Analysts are continuing to weigh in on the future of Apple's growth following the company's most-recent quarterly report, with Guggenheim Securities claiming the push for higher iPhone ASPs isn't enough, while Loup Ventures insists investors should shift to thinking of "Apple as a Service" rather than a traditional hardware producer.

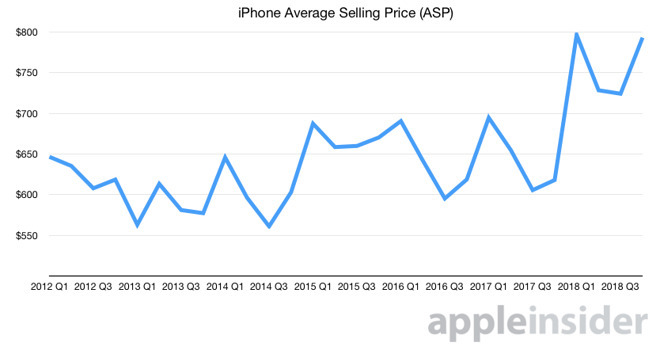

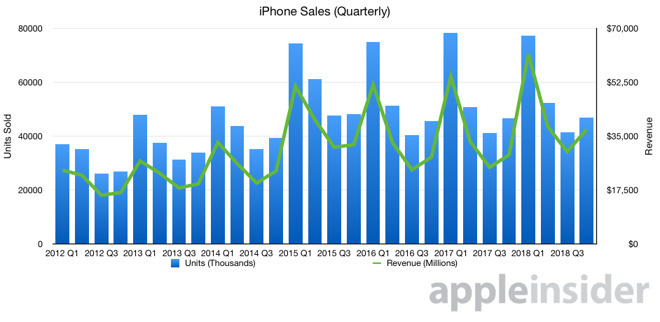

Apple's quarterly results at the start of November revealed marginal iPhone shipment growth of 46.9 million iPhones, but increased revenues of $37.2 billion for the product line due to raising the average selling price (ASP) to $793. While the ASP increase helped pad Apple's bottom line, this hasn't stopped Robert Cihra of Guggenheim from downgrading Apple from Buy to Neutral.

"Whereas a year ago AAPL looked like a table-pounder when iPhone units were weak but about to to be more than offset by a big jump in ASPs, which ultimately drove Apple's best iPhone revenue growth in three years," writes Cihra in an investor note seen by AppleInsider, continuing "we rather now find that setup flipped with 'growth via ASPs' widely known but just as those ASPs start to anniversary."

iPhone's average selling price

While noting the iPhone ASP has increased 40 percent over the past ten years, "reflecting its growing value to both consumer and business markets." Cihra points out nearly half of that growth arrived in the full year of 2018 alone, "making a period of digestion more likely."

Guggenheim's full year 2019 estimates for revenue and EPS have been cut from $281 billion and $13.41 respectively to $273 billion and $12.97, mostly due to iPhone providing nearly 60 percent of the revenue and the analyst suggesting that revenue may not grow that much next year.

Noting reports of supply chain cuts, Cihra suggests the new estimate is that Apple will sell 5 percent fewer iPhones in 2019 compared to 2018. Crucially, it is predicted that, unlike last year, the increases in ASP will not provide enough to offset the reduction in unit sales, with a forecast 3 percent year-on-year ASP rise leaving iPhone revenues down 2 percent in 2019 from the previous year.

iPhone units and revenue

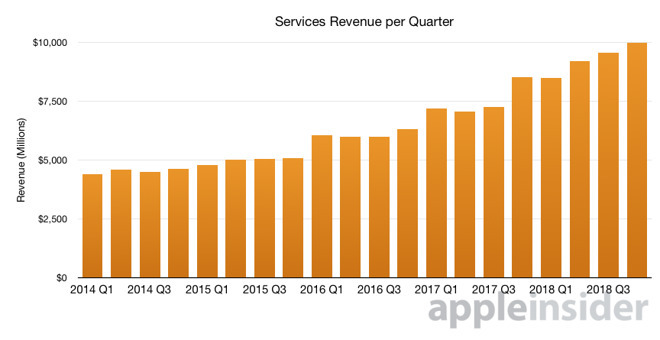

The future of Apple's Services arm is seen as a brighter spot for the future according to Cihra, who predicts revenue growth of 19 percent year-on-year for all of 2019, with the App Store providing 38 percent, Music and iTunes at 17 percent, and Licensing at 15 percent. The reliable growth will help increase its overall contribution to Apple's revenue to 16 percent from 14 percent, and gross profit from 24 percent to 28 percent.

In his own note, Loup Ventures analyst Gene Munster continues to put forward the opinion that investors should change the way they think of Apple, in what he has previously termed as "Apple as a Service." While analysts and investors continue to focus on the iPhone's unit sales, Munster believes Apple's reliance on iPhone for revenue growth will diminish, in favor of increasing its portfolio of software services.

Revenue earned by Apple's Services arm

During the results, it was announced Apple would no longer report hardware units numbers, a change that would prevent analysts from calculating the iPhone ASP, as well as from seeing how popular the iPhone is overall. Apple CFO Luca Maestri defended the move by claiming there is no correlation between unit sales and the stock price over the last three years, and that unit figures have "not been necessarily representative of the underlying strength" of the business.

In supporting this view, Munster claims data from the results can be used as evidence that this is a better way of thinking. According to his analysis, the unit growth of the iPhone, iPad, and Mac are disassociated with the revenue, earnings, and company's stock price since late 2015.

Apple's unit growth against revenue, earnings, and its stock price (via Loup Ventures)

The price dispersion within the iPhone product line has also increased over time, with the wide range of iPhones Apple currently sells for between $450 and $1,450 being a dramatic shift from just two years ago. "This is important because each unit of sale can now have a very different impact on revenue," suggests Munster.

The idea of using Google Trends to compare the interest in new iPhones to those of previous models is also challenged, with the conventional view claiming spikes in search traffic for the latest models have declined over the last four years, suggesting interest in the iPhone is softening. Referring to research from Inflection Capital that analyzed Google Trends for all iPhone models, it seems that interest is still growing for iPhones, and is spread across more models.

Munster then goes on to insist investor concerns over softening iPhone demand is an overreaction. "Interpreting data points around demand from the supply chain is a dangerous art," Munster claims. "Historically, investors and analysts (present company included) have drawn the correct conclusion as many times as the incorrect one."

As an example, the reports about Lumentum's disappointing guidance could be accounted for by Apple getting closer to rival suppliers II-VI and its recent acquisition of Finisar for future VCSEL orders.

Apple's frequent changes to components and suppliers is also said to add complexity to decoding supply chain data points.

Apple's guidance for the December quarter anticipates revenue would be 2 percent down on Street expectations. "The odds that something has materially changed between then and now is low," the analyst asserts. "things do change, but typically not that quickly. There would be real cause for concern if we continue to hear cautionary comments from suppliers into mid-December and early January."