Bank of America Securities analyst Wamsi Mohan has downgraded Apple's stock to a "neutral," citing a new balance to risk and reward as the stock has hit new highs following a blockbuster earnings report.

After hiking a target price for Apple stock to $420 after the earnings report, Wamsi Mohan at Bank of America Securities has again revised his expectations for the stock. In a note to investors seen by AppleInsider, Mohan is now no longer underwater at $470 per share, but has reclassified the stock as neutral versus buy, since he sees the stock as more balanced than it has been previously.

Mohan's new $470 Apple stock price target assumes single-digit year over year revenue grown, and flat margins from hardware for the fall, including the "iPhone 12." Like other analysts, Mohan believes that there will be "high-teens" year over year growth in services, and an increase in services margins.

To support a $17 earnings per share, Mohan believes that $6 of that will come from Services with a 40x earnings per share multiple, with the remaining $11 being delivered from hardware at a 20x earnings per share.

Mohan justifies the multiple on Apple's large cash balance and "opportunity to diversify into new end markets, increasing mix and diversity of services."

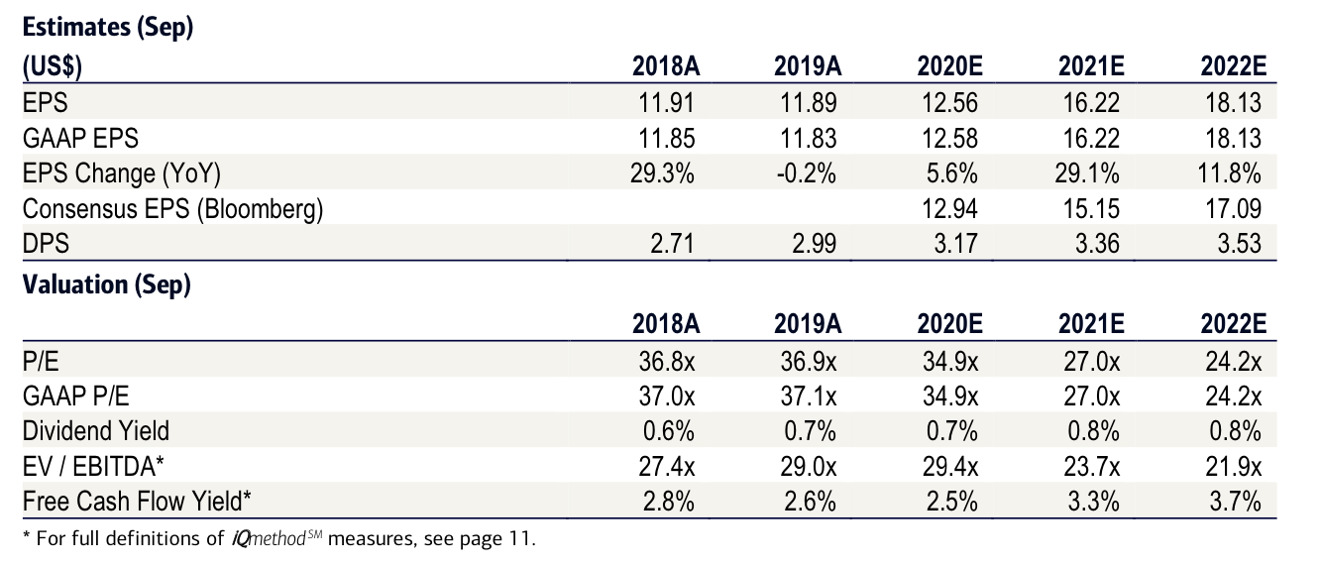

Bank of America 2021 and 2022 estimates for Apple

Overall positives for Apple, according to Mohan are Apple's hardware product cycle becoming less material as a percent of total revenue over time, the company's loyal user base, a growing install base, and low Services penetration. Potential negatives, leading to the "neutral" rating are the fact that valuation has moved to the higher end, a risk to margins and Services growth for calendar year 2021, buyback impact to the stock price is muted, and the growth in recent results being cyclical rather than "secular."

On the upside, Mohan sees possible avenues for further growth. Specifically, Mohan says that there could be "a stronger than anticipated cycle from 5G iPhones, gross margin upside, fund managers closing the underweight gap and a weak dollar" that could contribute to an incremental upside.

Notably, Mohan widely missed estimates for Apple's third quarter. Mohan predicted $51.7 billion in revenue, with a $1.89 earnings per share, versus Apple's actual revenue of $59.7 billion and an earnings per share of $2.58.