Apple will be announcing the first-quarter results for 2025 on January 30. Here's what to expect from what should be a blockbuster financial release.

Apple's Q1 2025 financial results will be released on Thursday, January 30, a short time ahead of the analyst and investor conference call at 5p.m. Eastern.

The call will feature CEO Tim Cook explaining the financial details from the results, but he will have a new person on the call with him. Former CEO Luca Maestri bid farewell in October's earnings call, with Kevan Parekh set to take his seat in the quarterly call.

While Cook did take time to praise Maestri during his last conference call as CFO, it's more likely that Parekh's welcome will be a much quicker affair.

Last quarter: Q4 2024 details

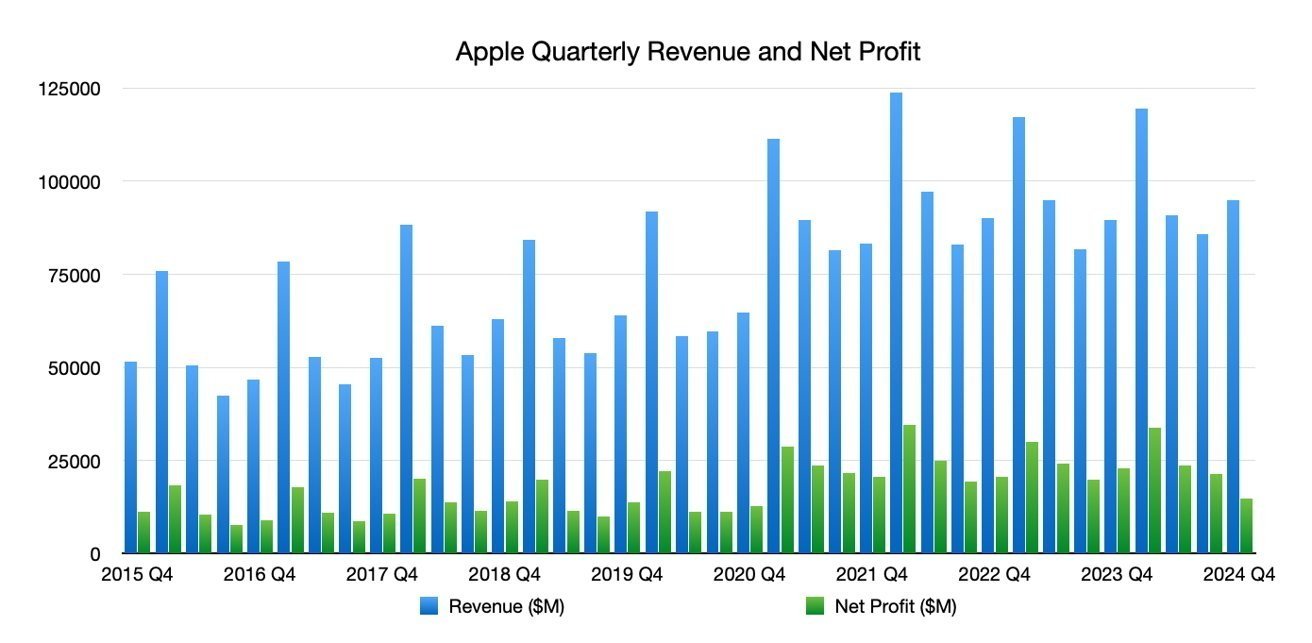

The Q4 results saw Apple haul in $94.93 billion in revenue, up from $89.5 billion one year prior. Apple also declared an earnings per share of $1.64.

Apple quarterly revenue and net profit, up to Q4 2024

iPhone revenue was up 5.5% year-on-year to $46.22 billion, with iPad up 7.9% to $6.95 billion. Mac also saw an increase, but of 1.7% at $7.74 billion, while Services continued growing with a 11.9% YoY increase to $24.7 billion.

Wearables, Home, and Accessories was the only blemish, dropping 3% year-on-year to $9.32 billion.

The period saw the launches of the iPhone 16 range, AirPods Max with USB-C, the Apple Watch Series 10, and an Apple Watch Ultra 2 in black. However, as usual, these releases will have only partly helped in Q4 2024, with them more likely to affect the Q1 2025 results instead.

Apple is a highly seasonal company, making sequential quarterly analysis not much of a guide for quarterly forecasts. What it does do is offer a glimpse of the lead into the quarter, by seeing where the previous one left off.

With Q4 2024 being about 6% better year-on-year than Q4 2023's total, this gives Q1 2025 a good starting point to build from. However a really poor holiday season could easily undo that progress.

Year-ago quarter: Q1 2024

Released in February 2024, the Q1 2024 results are the figures Q1 2025 aim to beat. The seasonality of Apple's business means that Q1 is the biggest for the company in the year.

It's the quarter that happens just after the launches of the latest iPhones, and often involves other early-in-period launches too. Then there's the holiday sales period, which can make a big impact on the quarter as well.

These factors, as well as the overall importance of Q1 in Apple's fiscal year, means the previous year's Q1 performance is a measurable yardstick to compare the newest Q1 results against.

At the time, Apple reported revenue of $119.58 billion, marginally rebounding earnings from one year prior of $117.15 billion by a mere 2%. While a positive revenue level is good for Apple, it's not really that much of an increase and could be considered close to flat growth by investors.

The EPS was set at $2.18, up from $1.88.

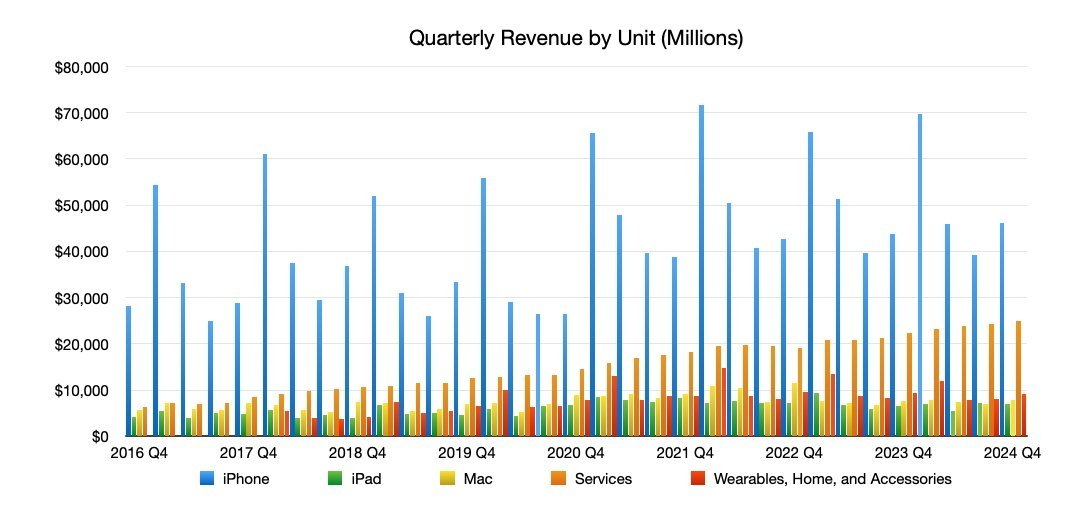

Apple quarterly revenue by unit, up to Q4 2024

Broken down, the iPhone revenue of $69.7 billion was up from the $65.78 billion of the year-ago quarter, with Mac revenue also up to $7.78 billion versus $7.74 billion in Q1 2023. iPad revenue was down, from $9.4 billion in Q1 2023 to $7.02 billion in Q1 2024.

Wearables, Home, and Accessories saw a one-year drop from $13.48 billion to $11.95 billion. Services was reliable as ever, growing from $20.77 billion to $23.12 billion.

The few billions of improvement from iPhone and Services, and to a lesser extent Mac sales, largely offset the billions in drops seen by iPad and Wearables. If the down quarters were instead flat, Apple could've effectively doubled its revenue growth in the period.

As for iPhone specifically, reports point to the iPhone 16 Pro models dominating, while non-Pro models are seemingly lackluster. This is a trend that is often seen post-launch, with the premium models getting an early advantage, but it's anyone's guess whetherthat translates into reduced or increased sales overall.

At the time, Cook reported an install base of active devices exceeding 2.2 billion. He was also upbeat about the prospect of the just-launching Apple Vision Pro. The less said about the Apple Vision Pro, the better.

What happened in Q1 2025

In terms of product launches, Apple saw a lot more in the period beyond the Q4 launches, which will have a major effect on the finances of the holiday quarter.

In October, Apple updated the iPad mini to use the A17 Pro, followed by updating the Magic Mouse 2, Magic Trackpad 2, Magic Keyboard, and Magic Keyboard with Touch ID.

Apple's revamped M4 Mac mini

Apple used November to finally upgrade the Mac range to the M4 level of Apple Silicon. The biggest change was the revamp of the Mac mini, which uses a much smaller design and new port placements, and saw a warm reception from critics.

Other Mac launches that month include the 24-inch iMac and updates to M4 for the MacBook Pro.

While the Q1 releases won't necessarily have as much of an impact on the quarter due to being introduced during the period, it's likely that they will still have some effect due to the holiday sales period.

The key element to look out for is iPhone sales, as that continues to be the biggest factor in how the quarter goes for the company. With the continued slow rollout of Apple Intelligence, it could be that Apple's software push could be a big factor in generating sales, if it can continue its development and expansion at pace.

The shift to M4 chips in the core Mac and MacBook lines will probably bring in more sales too, especially for the Mac mini's radical redesign. But it's doubtful that Mac will make as much of a dent as a small iPhone revenue change.

Wall Street Consensus

The Wall Street consensus refers to a survey of analysts. The results are averaged out to give a general opinion of where investors and analysts are leaning in their quarterly forecasts.

Yahoo Finance

In the estimates published by Yahoo Finance as of January 28, 29 analysts offered an average revenue estimate of $124.04 billion. The estimate's range goes from a high of $129.89 billion to a low of $119.56 billion.

For the earnings per share, a group of 25 forecasts an average of $2.34, with a high of $2.50 and a low of $2.19.

TipRanks

On January 28, TipRanks offered its own consensus figures. The revenue forecast is at $124.25 billion, with a range from $119.56 billion to $129.89 billion.

The earnings per share is expected to be $2.35, with a range from $2.19 to $2.50.

Zacks

The Zacks consensus estimate on January 27 puts first-quarter revenue at $124.04 billion, representing 3.73% growth year-on-year and matching the Yahoo Finance consensus.

When it comes to the earnings per share, the consensus believes it will be $2.36, and has done for the last 30 days. This is an 8.26% increase on Q1 2024's figure.

On a per-category basis, it is forecast for iPhone sales to decline 0.7% to $69.189 billion, and for Services to grow 13.2% year-on-year to $26.176 billion.

Post Q4 hot takes

Following the Q4 2024 results, analysts offered their hot takes on the period. However, they were more interested in the Q1 2025 results.

The sentiment was of cautious optimism.

Morgan Stanley said its Q1 outlook is "mixed" with lighter revenue than buying expectations, but with a better gross margin than the consensus view. Evercore ISI pointed to single-digit growth in Q1 and a more staggered iPhone cycle.

In analysis from January 3, The Motley Fool writes that Apple is still an impressive stock pick, thanks to its high revenue versus its peers. However, growth has been seen to be slower, at 2% versus 10% or more for Alphabet or Microsoft.

With mixed results across its product categories, Services is seen as a continual bright spot. Its free cash flow is still staggering, and still growing, with Apple also prioritizing a return in capital to shareholders.

Forbes offered on November 21 its prediction for Apple in 2025, the iPhone continues to be a centerpiece of the business, but China is a challenge for both production and sales. Services segment revenue will be a driver for the company, and it's key for the future as it's poised to become "a second juggernaut business line" that can make up for hardware segment cycles.

The report finds that Apple's challenge in 2025 won't be in producing massive revenue, but more needing to justify its valuation to investors.

Analyst Expectations

As time draws near to the results, analysts are keen to put forward their forecasts and predictions for the quarter.

Morgan Stanley

In Morgan Stanley's January 23 preview, it offers expectations of the Q1 quarter being in-line, with $124GB of revenue being up 3.5% year-on-year, and an EPS of $2.31.

Stable iPhone builds in the quarter helps raise the shipment forecast just half a million to 76.5 million units, up 3% year-on-year. However, average selling prices forecasted to be less favorable than anticipated led to an iPhone revenue forecast of $69.1 billion, down 1% year-on-year.

Incremental currency headwinds have also forced a lowering of iPad and Mac ASPs by 1.5%, though stronger Mac demand offsets this a bit. Meanwhile Services revenue is forecast to grow by 13.5% year-on-year, thanks to App Store outperformance.

However, the report says that a Q2 guide-down is "well-telegraphed at this point." Current Q2 estimates include $92.6 billion of revenue and more cautious iPhone revenue as well.

Morgan Stanley rates Apple as "Overweight" with a price target of $273.

Wedbush

In its January 22 estimate, Wedbush insists the "panic and bear frenzy around Apple is way overdone." While recent China iPhone checks are mixed to perceived softer unit declines, it's still "manageable" with stronger US and rest-of-world growth.

On the revenue side, Wedbush thinks Apple will get $124.8 billion in the quarter, with an EPS of $2.43.

Services should be strong, with it being a "linchpin to the $4.5 trillion sum of the parts valuation we see over the next 12-to-18 months," the analysts write. The slow rollout of Apple Intelligence in a phased strategy is the start of a "massive growth renaissance at Apple," with about 20% of the world's population expected to access AI through an Apple device in the coming years.

What bears are missing, Wedbush muses, is Apple's massive install base of 1.5 billion iPhones and 2.3 billion iOS devices, which should create "a new AI driven growth story" Wall Street is failing to consider.

"We have been here many times on Apple's stock over the last decade with the noise/bears piling on," the note concludes. "But that creates the opportunity to own this tech stalwart poised to enter its next phase of growth in 2025 in our view."

Wedbush rates Apple as "Outperform" with a price target of $325.

Loop Capital

On January 21, Loop Capital downgraded Apple from "Buy" to "Hold," revising the price target down from $275 to $230. Supply chain research seemingly indicated a material reduction in demand for the iPhone in the March quarter, which could amplify in subsequent quarters.

JP Morgan

J.P. Morgan analysts kept Apple on an "overweight" call on January 21, but a wariness of Apple's outlook prompted a small downgrade of the price target from $265 to $260.

Analysts cited a strong dollar and "flattish unit sales," when considering the current state of AI features on the market.

Weak demand in China was also an issue, with expectations that Apple will continue losing market share as it's "past its product cycle peak." There's also the problem of iPhones failing to benefit from local government subsidies, as they target low and mid-tier phones, not premium iPhones.

Goldman Sachs

On January 23, Goldman Sachs tweaked the price target for Apple's shares. The shares retain a "Buy" rating, but the target shrank from $286 to $280.

Goldman Sachs also said it expected Q1 revenue of $124.2 billion, along with an earnings per share of $2.35.

The iPhone revenue will grow by 1%, with a 4% shipment decline offset by 5% year-on-year sales price growth. There is also encouraging signs of potential growth for the 2026 fiscal year, thanks to the continued rollout of Apple Intelligence in new markets, such as China.

Evercore

On January 17, Evercore ISI reiterated its "Outperform" rating for Apple and a $250 price target. However, that "Outperform" was deemed a "Tactical Outperform."

The reasoning for the specific "tactical" tag is because Evercore reckons Apple is a well-positioned company overall, but with low expectations. It has the potential for an in-line quarter, thanks to growth in emerging markets and strong performances in the Services and Wearables areas.

Despite discounts on iPhones in China, overall demand is expected to remain steady. The September quarter flat growth in China was seen as a positive, with Apple able to maintain its position in the face of increased competition from Huawei.