Apple is announcing its first-quarter financial results for 2026 on January 29. Here's what to expect from the figures, in a quarter that the company has already said will be record-breaking.

Apple's Q1 2026 financial results will be shared via a press release on Thursday, January 29. It will arrive just ahead of the company's analyst and investor conference call at 5 P.M. Eastern.

The call will see CEO Tim Cook discussing the finer points of the numbers alongside CFO Kevan Parekh, as well as providing guidance of what investors can expect in future quarters. This will include the duo dealing with a volley of questions from analysts about the quarter and their expectations of the future.

Apple's seasonal sales, along with its traditional fall launch schedule, mean the Q1 results will be the biggest for the year overall. In the final quarter of the fiscal year, Tim Cook said that they were expecting a record-breaking quarter.

As usual, AppleInsider will be looking at the results data and listening in to the conference call.

This article was last updated on January 28, 2026, with the addition of more analyst forecasts.

Last quarter: Q4 2025 details

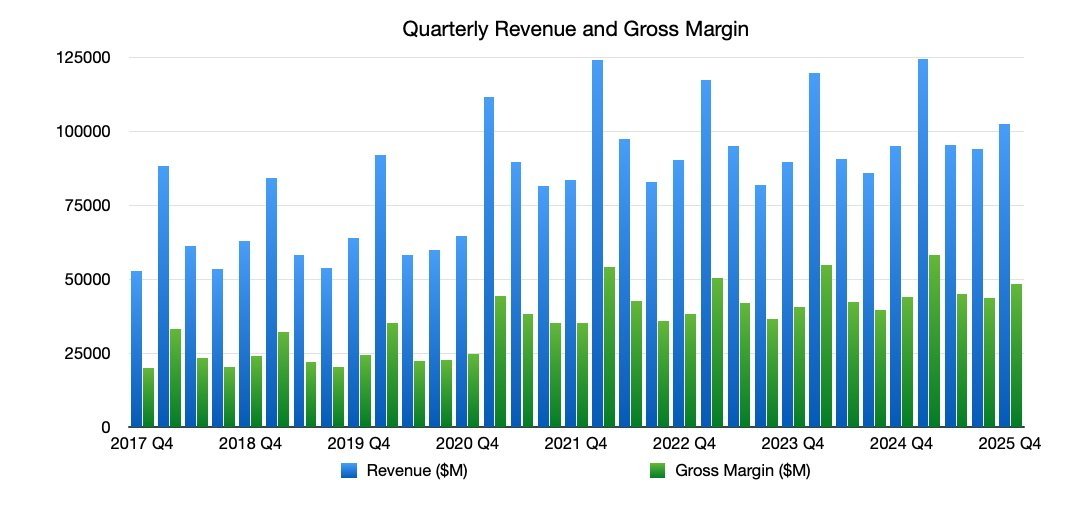

The Q4 2025 financial results had Apple achieve a revenue of $102.5, up from Q4 2024's figure of $94.93 billion and a revenue record for the quarter. The earnings per share went up to $1.85.

The Wall Street consensus placed Apple at $107.79 billion for revenue and $1.78 for the earnings per share.

Apple quarterly revenue and gross margin, as of Q4 2025.

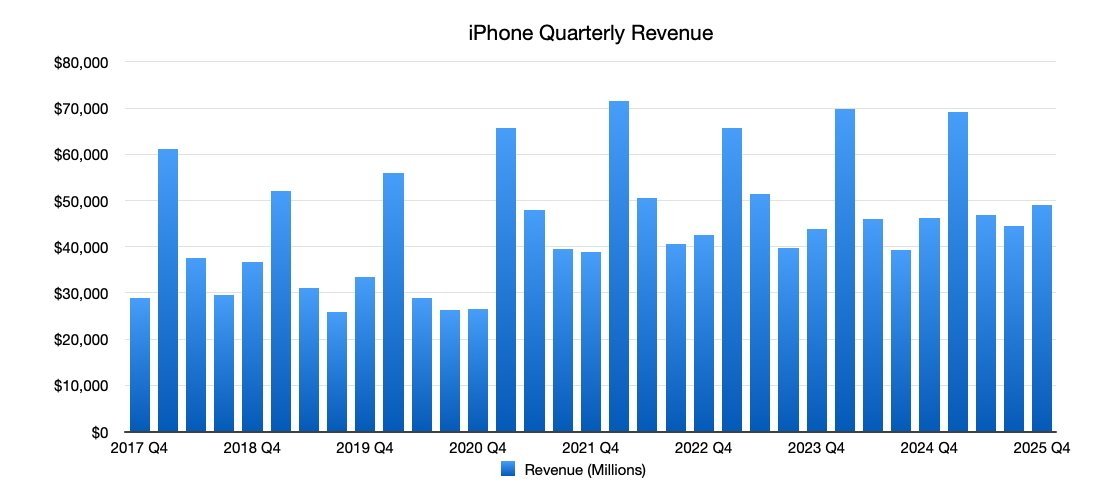

On a per-product basis, iPhone revenue of $49.02 billion was up from $46.22 billion one year prior, but didn't quite meet Wall Street expectations of $50.2 billion.

Revenue from iPad sales were barely up year-over-year, at $6.952 billion versus $6.95 billion. Mac revenue did better, going from $7.74 billion in Q4 2024 to $8.73 billion in Q4 2025.

Services remained a reliable source of growth at $28.75 billion, up from $24.9 billion 12 months earlier. Wearables, Home, and Accessories joined iPad in being relatively flat, but with a minor dip from $9.04 billion in the year-ago quarter to $9.01 billion.

During Q4, Apple saw numerous product launches at the end of the period, including the iPhone 17 family of smartphones, iPhone Air, Apple Watch Series 11, Apple Watch SE 3, Apple Watch Ultra 3, and AirPods Pro 3. As is usual, those launches will have made a minimal impact on the bottom line of the quarter itself, but would be more fully felt during the entire Q1 2026 period.

Year-ago quarter: Q1 2025

The figures from Q1 2025 will be used as the yardstick for the Q1 2026 results. For Q1 2025, the revenue hit $124.3 billion, up from $119.58 billion reported one year ago in Q1 2024.

On a product category basis, iPhone revenue reached $69.1 billion, marginally down from $69.7 billion in Q1 2024. However, iPad revenue went up from $7.02 billion in Q1 2024 to $8.088 billion in Q1 2025.

Mac revenue went from a fairly static $7.78 billion in Q1 2024 to a higher $8.987 billion for Q1 2025. Wearables, Home, and Accessories flattened a bit, slightly dipping down from $11.95 billion to $11.747 billion.

Services continued to be reliable, growing from $23.12 billion in Q1 2024 to $26.34 billion in Q1 2025.

What happened in Apple's 2025 holiday quarter

As usual, the quarter is expected to be the highest of the year, thanks to the double punch of holiday season sales and feeling the full effects of the fall product launches.

Apple iPhone revenue, as of Q4 2025.

There were also some product launches in October, including the M5 upgrade of the iPad Pro, the M5 Apple Vision Pro, and the M5 14-inch MacBook Pro. While sales from these products didn't happen throughout the entire quarter, the early-in-period launches mean there will be some impact from them in the period, especially when considering seasonal sales patterns.

Not everything will be rosy for the company's financials, however. Despite presidential exceptions, Apple will still have to pay tariffs. And, in the year-ago quarter, the M4 MacBook Pro with Pro and Max processors launched, so Mac sales won't be a good compare.

For Q4, tariffs cost Apple $1.1 billion, with about $2 billion paid out in total. For Q1 2026, Apple expects to have paid around $1.4 billion.

What is Wall Street expecting to see in Apple's Q1 2026 financial report?

The Wall Street consensus refers to a survey of analysts. The results are averaged out to give a general opinion of where investors and analysts are leaning in their quarterly forecasts.

Yahoo Finance

In the estimates published by Yahoo Finance as of January 24, 30 analysts offered a mean average revenue estimate of $138.35 billion. The estimate's range goes from a high of $142.74 billion to a low of $136.66 billion, indicating that analysts are expecting the result to be at the lower end of the range

For the earnings per share, a group of 31 forecasts an average of $2.67, with a high of $2.80 and a low of $2.51.

TipRanks

On January 24, TipRanks offered its own consensus figures. The revenue forecast is at $133.38 billion, with a range from $136.31 billion to $142.74 billion.

The earnings per share is expected to be $2.67, with a range from $2.51 to $2.77.

Analyst Expectations

Ahead of the results and call, analysts offer their own forecasts of what they think Apple will be declaring in its financials. Depending on the firm and the analyst, these hot takes include both positive and negative opinions about Apple.

Wedbush

The January 28 note from Wedbush puts Apple as bringing in revenue of $136.68 billion for the quarter, up from $124 billion last year.

This is down from the top estimate of Wedbush's Wall Street consensus of $138.4 billion. But even so, that figure is still beatable in the view of the analysts, due to a strong iPhone 17 launch.

Wedbush is also bullish on Apple talking about its AI plans, following its deal with Google to use Gemini, and could lead to a bumper 2026 for the company. As it stands, Wedbush doubts that Apple's share price has an "AI premium" attached at the moment, which could raise the price by $75 to $100 if properly realised.

Wedbush maintains its current price target for Apple at $350 with an "Outperform" rating.

Evercore

On January 27, Evercore reiterated its predictions of better-than-expected results from Apple, after raising the price target to $330 on January 9.

Evercore's forecast for Apple is for revenue of $140.5 billion in the quarter, with an earnings per share of $2.71. iPhone demand will grow revenues 13% year-over-year, with Services continuing its growth by 17% year-over-year.

However, the Services growth could've been better, had it not been for weaker App Store performance in the quarter. With the App Store making approximately 20% of Services revenue, the weakened gaming revenue from Asia will probably make a bit of a dent in quarterly growth for the operating segment.

Apple is also well-positioned to handle the current issue of soaring RAM prices. While the cost has been increasing, Apple is expected to benefit in the short term due to its use of long-term deals with suppliers at previous pricing levels that will protect the pricing.

Morgan Stanley

Morgan Stanley's January 26 note to investors builds upon the earlier claim from the analysts that Apple will have an incredible 2026. It maintains the $315 price target it set in October, as well as the "Overweight" stock rating.

For the quarter itself, overall revenue is expected at $139.5 billion, or a 12.3% year-over-year growth for the period. The Earnings Per Share is anticipated to be $2.70.

iPhone will make up $80 billion of the total, based on what the analysts say is one of the strongest iPhone cycles in history. iPad revenue will reach $7.98 billion, Mac will get to $9.3 billion, Wearables, Home, and Accessories should achieve $12.5 billion, and Services will get tantalizingly close to $30 billion by hitting $29.8 billion.

On the industry's memory crisis, Morgan Stanley believes that Apple has sufficient low-priced NAND inventory to last the next quarter. However, it will eventually have to face paying higher prices for memory, and raise product costs to match.

JP Morgan

The January 26 note from JP Morgan had strong expectations from Apple from the outset. It raised AAPL's one-year target to $315 from $305, though it still considered the stock to be "Overweight."

For the quarter specifically, it forecasts Q1 revenues of $139.8 billion, with iPhone revenue up 16% year-over-year at $80.2 billion. Services will grow, but it will be just shy of the $30 billion milestone at $29.9 billion.

The gross margin will be at 47.6%, the analysts think, at the midpoint of the 47% to 48% guidance. Operating expenses should track below guidance at around $17.5 billion, due to expectations of a delay in the timing of a ramp in fees to access LLM models.

While the industry faces memory pressures, JPM doubts it will greatly affect the results. Apple's famous bargaining power and long-term contracts with suppliers will help insulate it from the extra cost.

Goldman Sachs

In its pre-results advisory, Goldman Sachs has maintained its Buy rating and $320 price target for AAPL. In media reports, its analysts say it is a good time to buy Apple's shares, in part because its stock is down 9% since December.

When it comes to growth, Goldman Sachs expects revenue to increase by 9% in the full fiscal 2026 year and in 2027. The first quarter earnings per share is anticipated to be $2.66.

First-quarter iPhone revenue is thought to increase 13% year-over-year, thanks to 5% unit growth and 26% growth in China, as well as an 8% improvement in price and mix. While App Store spending is down 7% year-over-year in the quarter, that should still result in overall Services revenue growth of 14%.

As individual analysts report what they expect, we will add to this post.