Apple will announce its second-quarter financial results this evening at 4:30 PM ET. Here's what happened in the quarter, and what analysts think is going to be revealed.

The Q2 2026 financial results will be shared by Apple in a press release on April 30. A short time after, at 5 P.M. Eastern, it will hold its usual analyst and investor conference call.

That call will involve both current CEO Tim Cook and CFO Kevan Parekh discussing the quarter and providing guidance for future quarters. There will also be questions from analysts about the quarter and expectations for Q3 and beyond.

There's also the small matter of the announcement with Cook replaced as CEO in September by John Ternus. Analysts will be keen to know more about the transition plans.

As usual, AppleInsider will check out the data and listen in to the conference call, to report the bigger stories from the financial event.

This article was last updated on April 29, 2025, with more analyst forecasts.

Last quarter: Q1 2026 details

Released on January 29, the first quarter results are always Apple's best, seasonally speaking. It's the highest revenue quarter of its year, due to the fall product launches and holiday sales period.

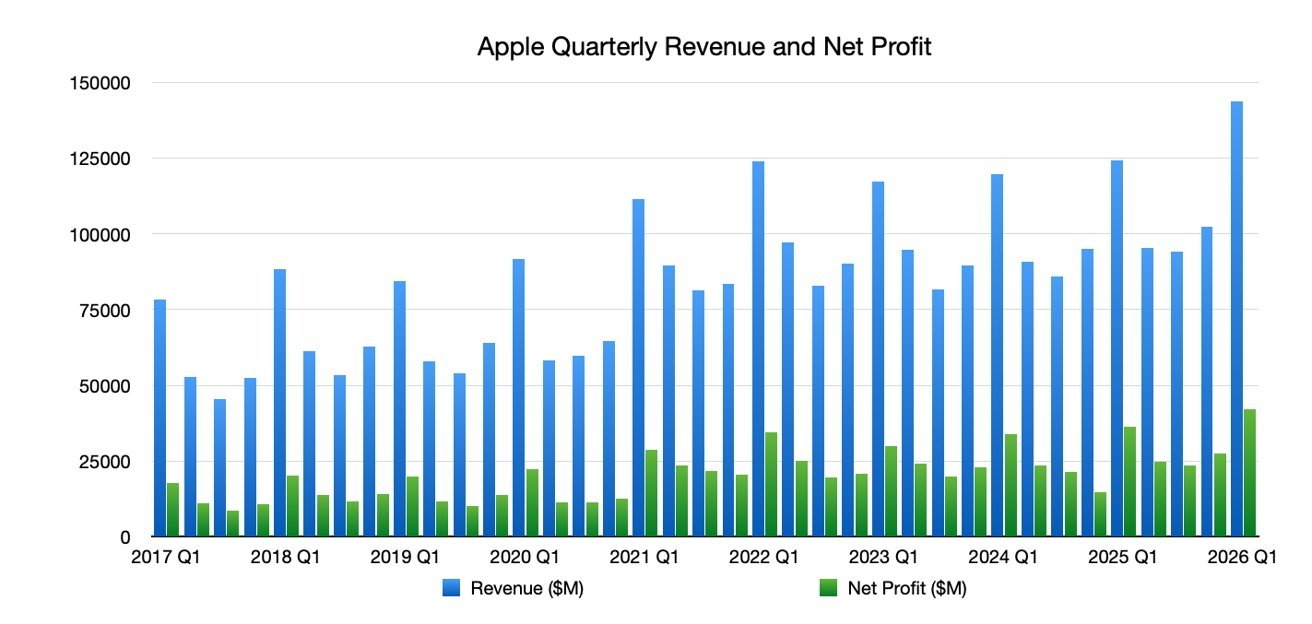

For Q1 2026, Apple hauled in record revenue of $143.8 billion, up from the $124.3 billion it brought in for Q1 2025. It reported an earnings per share of $2.84, and declared a cash dividend of $0.26 per share of common stock.

Apple Quarterly Revenue and Net Profit, as of end of January 2026

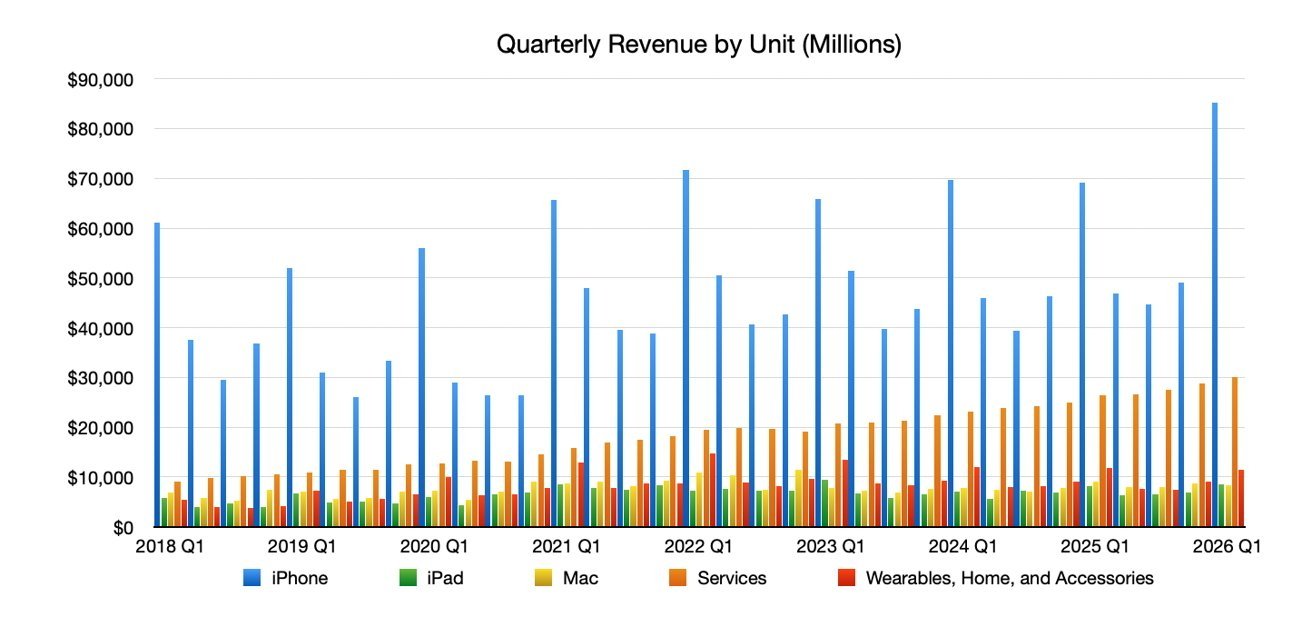

On a per-product basis, iPhone grew from $69.1 billion in the year-ago quarter to $85.3 billion. Revenue from iPad also jumped from $7.01 billion to $8.6 billion.

Mac was down from $8.9 billion to $8.39 billion, meanwhile Wearables, Home, and Accessories dipped slightly to $11.49 billion from $11.747 billion.

The ever-reliable Services continued its annual growth, from $26.34 billion to $30.013 billion.

The period enjoyed the first full quarter of availability for Apple's late Q4 launch roster, including the iPhone 17 family, iPhone Air, Apple Watch Series 11, Apple Watch SE 3, Apple Watch Ultra 3, and AirPods Pro 3. Launches in the quarter included the M5 upgrade of the iPad Pro, the M5 Apple Vision Pro, and the M5 14-inch iPad Pro.

Year-ago quarter: Q2 2025

The Q2 2025 results are the natural yardstick used to compare the Q2 2026 results against. It occurs at the same point in the seasonal cycle, and follows after the usual blockbuster Q1 figures.

For the Q2 2025 results, Apple saw its revenue grow 5% year-over-year to $95.4 billion.

Apple revenue by unit, as of end of January 2026

For iPhone, revenue was also up from $45.96 billion in Q2 2024 to $46.84 billion in Q2 2025. Mac revenue also grew slightly, from $7.45 billion to $7.95 billion.

iPad dipped from $6.4 billion to $5.56 billion, while Wearables, Home, and Accessories went from $7.9 billion for the year-previous results to $7.5 billion.

Services continued its ever-dependable march of growth, going from $23.9 billion in Q2 2024 to $26.6 billion.

That quarter benefited from the post-holiday sales of the iPhone 16 range and other fall launches. During the quarter, Apple launched the iPhone 16e, the iPad 11, the M3 iPad Air, the M4 MacBook Air, and the updated Mac Studio.

The period also had to deal with a backdrop of a tariff war, with President Donald Trump applying tariffs against all other countries. China was a particular target of the tariff hikes, but Apple and others did get a temporary semiconductor-based reprieve at the time.

What happened in Apple's second fiscal quarter of 2026

For Q2 2026, Apple will still be benefiting from the fall launch sales. But the attention will be turned towards products launched during the quarter itself.

That list includes many expected launches, including the M4 update to the iPad Air, the iPhone 17e, the M5 upgrade to the MacBook Air, and the M5 Pro and M5 Max versions of MacBook Pro.

Apple did also bring out some unexpected changes, including a refreshed Apple Studio Display, and the Apple Studio Display XDR replacing the Pro Display XDR.

MacBook Neo in Citrus

There was also the widely-celebrated launch of the MacBook Neo, a budget-focused MacBook powered by the A18 Pro chip.

As for the topics of discussion during the conference call, one will almost certainly be about pricing pressures.

The tech industry is dealing with rapidly rising prices for memory, processors, and SSDs, due to the build-out of AI infrastructure. While Apple has managed to insulate itself so far with its supply chain agreements, it's not something it can continue forever.

There is also the ever-present issue of artificial intelligence, and Apple's seemingly consistent lagging behind the rest of the industry. With the delayed Siri overhaul now expected for WWDC and the Google Gemini deal impacting its work, analysts will be keen to know Apple's plan for the future.

However, this will not be all that the analysts will want to talk about. There's also the matter of the CEO transition.

On September 1, Tim Cook will move out as CEO and become executive chairman at Apple. In his place will be John Ternus.

While it is unclear if Ternus will appear on the conference call before the start of his tenure, you can be sure that the analysts will want to prod Cook about the topic. After all, this is a major event that can have an impact on investments.

What is Wall Street expecting to see in Apples' Q2 2026 financial report?

The Wall Street consensus refers to a survey of analysts. The results are averaged out to give a general opinion of where investors and analysts are leaning in their quarterly forecasts.

Yahoo Finance

Yahoo Finance's revenue estimate for Apple in Q2 stems from 30 analysts. As of April 29, the average estimate is $109.69 billion, with a low of $107.08 billion and a high of $115.37 billion.

For the earnings per share estimate, 31 analysts put it at an average of $1.94. The low is $1.56 and the high is $2.16.

TipRanks

TipRanks also does its own analyst polling on Apple's quarter. In its forecast as of April 29, its consensus is for a revenue of $109.46 billion, with a high of $115.37 billion and a low of $104.55 billion.

On the earnings per share, the consensus is $1.95, with a high of $2.16 and a low of $1.56.

Analyst Expectations

Ahead of the results and call, analysts offer their own forecasts of what they think Apple will be declaring in its financials. Depending on the firm and the analyst, these hot takes include both positive and negative opinions about Apple.

JP Morgan

In an April 21 note to investors seen by AppleInsider, JP Morgan forecasts Apple's Q2 to result in $112.7 billion in revenue, with an earnings per share of $2.05. This will be driven by better product revenues, consisting of $82.3 billion versus a consensus of $78.8 billion.

The iPhone forecast will be aided by robust demand for the iPhone 17, hitting $59.5 billion, while Services will be in line with the guide of $30.4 billion.

For the quarter itself, memory headwinds are expected thanks to rising costs, but the issue will be not as bad as once feared. Apple is anticipated to balance revenue share relative to margins by taking modest price increases, only after efforts to limit the increase of the bill of materials, by taking advantage of its sheer scale.

These price rises could be a mid-single-digit percentage increase, or about $50 for every $1,000 of regular pricing.

JP Morgan classes Apple as "Overweight" with a price target of $325.

Bank of America

In its April 20 note, Bank of America said Apple was a premium story in what is otherwise a messy market. While Services is a main pillar for the company, the push into AI could be a new engine for growth.

With the M5 introduction, it is a major step forward for on-device processing and inference, which could help lower cloud-related expenses for consumers and businesses.

Apple is rated a "Buy" by BoA, with a price target of $325. It has forecasted an upside of 23.4%.

Morgan Stanley

On April 20, before the CEO change announcement, Morgan Stanley's pre-earnings talk was positive, expecting for revenue and the EPS to be 1% to 2% better than the consensus. There were the usual worries, including if memory will impact revenue, but with a belief that iPhone, Mac, and Services will be stable.

The company stuck with its overweight call and a $315 price target.

After the CEO announcement, Morgan Stanley said Apple's core strategy probably won't change, with priorities continuing as they are instead of shifting in direction. It's an evolutionary, not transformational, change.

Goldman Sachs

In pre-CEO chatter on April 20, Goldman Sachs forecasted a second-quarter EPS of $2.00, above its Wall Street consensus of $1.93. Services and favorable exchange rates will help bump up the results.

Services are projected to have 14% year-on-year growth despite an apparently slow App Store quarter, as well as price increases on various products.

Overall, there was a sense that Goldman Sachs was pushing back against what it viewed as negative sentiment for Apple's earnings. The stock price's underperformance didn't match up to its actual position, it felt.

On April 22, another note added that Services will grow 14% year-over-year to $30 billion, iPhone revenue up 23% to $85.3 billion, and overall revenue growth of between 13% and 16% year-over year.

Goldman reaffirmed its "Buy" recommendation with a $330 price target.

UBS

UBS told CNBC on April 28 that it is raising its price target for Apple from $280 to $287. It's a small increase, but positive, even if they kept the Neutral rating.

UBS analyst David Vogt believes that the strong supply chain and sustained demand for the iPhone 17 series will raise iPhone revenue about 20% year-over-year.

However, the neutral rating stems from longer-term risks, including product delays and lower amounts of innovation in future products, as well as a possible decline in iPhone unit shipments.

Evercore ISI

In a note shared by Evercore ISI on April 27, Apple will report revenue at or above the consensus estimates of $109.2 billion. The earnings per share is expected at $1.94.

To Evercore, iPhone revenue should grow 20% year-over-year, thanks to a strong iPhone 17 cycle and ongoing demand in China. Services should sustain mid-teens growth, with Apple Pay, iCloud, Licensing, and AppleCare offsetting a weaker App Store.

Evercore ISI rates Apple as an Outperform with a $330 price target.