Citing a trio of trends it expects to power Apple through the ongoing COVID crisis, investment bank JP Morgan on Monday recommended that investors use any post-earnings recalibration of the company's share price to make incremental adds to their existing positions.

In a note to investors seen by AppleInsider, JP Morgan analyst Amik Chatterjee said that the investment bank is maintaining a "strong long-term outlook" on Apple despite the possibility of weak second-quarter results and lack of guidance for the third quarter. Apple will report earnings for Q2 2020 on Thursday, April 30.

Chatterjee believes there's a high likelihood that Apple will side-step its usual practice of issuing guidance for the June quarter. Combined with the fact that current buy-side expectations of 25 to 28 million iPhones sold in this quarter could be ratcheted down, there's a chance of underperformance in the shares.

Chatterjee says that there's a current precedent among technology companies to not guide for the June quarter, and that Apple's move in this area should come as no surprise to investors. Beyond that, the analyst remains upbeat about Apple's long-term outlook and the company's ability to recover from the current coronavirus pandemic. In fact, JP Morgan is recommending that investors use the potential fallout from weak Q2 2020 results to make incremental adds.

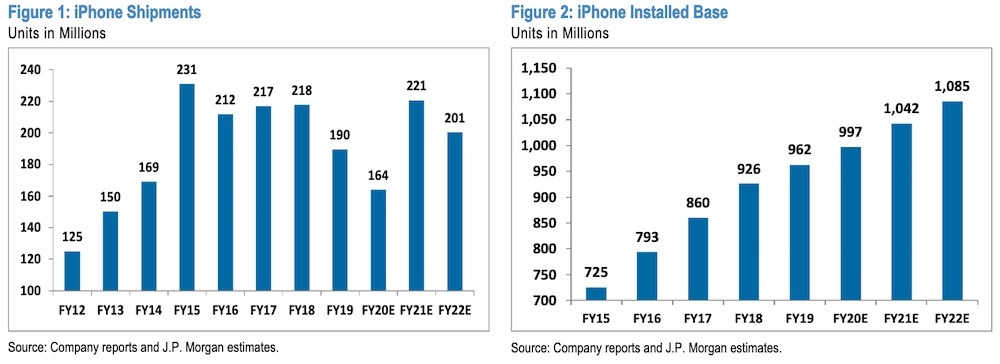

Credit: JP Morgan

Despite growing concerns about COVID-19, Chatterjee said that Apple is currently outperforming the S&P 500 year-over-year and that the company is well-positioned for a strong recovery in the fall and through 2021.

That outlook is largely lead by three factors. For one, Apple retains high-quality earnings, cash flow and balance sheet, and the company's Services transformation is still an upside. A rumored 5G iPhone is likely to drive a strong volume cycle through 2021.

Chatterjee said that Apple is "relatively better positioned" to outperform in the long-term with the recovery of discretionary consumer spending. While investors still question the possibility of weak consumer spending recovery, JP Morgan pointed to a "much broader portfolio in terms of price points" and Apple's ability to leverage on the supply chain to drive prices lower.

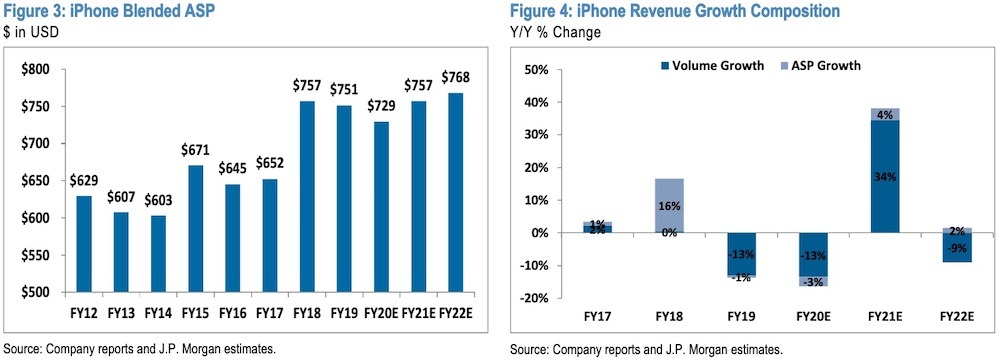

Credit: JP Morgan

Other factors, such as growth in installed user base, leadership in the technology industry, and optionality around capital deployment, "together lead us to expect double-digit earnings growth and a modest re-rating for the shares," Chatterjee wrote.

At Apple's earnings call Thursday, JP Morgan is forecasting total revenues of $52.1 billion, a bit lower than the consensus expectation of $54.3 billion, and a gross margin of 38.4%. That includes revenue estimates of $23.9 billion for iPhone, $4.1 billion for iPad, $4.6 billion for Mac, Services $13.6 billion for Services, and $5.8 billion for Wearables, Home and Accessories.

The investment bank also estimates Apple's total revenue to be $36.2 billion for the June quarter, down from a consensus of $51.5 billion.

JP Morgan is maintaining its $335 December 2020 price target, which is based on an FY2021 earnings-per-share estimate of $16.75 and a blended price-to-earnings ratio of 20.0x. That ratio is based on multiples of 16x for iPhone, 11x on Mac and iPad, 25x on Services, 20x on Apple Watch and AirPods and 11x for Other Products.

Shares of Apple are currently trading at $283.14, up 0.06% on the NASDAQ as of publication time.