RBC Capital Markets on Friday cut its estimates for Apple's just-concluded March quarter, citing apparent weakened demand, but the firm also believes that the iPhone maker could pick up steam in the second half of the year.

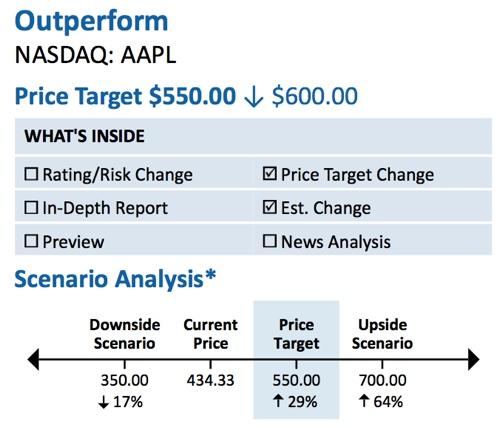

Analyst Amit Daryanani of RBC cut is price target for AAPL stock from $600 to $550, while reducing his projected sales for the March quarter. He has modeled for Apple to sell 35 million iPhones and 18.3 million iPads in the three-month span.

His new March projections of $41.2 billion in revenues and $9.59 earnings per share are below Wall Street expectations of $42.7 billion in revenues and $10.08 earnings per share.

Daryanani has also cut RBC's estimates for Apple's in-progress June quarter, when he believes the company will earn $37.3 billion in revenues and $8.72 earnings per share. Those numbers are also below market consensus, as the analyst believes Apple will be affected by product transitions during the quarter.

He sees iPhone units dropping to 28.6 million in the June quarter, while iPad sales are forecast to be around 19 million.

But beyond what he called the "June trough," Daryanani believes Apple could see some of its momentum return in the second half of calendar 2013. He sees a number of catalysts on the horizon, including anticipated debuts of iOS 7 along with a next-generation "iPhone 5S" and a more affordable new iPhone model.

The same analyst reported last month that he believes Apple will launch "multiple new phones" in the June-July timeframe. Specifically, he expects that a new low-end iPhone with a plastic casing could be Apple's way of addressing the entry-level smartphone market, where the company currently does not compete.

Beyond the iPhone, other potential boosts for Apple later this year include carrier expansion to partners like China Mobile, which is the largest wireless provider in the world, as well as the possibility of new products, like a full-fledged Apple television set or a smart wrist watch accessory.

While RBC's price target calls for AAPL shares to grow 29 percent to $550, the firm does also offer "upside" and "downside" scenarios, in which shares could swing as high as $700 or as low as $350. Despite the lower price target, RBC has maintained its "overweight" rating on Apple.