It's been nearly five years since the introduction of the Apple Card, and cardholders are taking advantage of everything it offers.

In partnership with Goldman Sachs, Apple launched the Apple Card in 2019. Since then, it's been a notable, if not somewhat controversial, hit.

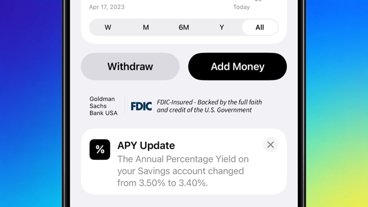

In 2023 alone, users earned over $1 billion in Daily Cash from using Apple Card. Cardholders also took advantage of the new savings account feature that was launched in April 2023. According to Apple, users reached over $10 billion in deposits "in just a few short months."

Additionally, most Apple Card cardholders auto-deposit their Daily Cash into savings, with two-thirds adding additional funds from linked bank accounts. Currently, the Apple Card offers an APY of 4.5%

"We designed Apple Card with users' financial health in mind, and it's rewarding to see our more than 12 million customers using its features to make healthier financial decisions," Jennifer Bailey, Apple's vice president of Apple Pay and Apple Wallet said in a press release.

"We're proud of what we've been able to deliver to Apple Card customers in just five years. As we look at the year ahead and beyond, we're excited to continue to innovate and invest in Apple Card's award-winning experience, and provide users with more tools and features that help them lead healthier financial lives."

Of its 12 million users, Apple says that nearly 30 percent make two or more payments per month, which helps to avoid racking up interest when making large payments.

Apple also shared that more than a million Apple Card users have shared their Apple Card with their Family Sharing Group. It also says that "600,000 users are building credit equally with their spouses, partners, or another trusted adult on Apple Card."