Rosenblatt Securities hikes AAPL target to $189 on overall strength

Rosenblatt Securities is raising its price target for AAPL to $189 in light of profound consumer interest in the Apple Watch Ultra and iPhone 14 Pro Max.

Rosenblatt Securities is raising its price target for AAPL to $189 in light of profound consumer interest in the Apple Watch Ultra and iPhone 14 Pro Max.

The most bearish Apple analyst on the Street is parting ways with Rosenblatt Securities, and as a result the firm said it will be ceasing its coverage of the iPhone maker.

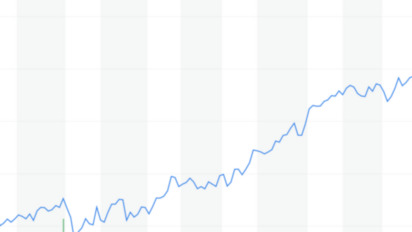

Just four days before Apple's crucial holiday quarter earnings report, Rosenblatt Securities has dramatically hiked its target price for Apple stock — to $250.

Apple's shares have more than doubled over the last year, but the rapid increase isn't just the result of some temporary irrational exuberance. Instead, as a variety of analysts and observers have noted, it means that investors have formed a new understanding of Apple as a company, shedding their formerly bleak pessimism that valued Apple far lower than the various consumer electronics rivals it has been outperforming.

Rosenblatt Securities said Monday it believes Apple is working on as many as six different "iPhone 12" models — including 'Plus' and 'Max' size variants of its 'Pro' series — but nonetheless reiterated its sell rating on the company's shares, predicting impending share losses in China that won't be helped by a so-called 'iPhone SE 2.'

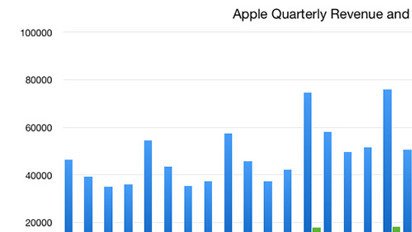

Analysts have passed comment on Apple's record fourth quarter results for the fiscal year 2019, with investor expectations and analyst estimates being beaten in a variety of ways, though the lower iPhone revenue is suggested to be an indicator of challenging December quarter results.

Continually bearish analysis from Rosenblatt Securities paints Apple as a company that disappoints with its latest iPhone launch, and is predicting low sales for the iPhone 11 and Pro models versus the 2018 releases, along with expressing concerns over sales momentum.

Analysts are weighing in on Tuesday's "It's Innovation Only" iPhone 11 launch event, with positive sentiment from industry watchers over the pricing of Apple TV+ and Apple Arcade accompanying the largely-expected iPhone upgrades.

Apple is staying relatively conservative with production of its 2019 iPhones, analysts suggest, with the overall number of units ordered from its assembly partners thought not to be that much higher than what the company requested for 2018's releases.

Following the announcement of Apple's record-setting June quarter revenue of $53.8 billion, analysts have been quick to pass judgment on the iPhone maker's fortunes, with Apple exceeding expectations but still with some trepidation present for the fourth quarter results ahead of an anticipated high-performing 2020.

Analysts at Rosenblatt Securities have changed their tune about Apple's stock, downgrading it to 'sell' over the belief it will face 'fundamental deterioration" for the next year, as well as predicting disappointing iPhone sales for the second half of 2019.

Apple will be making cuts to production for its older iPhone models in the third quarter, Rosenblatt Securities predicts, but while the 2019 iPhone manufacturing effort is thought to be on schedule, the analysts don't believe market share will be maintained in China due to the turbulent trade relations with the United States.

Analysts are weighing in on Apple's quarterly financial results the morning after its release, with generally favorable impressions of iPhone shipments better than anticipated and the growth of Services.

Apple's March-quarter financial results are set to be released on Tuesday, and all eyes are on what Apple will say — or won't say — about iPhone sales volumes. Here's what observers of the iPhone maker anticipate Apple will reveal.

Apple's attempts to boost its iPhone sales in China via price cuts offered only a temporary effect, according to Rosenblatt Securities, with post Chinese New Year sales reportedly seeing little in the way of improvement in a depressed smartphone market.

Rosenblatt Securities' Jun Zhang has jumped on reports that Apple is allegedly reducing production of the iPhone XR within weeks of its release, warning of further production cuts and possible supply issues over the quality of printed circuit boards.

Apple's stock price has taken a beating during early Monday trading, after analysts from two investment firms downgraded the iPhone producer following the latest quarterly results release, with analysts pessimistic on shipment figures and the lack of data going forward.

Analysts have offered more opinions on Tuesday's Apple special event, with J.P. Morgan and Rosenblatt Securities issuing generally positive notes to investors about the refreshed MacBook Air and Mac mini, but were more enthused about the prospects of the new iPad Pro.

Preorders for the iPhone XR are better than the equivalents for the iPhone XS and iPhone XS Max, according to Rosenblatt Securities' Jun Zhang, but that hasn't stopped the analyst from reducing expectations for the value-oriented iPhone release.

Rosenblatt Securities' Jun Zhang, who was perhaps the leading skeptic of the iPhone X and stuck with that bearish outlook even as it was clear the 2017 phone was a hit, weighs in again on iPhone XS and XS Max, with the same take.

{{ summary }}

Andrew Orr

Andrew Orr Mike Wuerthele

Mike Wuerthele Daniel Eran Dilger

Daniel Eran Dilger Malcolm Owen

Malcolm Owen

Stephen Silver

Stephen Silver