Apple's iPhone is positioned to weather a looming smartphone memory price spike better than nearly any rival, even as industry forecasts point to softer sales in 2026.

Counterpoint Research released a report on December 16, lowering its 2026 global smartphone shipment forecast. The report attributes this to significant price hikes in DRAM and NAND flash memory.

The revised forecast expects global smartphone shipments to fall about 2% year over year, reversing earlier expectations for modest growth. Memory costs are the primary driver, with Counterpoint pointing to supply tightness and aggressive pricing from memory vendors.

For Apple, the shift creates pressure but carries far less risk than it does for many Android manufacturers. The report suggests Apple can absorb higher component costs more effectively while preserving margins.

Competitors are more likely to respond with price hikes, spec cuts, or narrower product lineups.

Memory prices are squeezing the market

Counterpoint reports that rising DRAM prices have already boosted smartphone bills of materials significantly. The steepest impact is on low-end and midrange devices, with double-digit percentage increases.

Budget phones under $200 have already seen cost increases of roughly 20% to 30% since early 2025. Midrange models face increases closer to the mid-teens, while high-end flagships have seen smaller but still meaningful jumps.

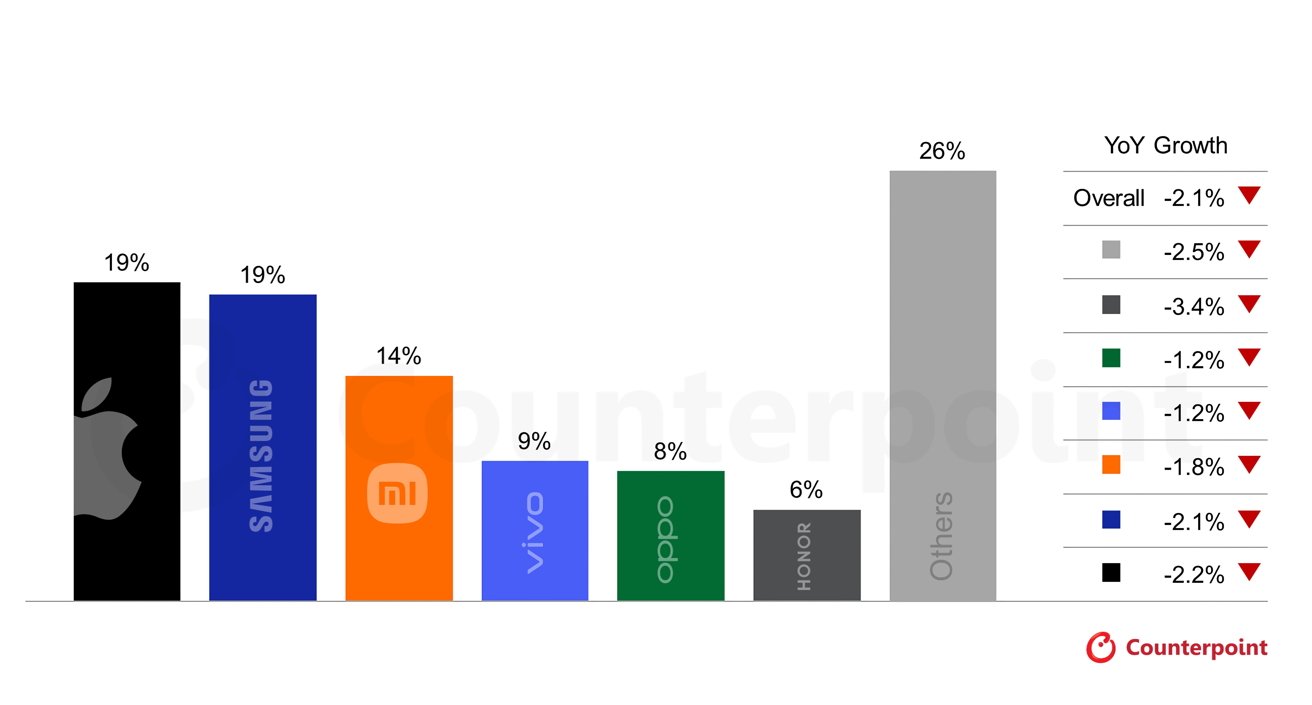

Projected 2026 global smartphone market share. Image credit: Counterpoint

Another round of cost increases is expected through the first half of 2026, driven by constrained supply and renewed demand from AI servers and PCs. The result is a market where cheap phones are becoming harder to make profitably.

That matters because low-end Android devices account for a large share of global volume. Vendors may cut back entry-level SKUs, reuse older components, or quietly raise prices to stay afloat.

Apple and Samsung are best positioned to manage the pricing shock due to scale, purchasing power, and premium-focused lineups. Apple's advantage goes beyond sheer volume and rests in tight control of its hardware strategy.

Apple and Samsung have structural advantages

RAM and flash media are commodities that Apple manages by securing long-term supply deals. This limits exposure to volatile component pricing. In part, this is why Tim Cook was hand selected by Steve Jobs for the Apple CEO job.

Higher iPhone price points also give Apple room to absorb cost increases without immediate consumer backlash.

By contrast, Chinese OEMs like Oppo, Vivo, and Honor are expected to take the largest forecast downgrades for 2026. Their portfolios lean heavily on price-sensitive segments with razor-thin margins, where passing costs on to buyers is difficult.

Counterpoint predicts that many Android vendors will trim memory configurations, reduce camera or display specs, or consolidate model lineups. These changes will make mid-range phones less competitive at a time when buyers are already stretching replacement cycles.

iPhone volumes may dip, but the year still looks solid

For Apple, Counterpoint doesn't predict a collapse in demand. Instead, it expects a very modest year-over-year dip in iPhone shipments, offset by higher average selling prices.

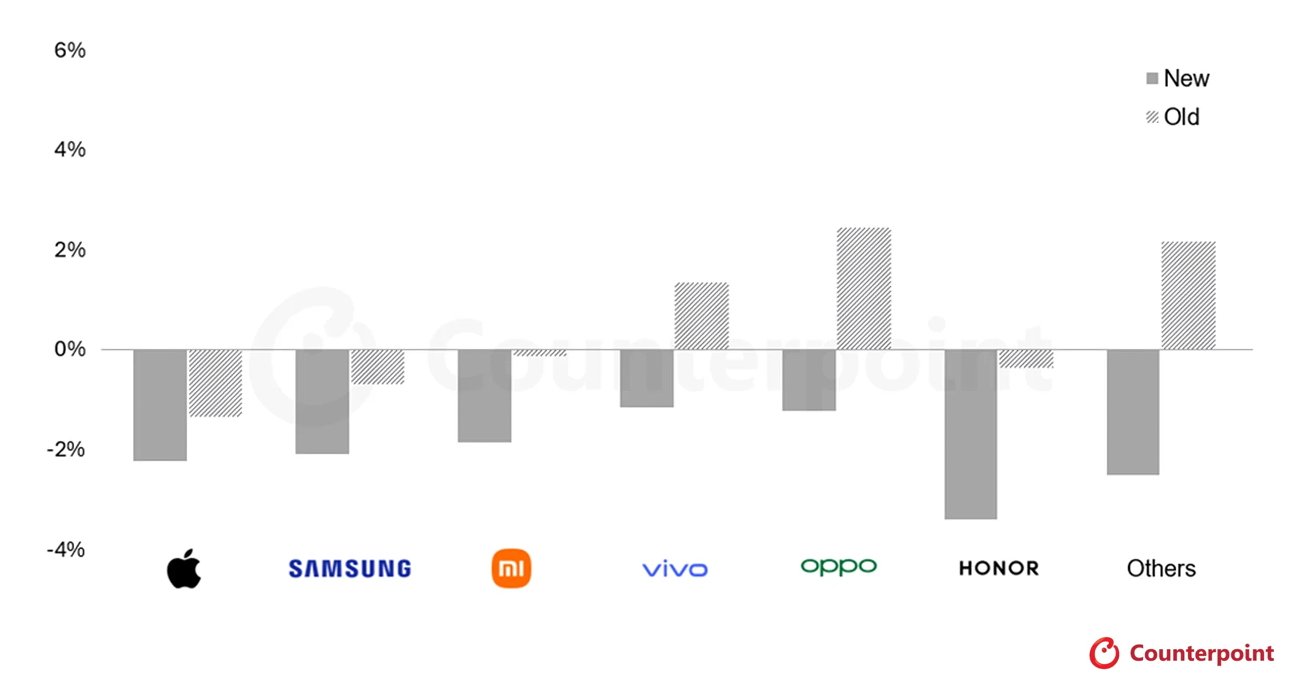

Projected year-over-year smartphone shipment growth for 2026. Image credit: Counterpoint

The firm revised its 2026 ASP growth forecast upward to nearly 7%, more than double its previous estimate. The increase reflects higher component costs being passed along and a continued shift toward higher-end models.

In practical terms, Apple may sell slightly fewer iPhones but still generate similar or higher revenue across the lineup. This approach has defined much of Apple's recent hardware strategy as upgrade cycles continue to lengthen.

A pricing storm that reshapes competition

Importantly, the report doesn't frame 2026 as a weak year for Apple. Relative to the broader smartphone market, it may actually be a strong one.

The bigger takeaway is how memory pricing could reshape the competitive landscape. As low-end devices become harder to justify, the middle of the market may thin out.

Apple benefits from the shift as fewer compelling mid-range Android options make premium devices easier to justify. Financing plans and carrier subsidies further reduce upfront costs and nudge buyers toward higher-priced devices.

If memory prices remain elevated, the next smartphone cycle may favor brands that already sell fewer, more expensive models. Apple fits that profile better than almost any company.