Neil Hughes

Neil Hughes

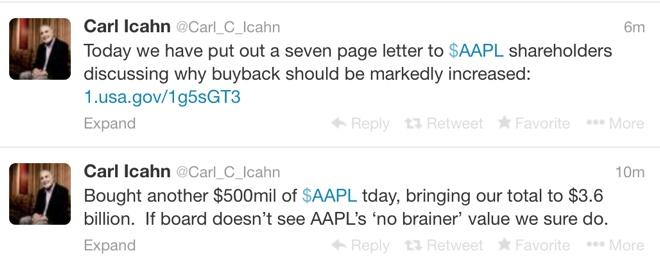

Activist investor Carl Icahn revealed on Thursday that he just invested another $500 million in Apple, bringing his stake in the company to $3.6 billion. Coinciding with the announcement, he issued a new 7-page letter to investors encouraging them to vote in favor of his share buyback proposal.

As he did on Wednesday to announce his large position in Apple, Icahn took to Twitter again on Thursday where he once again said he views the company as a "no brainer" investment. Icahn suggested that Apple's own board of directors may not see the company as such a strong investment, since they have not opted to spend more of their $150 billion in cash on a larger share buyback program.

Icahn also issued an open letter to AAPL shareholders that was published by the U.S. Securities and Exchange Commission on Thursday. The letter encourages investors to vote "for" his proposal No. 10 ahead of the upcoming annual shareholders' meeting.

"The S&P 500's price to earnings multiple is 71% higher than Apple's, and if Apple were simply valued at the same multiple, its share price would be $840, which is 52% higher than its current price," Icahn wrote. "This is a dramatic valuation disconnect that simply makes no sense to us, and it seems that the company agrees with us on this point."

The activist investor, who has a reputation for using his considerable sway with publicly traded companies, revealed his position in AAPL was over $3 billion on Wednesday. He also teased the upcoming release of the letter to shareholders, and has repeatedly said he believes Apple's board is doing a "disservice" to them by not investing more.

During fiscal 2013, Apple spent $23 billion of an expanded $60-billion share repurchase authorization, which contributed to combined dividend payments and repurchases totaling over $43 billion since the program was initiated some six quarters ago.

Icahn believes Apple should spend the entirety of the $150 billion it has on its own shares, but made a more moderate proposal to shareholders, asking that Apple invest $50 billion immediately. Apple has advised that shareholders vote against the proposal, saying that its board is already "thoughtfully considering options for returning additional cash to shareholders."

Icahn's full 7-page letter is included below:

CARL C. ICAHN767 Fifth Avenue, 47th Floor

New York, New York 10153

January 23, 2014

Dear Fellow Apple Shareholders,

Over the course of my long career as an investor and as Chairman of Icahn Enterprises, our best performing investments result from opportunities that we like to call "no brainers." Recent examples of such "no brainers" have been our investments in Netflix, Hain Celestial, Chesapeake, Forest Labs and Herbalife, just to name a few. In our opinion, a great example of a "no brainer" in today's market is Apple. The S&P 500's price to earnings multiple is 71% higher than Apple's, and if Apple were simply valued at the same multiple, its share price would be $840, which is 52% higher than its current price.1 This is a dramatic valuation disconnect that simply makes no sense to us, and it seems that the company agrees with us on this point. Tim Cook himself has expressed on more than one occasion that Apple is undervalued, and as the company states, it already has in place "the largest share repurchase authorization in history." We believe, however, that this share repurchase authorization can and should be even larger, and effectuating that for the benefit of all of the company's shareholders is the sole intention of our proposal. The company has recommended voting against our proposal for various reasons. It seems to us that the basis of its argument against our proposal is that the company believes, because of the "dynamic competitive landscape" and because its "rapid pace of innovation require[s] unprecedented investment, flexibility and access to resources", it does not currently have enough excess liquidity to increase the size of its repurchase program. Assuming this indeed is the basis for the company's argument, we find its position overly conservative (almost to the point of being irrational), when we consider that the company had $130 billion of net cash as of September 28, 2013 and that consensus earnings are expected to be almost $40 billion next year. Given this massive net cash position and robust earnings generation, Apple is perhaps the most overcapitalized company in corporate history, from our perspective. Regardless of what liquidity it may require with respect to "unprecedented investment, flexibility and access to resources" for innovation moving forward, we believe the unprecedented degree to which the company is currently overcapitalized would overcompensate for any such investments (including possible investments in strategic M&A, to which the company does not refer). Said another way, we believe that the combination of the company's unprecedentedly enormous net cash balance, robust annual earnings, and tremendous borrowing capacity provide more than enough excess liquidity to afford both the use of cash for any necessary ongoing business-related investments in addition to the cash used for the increased share repurchases proposed.

It is our belief that it is the responsibility of the Board, on behalf of the company's shareholders, to take advantage of such a large and unmistakable opportunity. Indeed, we believe that by choosing not to increase the size of the repurchase program, the directors are actually performing a great disservice to the owners, especially smaller shareholders who may not be in a position to buy more stock themselves. Meanwhile, we are in a position to continue buying shares in the market at today's price, so perhaps we should thank the Board for not being more aggressive, and thus allowing us to accumulate an even larger investment position at a price that reflects the aforementioned valuation disconnect. In fact, over the past two weeks we purchased $1 billion more in Apple shares, $500 million of which we purchased today, bringing our total ownership position in Apple to a current value of approximately $3.6 billion.

Given the degree to which Apple appears undervalued to us, we almost feel that it's a waste of time to debate the point. As we believe it to be the preeminent and most innovative consumer products company in the world, with the greatest brand, hardware, software, and services in the world, Apple has had tremendous growth to date, and we fail to see why this growth would not continue moving forward. The industry (smartphones and tablets) is expected to grow volume at a 15% compounded annual growth rate from 2013 through 2017 according to IDC. We believe Apple should continue to benefit from this secular growth, as last year, 85% of Apple's revenues came from smartphones, tablets, and related software, services, and accessories. The naysayers question whether Apple will be able to participate in this growth without sacrificing pricing and gross margins, especially with competition from Google, Samsung, Microsoft, Amazon and Chinese manufacturers. Our response to them is that the answer is already evident to us from the continuing loyalty of Apple's growing customer base. The highly successful evolutionary (not revolutionary) introductions of the iPhone 5s and 5c and Ipad Air and Mini, prove to us that Apple could, for the most part, maintain pricing and gross margin as we believe consumers are willing to pay a reasonable premium for the world's best smartphones and tablets. The rumored future introduction of product line extensions with larger screens for both the iPhone and iPad would further support this view.2 In fact, a recent study from NDC shows that the iPhone accounted for 42% of smartphone users in the United States at the end of 2013, up a staggering 20% from the prior year. Despite its great scale and narrow focus, Apple has an operating margin of just 28.5%. We believe its customers' willingness to pay a premium price for the world's greatest products should enable Apple to participate in the expected volume growth of these categories while at the same time largely maintaining its average selling prices and gross margins. And, as software and services improve and become even more important to consumers in the future, we expect customer loyalty to strengthen further.

Even if the story ended with Apple's existing product and software lines, we would still choose to make Apple our largest investment. But there is more to the story! Tim Cook keeps saying that he expects to introduce "new products in new categories" and yet very few people seem to be listening. We're not aware of a single Wall Street analyst who includes "new products in new categories" or new services in any of their financial projections, even though Apple clearly has an impressive track record of such new category product introductions, even if it does so rarely. Apple released the iPhone in 2007 and the iPad five years later in 2012, both so extraordinarily successful that today they represent the majority of the company's revenue. Tim Cook's comments, along with advancements in enabling technologies, lead us to believe that we may see in the not too distant future what new groundbreaking products they've been working on developing in Cupertino these last several years.3

To get a sense of the scale of the opportunity that stems from new products in new categories, let's take a moment to consider the possibility of an Apple television. The major electronics companies are now focused on ultra high definition TVs as their next big opportunity. Ultra high definition is expected to offer a level of image clarity that is superior to today's high definition televisions for screen sizes 55 inches and above. To date, the barrier to mass market adoption of ultra high definition has been the price gap between it and regular high definition, but that price gap is closing and will soon be de minimis. The closing of this price gap is supported by statements made by the Co-CEO of Samsung Electronics, who expects the price gap to fall to 10% by the end of this year. While cable companies will likely be slow to upgrade their linear TV infrastructure due to cost, video content is expected to be accessible through the internet via services like Netflix and others. We believe ultra high definition represents a major catalyst for the next TV replacement cycle and a promising moment for Apple to introduce its first new product in this category. Reed Hastings, CEO of Netflix, has referenced ultra high definition as a major catalyst for Netflix going forward. While this is true for Netflix, we believe it is also true for Apple, not just for its hardware but also for selling ultra high definition movies and shows on iTunes through the internet. With 238 million TVs sold globally in 2012, it would not surprise us if Apple could sell 25 million new Apple ultra high definition televisions at $1,600 per unit, especially when considering both its track record of introducing best in class products and its market share in smartphones and tablets.4 At a gross margin of 37.7%, which would be consistent with that of the overall company, such a debut would add $40 billion of revenues and $15 billion to operating income annually.5

The possibility of a television represents only one opportunity for the company that stems from new products in new categories. While we won't go through all of them here, we see several major opportunities in hardware alone. With advancements in miniaturization and continued improvements in Siri, it seems obvious to us that Apple has a compelling opportunity in the exciting area of wearable devices, supported by rumors that Apple is developing a smartwatch (as Tim Cook himself said the wrist is "an area of great interest for Apple"). While many consider Apple a hardware company, to pigeonhole it as such is no longer appropriate in our opinion. Apple has built an ecosystem of hardware, software, and services that we believe collectively represents the most successful consumer product platform in the entire history of consumer-facing technologies. And as Apple's customer base continues to enjoy the use of this ecosystem, storing media in the cloud and moving it from one Apple device to another as doing so becomes increasingly convenient with innovations such as Airplay (as just one simple example of this ecosystem's current functionality), we believe that customer base grows increasingly loyal and excited for the next Apple product release, making it an asset in and of itself that grows and becomes increasingly valuable. Indeed, we believe any new software service that offers new functionality to this customer base becomes a large opportunity for Apple to introduce as a revolutionary and disruptive bolt-on to the ecosystem. As just one of many possible examples of this phenomenon, Apple could introduce a next generation payments solution. In terms of whether the marketplace is well addressed by mobile payments solutions, Tim Cook has said "I think it is in its infancy... I think it is just getting started and just of out of the starting block." With the fingerprint sensor, iBeacon, 575+ million credit card numbers stored in iTunes, and Apple's homogeneous iOS installed base with 79% of devices using iOS 7, we believe a revolutionary payments solution is now a very real opportunity that the company could choose to pursue. With respect to all of Apple's new and existing opportunities for growth, they will only prove to be successful with strong execution from the company's management, in whom we hold great confidence. Naysayers say Tim Cook is not Steve Jobs, and they're absolutely right. He is Tim Cook and we believe he is doing an excellent job, and Jonathan Ive, Senior VP of Design, is Jonathan Ive and we believe he's doing an excellent job, etcetera.

In this letter, we have above summarized why we believe Apple is undervalued in order to express how ridiculous it seems to us for Apple to horde so much cash rather than repurchase stock (and thereby use that cash to make a larger investment in itself for the benefit of all of the company's shareholders). In its statement in opposition to our proposal, the company claims that "the Board and management team have demonstrated a strong commitment to returning capital to shareholders" and we believe that is true, but we also believe that commitment is not strong enough given the unique degree to which the company is both undervalued and overcapitalized. Furthermore, it is important to note that a share repurchase is not simply an act of "returning capital to shareholders" since it is also the company effectively making an investment in itself. To us, as long term investors, this is an important difference: a dividend is a pure return of capital while a share repurchase is the company making an investment in itself by buying shares in the market at the current price, which we believe to be undervalued, from shareholders willing to sell at that price for the benefit of shareholders who choose to remain investors for the longer term. And we are long term investors. It should be noted that no one on the Board seems to be an expert in the world of investment management. However, based on our record, we believe few will argue that we are experts in this area, and we have no doubts that the Board is doing a great disservice to its shareholders by not immediately increasing the size of the share repurchase program in order to more effectively take advantage of what we believe to be the company's low market valuation.

We have expressed above what we believe to be the company's primary reason for not supporting our proposal. Conversely, it is our belief that Apple's current excess liquidity is without historical precedent and beyond reasonable comparison to its peers or otherwise, and such dramatic overcapitalization affords the company enough excess liquidity to repurchase the amount of shares we proposed. Apple's existing capital return program has just $37 billion remaining, and the company has until the end of 2015 to complete it. Without any changes to the program, the largest pile of corporate cash in the world is likely to grow even larger, and if the share price rises, this Board will have missed a great opportunity to use more of that hoarded cash to repurchase shares at an attractive value. While it is important for the Board to focus on the return of capital on a sustained basis, it is also important for the Board to evaluate whether or not its share price is undervalued and to take advantage of it with share repurchases, especially when the balance sheet exhibits dramatic excess liquidity, as we believe Apple's does today.

The Board may argue that with so much opportunity, it would be prudent to maintain its excess liquidity to increase R&D or make acquisitions, especially when considering the financial strength of its competitors. We completely agree that the company must innovate and should be flexible to make prudent strategic acquisitions, yet even after taking such factors into account, we believe that tremendous excess liquidity remains. With respect to possible M&A (to which the company does not refer in its statement), for the opportunities highlighted above (a TV, a watch, a payment service), we find it extremely difficult to identify any possible strategic acquisitions of scale that make sense. Furthermore, such action would seem to conflict with Apple's culture historically. A remarkable fact is that since the Board reacquired Steve Jobs through the NeXT acquisition for $427 million in 1997, the next largest acquisition Apple made was $2.6 billion for Nortel's patent portfolio. Amazingly, over these 17 years, Apple made just $7.8 billion worth of acquisitions in total during this timeframe. Apple clearly has a long history and culture of developing its innovation internally, which leads us to believe that the company will not seek out large acquisitions to pursue any of the opportunities about which we have speculated. In terms of paying for the necessary innovation internally, Apple is expected to generate $40 billion of earnings next year, which already takes into account an increasing R&D expense. In order to address the argument that Apple should reserve excess liquidity to more effectively compete with some of its deep-pocketed competitors, there is no doubt that some of them also have significant earnings and net cash on their balance sheets (whether or not that is appropriate). But Apple has much more. When compared to its next largest competitor, Microsoft, for example, Apple has $68 billion more net cash and is expected to generate $18 billion more in earnings during 2014.

The Board may argue that much of its cash and earnings are international and therefore subject to a repatriation tax if returned to the United States to repurchase shares. While this is true, we question why the company would not simply borrow the money in the Unites States to the extent it deems its domestic cash of $36 billion and domestic earnings are insufficient. Given that the company has $130 billion of net cash and $40 billion of expected annual earnings, and the fact that it is hard to find a better time in history to borrow money, a $50 billion share repurchase over the course of fiscal year 2014 seems more than reasonable to us. Today, Apple's outstanding ten year bonds yield 3.63%, and its five year bonds yield 2%. Apple could either continue to carry this debt, repay it from its domestic earnings over time, or repatriate cash from abroad upon the passage of corporate tax reform.

The company has stated that it is "updating perspectives on its capital return program for 2014 and beyond" and "collecting input from a very broad base of shareholders." We believe, if our proposal receives majority shareholder support, that the Board should respect it and increase the repurchase program as requested. We believe this action will greatly enhance value for all long term shareholders who believe, as we do, in the great potential of this company. If the Board takes this action, we will applaud them for taking advantage of one of the greatest examples of a "no brainer" we have seen in five decades of successful investing.

Sincerely yours,

Carl C. Icahn

For more information on this and other topics, follow me on Twitter at: @Carl_C_Icahn

https://twitter.com/Carl_C_Icahn

-m.jpg)

Wesley Hilliard

Wesley Hilliard

Christine McKee

Christine McKee

Marko Zivkovic

Marko Zivkovic

Malcolm Owen

Malcolm Owen

William Gallagher

William Gallagher

Andrew O'Hara

Andrew O'Hara

92 Comments

Sell off, Icahndy corn. Go invest in a brokerage firm or something.

I am just going to keep saying this, if he does not believe in what apple is doing go put your money elsewhere. I do not understand why someone would put their money into an investment which they obvious thinks is not doing the right things, he asking to loose his money.

However, he started to put money in when it was in the low $400's so he is already made a couple of $100M on apple alone in the past year. and now of his whining has helped it increase, but he probably believes otherwise.

what's the matter carl, 3.5 billion not enough to start your own competitor company and run it the way *you* want to run it?

[quote name="Maestro64" url="/t/161727/carl-icahn-invests-another-500m-in-apple-promotes-increased-buyback-in-letter-to-shareholders#post_2461817"]I am just going to keep saying this, if he does not believe in what apple is doing go put your money elsewhere. I do not understand why someone would put their money into an investment which they obvious thinks is not doing the right things, he asking to loose his money. However, he started to put money in when it was in the low $400's so he is already made a couple of $100M on apple alone in the past year. and now of his whining has helped it increase, but he probably believes otherwise. [/quote] his goal is to make money, regardless of whether a better company comes out of it or not. he is investing huge sums so as to influence the stock price in his favor so that he can achieve his goal.

what's the matter carl, 3.5 billion not enough to start your own competitor company and run it the way *you* want to run it?

he is not smart enough to come up with an original idea, he rather financial engineer a company to look good so he can make a profits and when he pulls his money out everyone else is left hold the shell.