Apple's Q1 2026 results are in, with record-breaking iPhone sales, but a record R&D spend suggests the company is far from resting on its laurels.

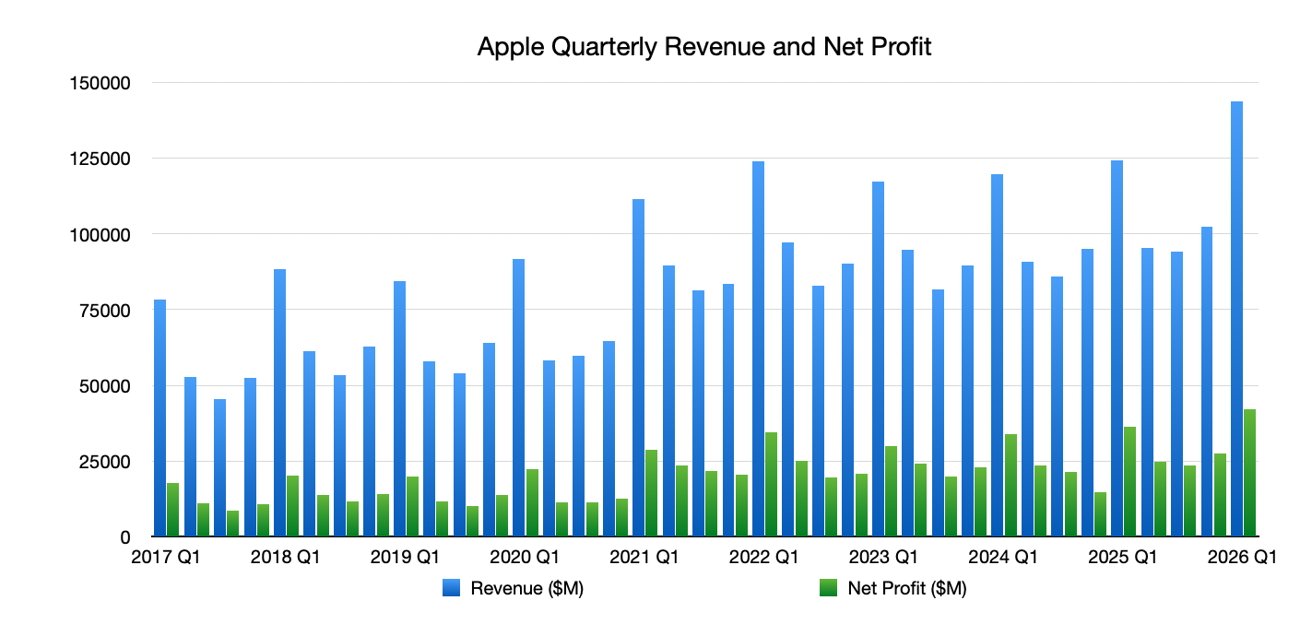

The fiscal quarter, which ended December 27, 2025, saw Apple post records aplenty. With revenue of $143.8 billion, the company saw a 16% increase over the previous year's results — a new record for the company. Of that figure, a whopping $42.1 billion was net profit.

Comparing that to the previous year's revenue of $124.3 billion and a net quarterly profit of $36.3 billion, Apple's already healthy balance sheet just got a shot in the arm. With record total revenue and earnings per share ($2.84, up 19%), it's hard to imagine how Apple shareholders could have hoped for better results.

Apple Quarterly Revenue and Net Profit, as of Q1 2026

Yet, they kept on coming. Backed by new iPhones, the Apple Watch Series 11, new AirPods Pro 3, and other launches, Apple's quarter went from strength to strength.

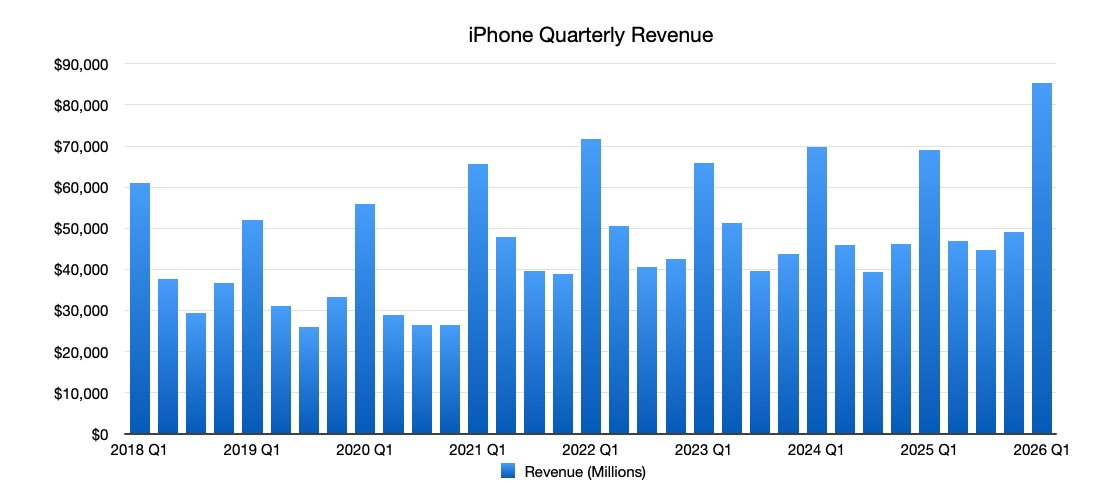

iPhone continues to be the key for Apple

The iPhone has long been vital to Apple's success, and that shows no sign of changing. In fact, Apple's Q1 2026 results present a new record for iPhone revenue.

Apple's figures show the iPhone had its best-ever quarter with a figure of $85.3 billion. That figure shows a huge increase from $69.1 billion in the year-ago quarter.

The newly launched iPhone 17 series no doubt helped drive sales, while the iPhone 16e remains a strong budget option. Deals on the outgoing iPhone 16 will also have helped give buyers a range of options to choose from.

CEO Tim Cook put the iPhone growth down to "unprecedented demand", adding that records were broken "across every geographic segment".

iPhone is once again a key revenue driver for Apple

Vitally, the iPhone's growth saw it responsible for almost 60% of the company's total revenue. That would likely be a concern for many businesses, but Apple's growth in other sectors helps insulate it from an over-reliance on iPhone sales.

As Apple continues to work on improving Apple Intelligence and Siri, iPhone sales seem likely to continue their upward trend. But a lot will depend on Apple's ability to execute on plans for a more conversational Siri — backed by its recent buyout of Q.ai.

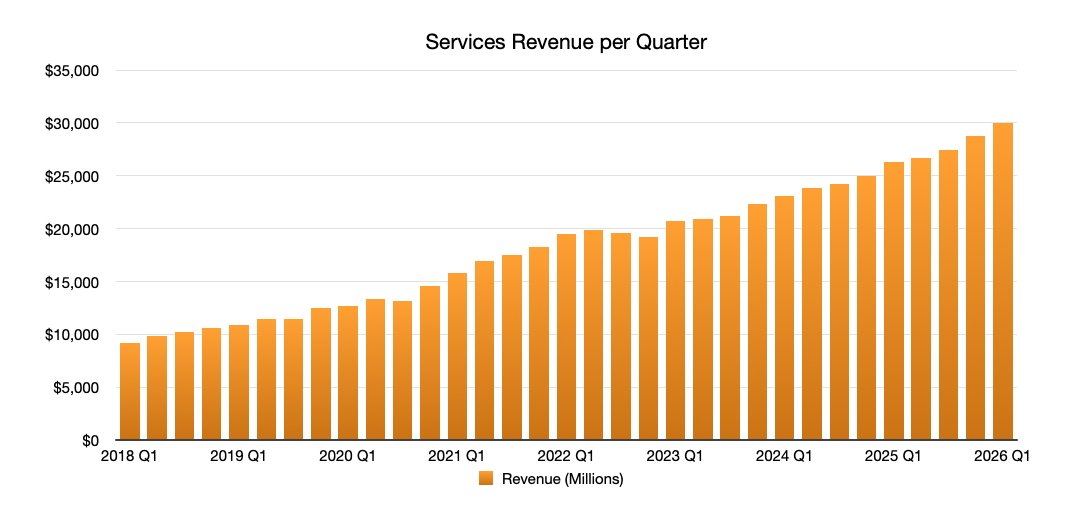

Record Services revenue shows its importance to Apple

Apple might be the iPhone company to some, but it's fast becoming a services outfit to others. With Apple Music, Apple TV, iCloud, and more, services revenue is a constant, repeatable income stream for Apple.

With that in mind, shareholders will be pleased to know that Apple posted record Services revenue for the quarter. The category broke the $30 billion barrier for the first time, a 14% increase over the same period the year prior.

Apple's Services category saw another record quarter

While it's notable that Services represented just 20.9% of revenue, down on the previous quarter, it's easy to see why. Bumper iPhone sales helped rejig the makeup of revenue.

Apple now has more than 2.5 billion active devices worldwide, with each one offering potential Services income. Add in the fact that Apple Music and Apple TV don't require an Apple device, and the ceiling for Services revenue is far from being reached.

Apple's Chinese business is back on track

Once seen as a key area for hardware growth, Apple's Chinese revenue has flattered to deceive in recent quarters. That changed in Q1 2026, with almost a 38% bump year over year.

Strong iPhone sales helped boost Chinese revenue for Apple

While that leaves China as the third most important geographic segment for Apple, the positive trend will be welcome. Unsurprisingly, the boost was thanks to bumper iPhone sales, which represented a 38% growth year over year and a record iPhone quarter for the country.

Apple told investors that its Chinese Apple Stores saw double-digit growth in the number of visitors, another reason for such strong performance.

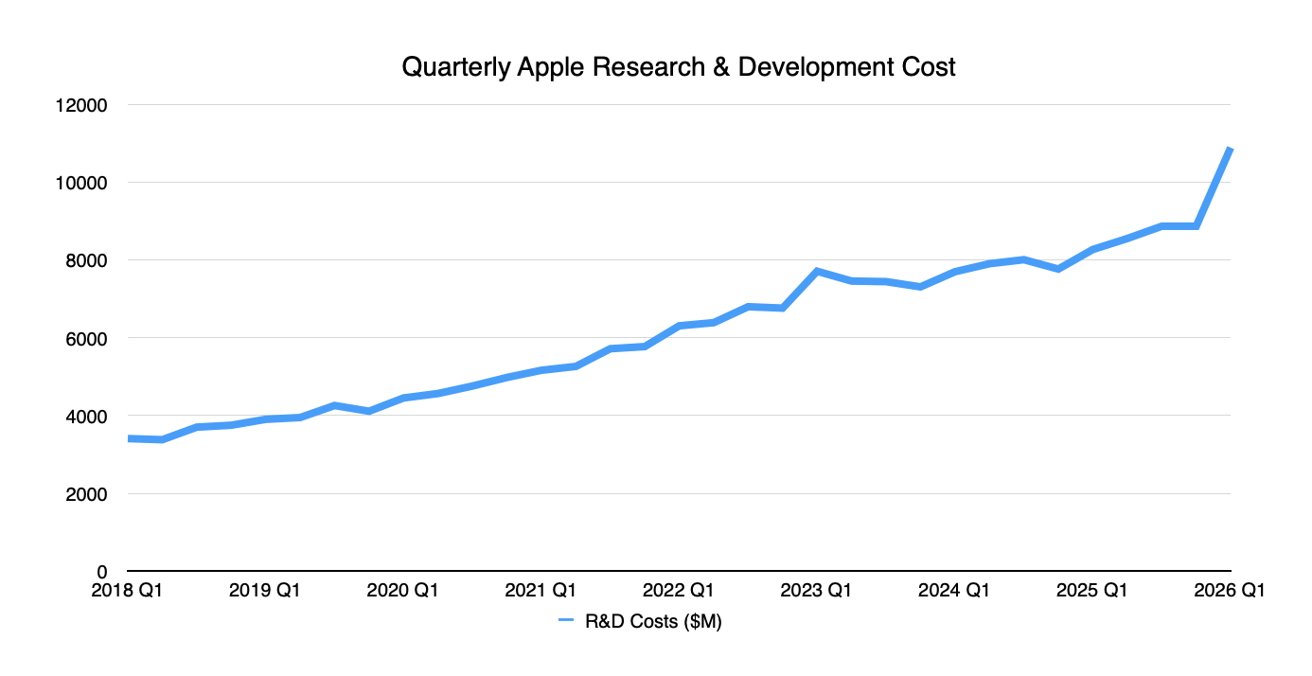

Record R&D spend acceleration shows Apple's intent

Despite such positive figures, there remains a cloud for investors over Apple. A faltering approach to AI has left the company playing catch-up, and that's annoying shareholders.

While public sentiment about AI varies, Apple is clearly using its warchest to try and figure it out — at least for investors.

Apple's figures show the company spent more than $10 billion on Research & Development (R&D) for the first time. The $10.9 billion sum was a significant increase over the $8.9 billion spent in the previous quarter.

The jump in R&D costs was Apple's biggest from one quarter to the next, again hinting at an internal desire to close the AI gap. Apple recently announced a deal to use Google Gemini to bolster Siri upgrades, but it would surely prefer to use an in-house AI model instead.

Apple spent more than ever on R&D

That costs money, as does work on perfecting the company's first foldable iPhone. That device is expected to be announced later this year, but plans for the future go far beyond 2026.

A recent report claimed Apple was developing an AI pin. But Apple is aware it has a Siri problem and will have to plough money into both software and hardware R&D if the accessory is to ever see the light of day.

What the analysts say

As always, Apple's quarterly results have sent industry analysts into overdrive.

Gene Munster

Analyst Gene Munster admitted that Apple "delivered a strong December quarter," noting that the company's performance in China was its "most notable upside". But he still believes that there is room for AAPL to grow.

Noting that Apple's stock rose just 1% in after-hours trading, Munster believes that the company's "AI credibility gap" remains a concern for investors.

J.P. Morgan

J.P. Morgan maintained its Overweight rating for Apple's stock and raised its price target from $315 to $325 a share. Analysts led by Samik Chatterjee pointed out that Apple's outlook should "calm investor nerves around memory-related impact to gross margins and a Services slowdown."

The comment refers to reports that a global memory chip shortage would impact Apple's ability to build out AI infrastructure.

However, the analysts believe that the availability of chip foundry capacity would be a concern for the company moving forward.

Morgan Stanley

Morgan Stanley also maintained its Overweight rating for AAPL, sticking with its price target of $315. But while the analysts remain positive on Apple as a whole, they did note concerns relating to the potential for memory chip price increases.

As for Apple's strong iPhone sales, Morgan Stanley believes that its product mix produced "the strongest iPhone cycle in history". Apple's suggestion that sales continue to be constrained by supply was also noted as a reason future growth could be expected.