A stronger-than-expected iPhone 17 launch and resilient services growth have Wedbush betting Apple's stock still has room to climb.

Wedbush increased its 12-month price target for Apple to $320, up from $310. The change comes after Apple's record earnings in the September quarter and positive guidance for December.

Analyst Daniel Ives observed in a note to investors seen by AppleInsider that the iPhone 17 cycle is performing well in both the U.S. and China. Data suggests that the holiday season might be strong.

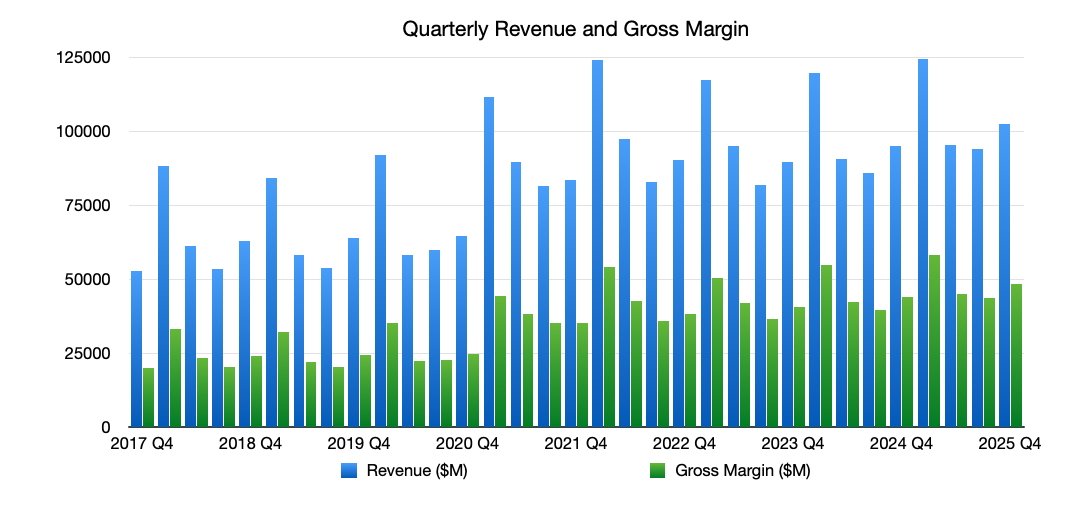

Apple reported $102.47 billion in quarterly revenue, slightly ahead of forecasts, with earnings per share reaching $1.85, topping consensus by 10 cents. Wedbush expects 10% to 12% year-over-year growth in the current holiday quarter, citing robust iPhone 17 demand and continued double-digit services growth.

The firm anticipates strong iPhone sales, particularly in China, driven by government subsidies boosting demand across the entire lineup.

iPhone 17 sales offset China slump

Apple's iPhone 17 lineup appears to be outperforming last year's iPhone 16 cycle by double-digit percentages in both major markets. That came even though the phones were only available for one week of the quarter.

Supply constraints kept iPhone revenue at $49 billion, just below analyst expectations. Wedbush expects those delayed sales to roll into the December results.

China remains Apple's biggest wild card. The region saw a 3.5% year-over-year decline, though Wedbush believes the December quarter could mark a return to growth as subsidies lift sales of the base iPhone 17 model.

Apple reported $102.47 billion in quarterly revenue

The firm noted that Apple's long-term strength in China will depend on maintaining brand loyalty amid renewed competition from Huawei.

Margins hold despite tariffs

Wedbush said Apple continues to manage tariffs and production shifts effectively. Tariffs cost the company about $1.1 billion during the quarter, but gross margin still came in at 47.2%, above expectations.

More iPhones sold in the U.S. are now being built in India instead of China. The manufacturing shift gives Apple more flexibility as trade tensions continue.

Wedbush described the transition as a "complex supply chain Rubik's Cube," but it has become a strategic strength. The firm believes Apple's growing presence in India will help cushion the impact of future tariff changes and ensure supply stability during peak demand.

Services stay the growth engine

Services led Apple's growth, rising 15% year-over-year to $28.75 billion and exceeding estimates. Wedbush called services Apple's "foundation of growth," citing their stability amid device cycles.

The segment includes the App Store, iCloud, and Apple Music, generating high-margin recurring revenue. Wedbush also addressed Apple's quiet AI approach.

They believe Apple's 2.4 billion iOS devices give it an advantage with AI strategy acceleration through partnerships like Google Gemini. Wedbush kept Apple on its "Best Ideas" list, citing its balance between hardware sales, services expansion, and manufacturing resilience.

The $320 target implies 18% upside from Apple's $271.40 closing price, positioning it as a top AI and consumer technology play for 2026. The note frames Apple's December quarter as a stress test for its entire ecosystem.