Less than a week after its last rise, JP Morgan now says Apple's target price is $325, specifically because of the latest earnings and Apple's guidance for the next two quarters.

On January 26, ahead of what was already expected to be a record-breaking quarter for Apple, JP Morgan raised its target from $305 to $315. Now following both higher than predicted earnings and, in particular, Apple's projections for the future, the investment firm has raised the target again.

In a note to investors seen by AppleInsider, JP Morgan summarized the earnings report and said that this should calm fears about rising costs.

It has been repeatedly presumed that Apple will be hit by the same memory price rises as the rest of the industry. But as Cook said in the earnings call, Apple is not going to be affected too badly in the next quarter.

JP Morgan notes that Cook and Chief Financial Officer Kevan Parekh appeared to imply that they are less concerned with memory. They alluded to how they are more concerned with chip manufacturing capacity.

That's because Apple has been surprised by the demand for the iPhone 17 range, and has not been able to fully supply that demand as yet.

Nonetheless, Apple did say that while memory was not a concern for the quarter, it will increase by Q3. Even so, Apple expects to weather the storm, even though Tim Cook refused to say more than that the firm had some options.

Long term strength

It was already clear that the iPhone 17 range was particularly successful, but JP Morgan notes that the earnings show this is true globally. Specifically, that it is not down to how Apple has benefited from subsidies in China.

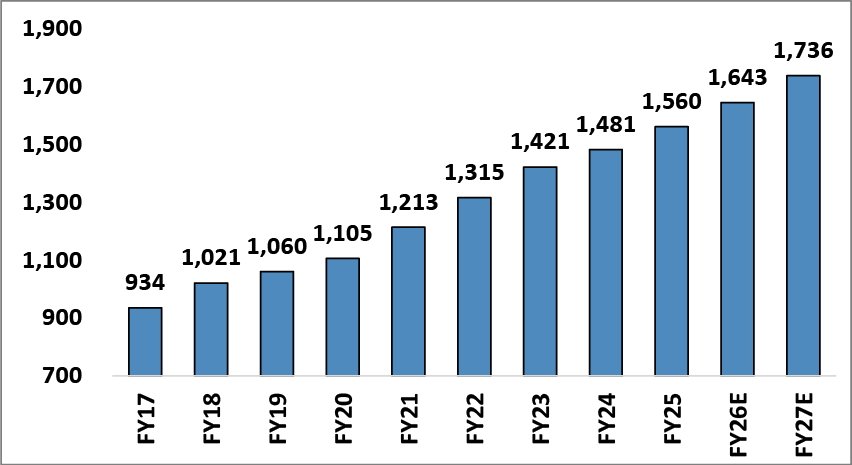

How JP Morgan expects iPhone growth to go. Figures are in millions. Image credit: JP Morgan

So with what it describes as robust growth across every geographic market, the investment firm sees Apple having the strength to overcome supply chain issues.

Plus, Apple managed a record December quarter revenue for the App Store, alongside breaking records in multiple Services.

Alongside this Services momentum, plus the iPhone demand, JP Morgan also continues to expect growth once the newly revamped Siri is finally launched.

Potential risks ahead

JP Morgan's analysts had previously predicted a possible slowing down in App Store sales, but now says that there was only limited evidence of that in the new earnings report. It remains a possibility for the future, however.

Tim Cook's eventual departure could present a risk to Apple's share price — image credit: Apple

More certainly, Tim Cook is going to step down as CEO at some point and JP Morgan warns that the loss of a key person is always a risk. Nonetheless, in this case, it thinks Apple is now managing change well, and that the company's group of executives is strong.

Cook and those executives are expected, though, to continue Apple's investment in acquisitions and new business directions. JP Morgan notes that Apple is secretive about these issues, so there could be ones that turn out to have unexpectedly high costs.

Then, too, despite its current success worldwide, and especially in China, the iPhone continues to face pressure from local rivals. Plus as the world economy continues to be uncertain, all smartphone sales may drop.

Still, with all of this in mind, JP Morgan is also predicting demand to be high for 2026's iPhone 18 range. That's in particular if Apple launches an iPhone Fold.

After earnings, Apple stock acted like it always does. It initially surged upwards a few percent, but will open down, at $257.11, down 0.45% overnight.