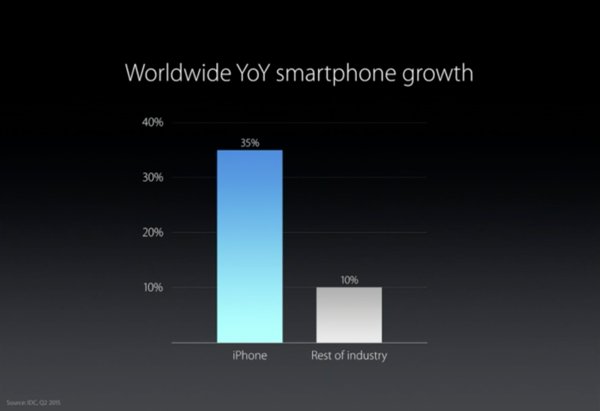

China's 4G mobile service continues to be built out from virtually nothing just a year or two ago. Incredible numbers of people are buying new iPhones to take advantage of it. Apple's market share in China could drop and the company would still be growing dramatically. Instead, Apple's growth is still outpacing the industry by a huge margin.

Source: Apple Event citing IDC data

Source: Apple Event citing IDC dataAnd outside of China, Apple's massively successful iPhone 6 launch, which has reclaimed market share in nearly every market, has helped to establish Apple's brand as shorthand for "customer satisfaction." Apple's only real rivals in smartphones are not only led by a disastrously poor series of rollouts by Samsung, but are also plagued by the malcontent associated with Android and its increasingly appalling reputation for security flaws that never get fixed by a company that doesn't seem to even care about it.

It's sort of like 2002's "Get a Mac" vs Windows XP malware crisis, but with a replacement Microsoft that's not even panicking to get a handle on the mess it created. If you recall how that worked out for Microsoft— even as it scrambled for years to patch up Windows XP's leaky holes— imagine a repeat where today's "Windows" platform has no financial motivation for Google to even address, even as its licensee and carrier partners are making any patchwork efforts by Android's primary developer essentially irrelevant to customers anyway, because they'll unlikely to ever get them.

Also witness how unsuccessful Microsoft has been in convincing Windows XP users to come back to Windows 7, 8, and 10 after getting a taste of a Mac or an iPad. Apple's computer sales growth is greatly outpacing PC sales and have been for years.

If somebody should be concerned about China, it should be the companies who have failed to make any inroads in the country or have been essentially blocked out by the State the way Google has.

Currency Headwinds

There are legitimate concerns in front of Apple, one notable issue being foreign currency headwinds. The U.S. dollar has been appreciating against a wide variety of other currencies, making Apple's exports more expensive. If this hadn't happened over the last two quarters, Apple earnings results would have been even better.

However, Apple has weathered unfavorable currency fluctuations better than many of its peers simply because it is so profitable, and it has the capital and credit to enter long term hedging contracts to mitigate risk. Additionally, it's unlikely that the situation will continue to worsen at the same rate going forward, given the impact the surging dollar already has on every other American company.

At the same time, energy costs are also continuing to fall, making Apple's international shipments and other transportation costs cheaper. The price of oil is expected to fall faster than the dollar can rise, offering some offset. And as oil falls, producer countries including Saudi Arabia are selling off their dollar reserves, blunting the dollar's rise.

Additionally, today's stronger dollars should also make it cheaper for Apple to invest in large infrastructure, production and lavish retail projects internationally, such as the surge in expensive retail stores Apple is working to build across China over the next few years.

Apple is expected to report its September quarter results October 19, which will include details on the size of its buybacks during the quarter and its performance leading up to new releases of iPhone 6s, iPad Pro and Apple TV, products which will largely or entirely contribute to the company's following fiscal Q1 2016, given their later than usual launches this year.

Until then, expect a lot of concerned handwringing worrying about Apple's future prospects, despite the fact that its competitors have never been weaker, its products have never been stronger, and it has never had more employees, more capital and a better ecosystem and retail network in place. It has to fail at some point, right?

-m.jpg)

Charles Martin

Charles Martin

Christine McKee

Christine McKee

Wesley Hilliard

Wesley Hilliard

Malcolm Owen

Malcolm Owen

Andrew Orr

Andrew Orr

William Gallagher

William Gallagher

Sponsored Content

Sponsored Content

44 Comments

Great Article - add to this Barron's comments this week on great product launch and the brilliant "leasing" plan introduced by Apple - Barron's expects a very large price jump in short time order ("Apple Shares Could Rally 50% on New iPhone Plan") -

This is an excellent summary of facts on the Apple financials front.

However, on the analyst front, less so. Most analysts cannot be predicting "further losses" since the 'consensus' analyst target -- as shown in the article -- is $150 against a current price of ~$112.

I realize we all love to hate analysts, but it is their wont to put these forecasts. Moreover, once those forecasts are out, the market getting to a so-called 'whisper' number is just a fact. It happens to all companies, not just Apple. Ultimately, the whisper number becomes the one to beat.

Also, almost very single market commentator or self-styled investment "guru" I've heard in the past few weeks -- even a short-seller like Jim Chanos, who has almost nothing nice to say about any company -- thinks Apple is a screaming buy. Yet, the stock does't move.

If one believes in the company and its future, buying at these levels is an incredible opportunity. But that presumes a buy-and-hold horizon of at least a few years, not lurching from quarter to quarter. But the author is also right: I hope Apple is repurchasing the heck out of its own shares.

You sir, are one of the few with the insight and knowledge to understand. It's awesome isn't it? To be this smart and tune out the noise for serious returns. Everyone, look to your left and right while you are in the car? Who has their eyes in their lap? 1 out of 3 I'd say in the younger demographic. It's far worse than most drunk driving and people STILL have to look at their phones. It's addictive and THAT is why Apple is so successful. Wall Street, CNBC shills, Bloomberg, everyone in the industry just wants your churn. F*** em.

In general a fear of shares happens when interest rates rise is spooking the markets.

"Given that Apple is really the only tech company to have any real success in selling products in China..."

Doesn't he mean 'non-Chinese' company? I thought a couple of their home-grown ones were doing okay...?