Daniel Eran Dilger

Daniel Eran Dilger

Apple's final quarter of 2014 is expected to set dramatic new records in iPhone sales and overall profits, but external issues out of the company's control will also play a part, ranging from cheaper oil to declining foreign currencies.

Cheap oil makes shipping less expensive

Record U.S. production of domestic oil— largely from new shale oil fracking extraction techniques— has incrementally pushed energy prices downward over the last two years.

More recently however, OPEC oil nations have overwhelmed global demand for oil with continued production in an effort to push crude prices dramatically downward— an apparent attempt to make U.S. production costs prohibitive and reduce new investment in fracking, allowing the oil cartel to win back market share.

The end result has been an abrupt drop in fuel prices. That directly benefits Apple, because it significantly reduces the cost of shipping components and finished goods.

Apart from shipping costs, Apple's own cost savings from cheap oil are tempered somewhat by the company's aggressive efforts to move away from oil to renewable energy sources, including the solar, hydroelectric and biomass fuel cell energy facilities it has built to power its vast data centers in the U.S.

Apple's Maiden, N.C. solar farm. | Source: AppleCheap oil gives consumers more money to spend

Low prices at the pump also give consumers extra cash to spend elsewhere. That's particularly fortuitous for Apple given that it has set up a holiday product lineup with a variety of premium options.

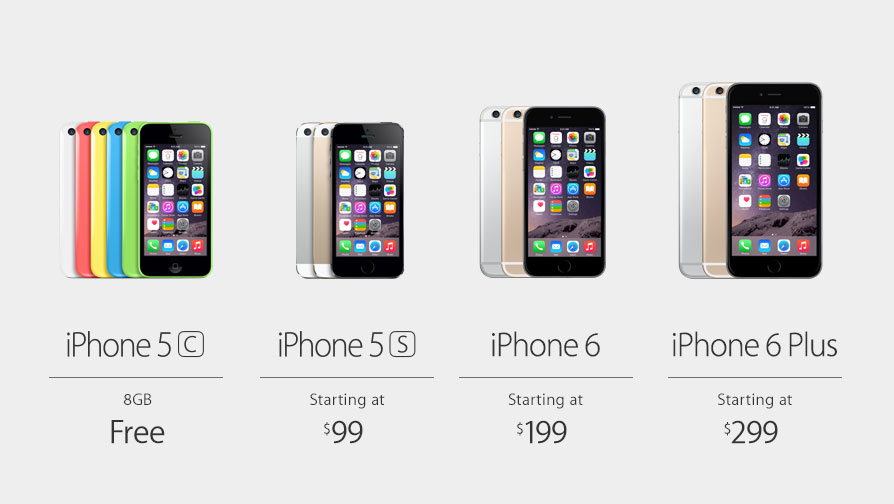

Among iPhones, Apple is now offering its most expensive phone ever: iPhone 6 Plus, at a $100 premium for its super sized screen.

Additionally, iPods— once Apple's primary holiday favorite— have scaled back to make way for a broad array of iPads targeting base model price points starting from $249 to $499.

Despite bearing a premium price among a sea of Android tablets that commonly target the low end, Apple's newest iPad Air 2 is broadly perceived to the most desirable tablet, even being picked out by Android Police as the tablet to buy in its latest holiday gift guide.

Weak competition for winter

Apple is not only well positioned to boost its Average Selling Prices and unit sales during the cheap oil holidays, but also faces some of the weakest competition ever exerted by rival vendors in smartphones, tablets and PCs.

Samsung, the company's primary smartphone rival, has blown both of its primary 2014 flagship launches with introductions of unexceptional products built using cheaper materials. Dinged by poor reviews and inventory it can't move, Samsung's September quarter chalked up an incredible 73.9 percent decline in phone profits as its premium sales volumes collapsed in the third quarter.

Once strongly differentiated by large screen sizes, Samsung's latest Galaxy S5 and Note 3 have been bludgeoned by the release of iPhone 6 models sporting not only larger displays but also functional Touch ID for fingerprint login, the broadly-promoted new Apple Pay, fast graphics and 64-bit processing, on top of Apple's use of premium materials.

Outside of Samsung, no other smartphone maker approaches Apple's smartphone sales in the West, even as iPhones have dominated the charts in Japan and taken the lion's share of premium phone sales in China. That's given Apple the majority of the global profits earned from selling phones, a position it also enjoys among tablets and PCs.

Google has abandoned its own "Silver" initiative to drive more premium Android devices, and is running into continued production issues with its Nexus line built in collaboration with troubled vendors including HTC, LG and Motorola.

BlackBerry and Microsoft's Windows Phone are barely even registering as also-rans this holiday season, funneling consumers directly to Apple Stores. Other retailers are continuing to leverage the popularity of Apple's products to drive traffic in their stores via incessantly promoted discounts.

Stronger dollars could affect Apple's perfect sales-storm

The significant strengthening of the U.S. dollar against a range of other currencies including the Euro and Japanese Yen could enable Apple to make corporate overseas investments at a discount.

The company is indeed expanding, with new offices in the UK and Japan, and dramatic plans for retail expansion, particularly in China where 20 new stores are planned.

However, a larger problem is that Apple will lose some profits from foreign sales when those revenues are converted back into dollars for financial reporting purposes. In fiscal 2014, international sales made up 62 percent of Apple's total revenues.

Apple has previously warned of "foreign currency headwinds," noting in its SEC filings that while it maintains hedges as insurance against extreme currency fluctuations, sustained strengthening of the dollar will eventually result in either the need to raise overseas pricing or force Apple to eat the difference.

Specifically, the company's Annual 10K warned that "weakening of foreign currencies relative to the U.S. dollar adversely affects the U.S. dollar value of the Company's foreign currency-denominated sales and earnings, and generally leads the Company to raise international pricing, potentially reducing demand for the Company's products.

"Margins on sales of the Company's products in foreign countries and on sales of products that include components obtained from foreign suppliers, could be materially adversely affected by foreign currency exchange rate fluctuations. In some circumstances, for competitive or other reasons, the Company may decide not to raise local prices to fully offset the dollar's strengthening, or at all, which would adversely affect the U.S. dollar value of the Company's foreign currency denominated sales and earnings."

Apple also noted that it "uses derivative instruments, such as foreign currency forward and option contracts, to hedge certain exposures to fluctuations in foreign currency exchange rates. The use of such hedging activities may not offset any, or more than a portion, of the adverse financial effects of unfavorable movements in foreign exchange rates over the limited time the hedges are in place."

-m.jpg)

Christine McKee

Christine McKee

William Gallagher

William Gallagher

Amber Neely

Amber Neely

Andrew O'Hara

Andrew O'Hara

Sponsored Content

Sponsored Content

Charles Martin

Charles Martin

63 Comments

It's difficult to see past the nonsense that is cited by Wall Streeters as the cause of markets or stocks rising and falling. Frankly, I doubt they really know themselves. It's cyclicality within cyclicality.

[quote name="AppleInsider" url="/t/183894/apple-incs-blockbuster-winter-quarter-boosted-by-cheap-oil-dinged-by-strong-dollar#post_2651449"]The end result has been an abrupt drop in fuel prices. That directly benefits Apple, because it significantly reduces the cost of shipping components and finished goods.[/quote] Is that confirmed? If Apple has fixed contracts in place for transport they are longer than this current drop in fuel prices it could be their transportation clients that are reaping the profits, not Apple. [QUOTE]Apart from shipping costs, Apple's own cost savings from cheap oil are tempered somewhat by the company's aggressive efforts to move away from oil to renewable energy sources, including the solar, hydroelectric and biomass fuel cell energy facilities it has built to power its vast data centers in the U.S.[/QUOTE] Wouldn't that be mostly fixed QoQ, which means that companies that pay for fossil fuels are more likely to see a bigger benefit from this cheap oil?

So Apple is now going bankrupt???

/s

(how long will it take before someone jumps on this comment???)

[quote name="SpamSandwich" url="/t/183894/apples-blockbuster-winter-quarter-boosted-by-cheap-oil-dinged-by-strong-dollar#post_2651450"]It's difficult to see past the nonsense that is cited by Wall Streeters as the cause of markets or stocks rising and falling. Frankly, I doubt they really know themselves. It's cyclicality within cyclicality. [/quote] I don't see anything nonsensical about this. It's a very good article, especially on the possible implications of the dollar appreciation on Apple's margins and reported earnings. With nearly two-thirds of its sales abroad, Apple's cash flows are hugely exposed to currency swings compared to even a few years ago. I have no doubt that Apple hedges aggressively, and that will hopefully mute the impact. Moreover, the fact that China had been the huge area of growth should mute the impact as well, since the U.S. Dollar has not appreciated too much against the Chinese Yuan (compared to the Euro or the Yen). I think the Japan numbers -- reported in dollars -- are going to suck this quarter. The net effect of all this could well be that, despite what may be a blockbuster quarter -- perhaps even the best ever in terms of actual volumes sold or in constant currency terms -- the stock will move sideways for a while.

I have no doubt that Apple hedges aggressively, and that will hopefully mute the impact. Moreover, the fact that China had been the huge area of growth should mute the impact as well, since the U.S. Dollar has not appreciated too much against the Chinese Yuan (compared to the Euro or the Yen). I think the Japan numbers -- reported in dollars -- are going to suck this quarter.

The net effect of all this could well be that, despite what may be a blockbuster quarter -- perhaps even the best ever in terms of actual volumes sold or in constant currency terms -- the stock will move sideways for a while.

It doesn't really matter if Apple's stock moves sideways for a while. That is out of Apple's hands. At this point I don't believe Apple can do anything to boost the share price. Looking at Apple's share price this past couple of weeks, the stock movement looks no better than any other two-bit tech stock on the market. Apple's share price seems no stronger or less volatile than any other stock. All that really matters is that Apple must be reaping huge amounts of revenue and profits while other companies aren't. Relatively speaking, Apple should be head and shoulders above nearly every other company during this holiday season but honestly it's hard to tell by looking at Apple's declining share price movement. I'm hoping while Wall Street steps on Apple's share price, Apple is buying back lots more shares to create a solid bottom to move from once the new year starts. It blows my mind to think Apple has lost close to $60 billion in market cap in just a couple of weeks and yet Apple can't sell products fast enough. $60 billion. It's crazy. That's more than Netflix and Tesla combined with $10 billion or so left over. Yet you've got people sternly claiming how Apple's iPad business is on the rocks and will be negatively impacting this quarter's estimates.

But who cares what the boo-birds say about this quarter. Apple's stores are packed (with more than just protesters) and the iPhone is selling in huge numbers. As shareholders we have to think longer term as Apple Pay grows and hopefully high sales of AppleWatch begin. I don't know where AppleTV is headed but without having control of content, selling AppleTV hardware isn't going to help much in terms of boosting Apple's revenue. I have no concerns about Apple's future for the next couple of years. Apple has enough cash to continue growing as well as any other company on the planet. As long as Apple continues increasing dividends, I'm golden.